Enlarge image

OFFICE USE ONLY

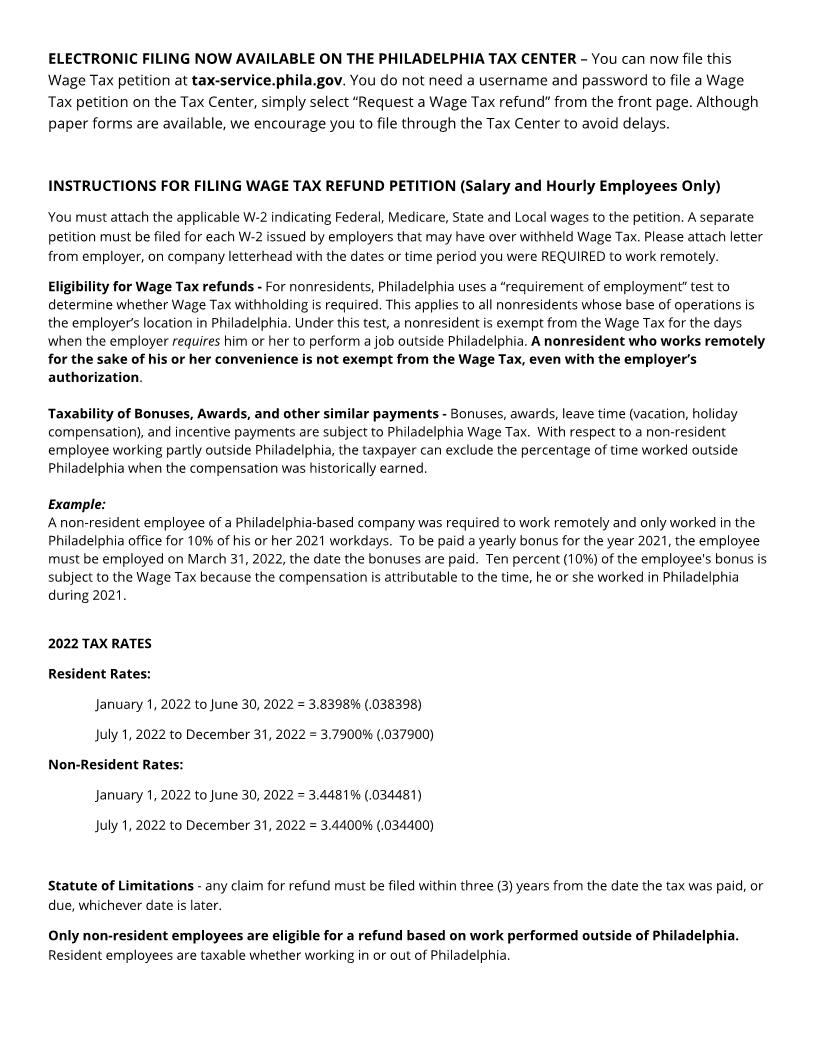

TAX YEAR WAGE TAX REFUND PETITION

SALARY/HOURLY EMPLOYEES

2022 (Not to be used by Commissioned Employees)

Read the instructions for both the Employer as well as the Employee on the reverse side of this form prior to completing this petition.

Print or type all information. The completed petition must include:

W-2 showing Federal, State, Medicare and Local wages

Signature of Employee and Employer

PA Schedule UE if claiming expenses on Line 2E. If PA Schedule UE has an entry on Line 15, submit a breakdown of those expenses.

EMPLOYEE'S NAME SOCIAL SECURITY NUMBER DAYTIME TELEPHONE NUMBER

HOME ADDRESS OCCUPATION

CITY STATE ZIP CODE IF PARTIAL YEAR, PROVIDE DATES:

From To

EMPLOYER EMPLOYER IDENTIFICATION NUMBER (EIN)

PLACE OF EMPLOYMENT COLUMN A COLUMN B

January 1, 2022 to June 30, 2022 July 1, 2022 to December 31, 2022

1. Gross Compensation per W-2 .00 .00

A. Non-Taxable Stock Options included in Line 1 (Must reflect on W-2) .00 .00

B. Adjusted Gross Compensation (Subtract Line 1A from Line 1) .00 .00

2. Computation of taxable compensation and/or allowable expenses 181 Days/1448 Hours 184 Days/1472 Hours

A. Number of Days/Hours (Include overtime from Line 2C)

B. Non-workdays/Hours (Total of weekend, vacation, holiday, sick or any type of leave time) Days/Hours Days/Hours

C. Number of actual Workdays/Hours (Base__________Overtime__________) Days/Hours Days/Hours

(Line 2A minus Line 2B) If computing overtime, see instructions on reverse.

D. Number of actual Days/Hours worked outside of Philadelphia in Line 2C. A list of dates and

locations when you worked outside of Philadelphia, verified and signed by your employer, Days/Hours Days/Hours

is required to be attached. Also provide a copy of Telework Agreement if applicable.

E. Percentage of time worked outside of Philadelphia.

Divide Line 2D by Line 2C.and round the resulting percentage to 4 decimal places. .%.%

F. Non-taxable compensation earned outside of Philadelphia (Line 1B times Line 2E) .00 .00

G. (i) Total non-reimbursed business expenses allowable under Income Tax Regulation Section

204. Please submit Pennsylvania Schedule UE .00 .00

(ii) Multiply amount on Line G (i) by the percentage on Line 2E .00 .00

(iii) Deductible non-reimbursed employee business expenses. Subtract Line G (ii) from Line G (i) .00 .00

H. Non-taxable income and/or deductible employee business expenses Add Line 2F and Line 2G (iii) .00 .00

3. Net Taxable compensation (Line 1B minus Line 2H) .00 .00

4. TAX Resident of Philadelphia multiply Line 3, Column A by .038398 and Column B by .037900.

DUE Non-Resident of Philadelphia Line 3, Column A by .034481, and Column B by .034400. .00 .00

5. TOTAL TAX DUE (Add Line 4, Column A and Line 4, Column B.) .00

6. Wage tax withheld per W-2 .00

7. REFUND REQUESTED (Line 6 minus Line 5) .00

EMPLOYER CERTIFICATION

I certify that the facts shown above supporting employee's claims are correct based on available payroll records. Individuals serving as authorized official

signatories should be familiar with employee's time and attendance, as well as applicable Wage Tax Regulations. Income Tax Regulations Section 401

through 404 requires that the employer withhold and allocate wages for tax purposes. General Regulation Section 306 (2) provides that the employer, for

and on behalf of the employee, requests the refund.

AUTHORIZED OFFICIAL SIGNATURE (Signature must be clear and legible.) PRINTED NAME DAYTIME TELEPHONE NUMBER

EMPLOYEE CERTIFICATION

I HEREBY CERTIFY that the statements contained herein and in any supporting schedule or exhibit are true and correct to the best of my knowledge and

belief. I understand that if I knowingly make any false statements herein, I am subject to such penalties as may be prescribed by City Ordinance.

EMPLOYEE'S SIGNATURE (Signature must be clear and legible.) DATE

2022 Salary Wage Petition 01-30-2023