Enlarge image

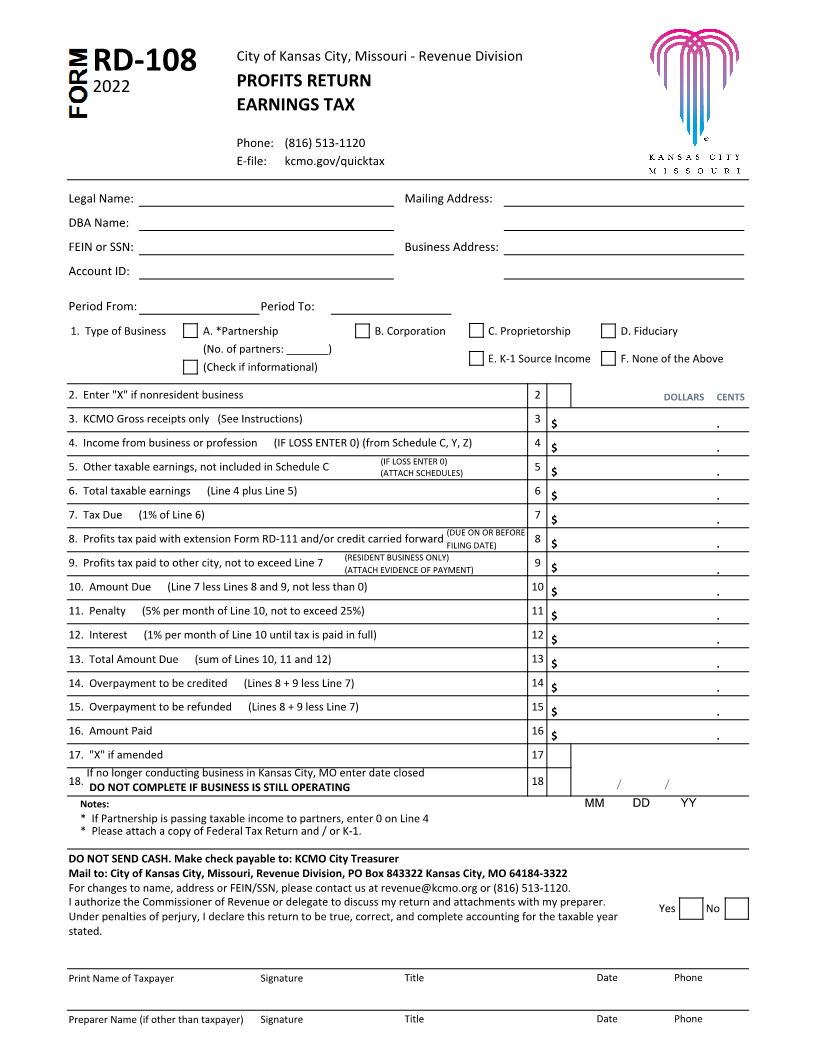

City of Kansas City, Missouri - Revenue Division

RD-108

2022 PROFITS RETURN

EARNINGS TAX

Phone: (816) 513-1120

E-file: kcmo.gov/quicktax

Legal Name: Mailing Address:

DBA Name:

FEIN or SSN: Business Address:

Account ID:

Period From: Period To:

1. Type of Business A. *Partnership B. Corporation C. Proprietorship D. Fiduciary

(No. of partners: _______)

E. K-1 Source Income F. None of the Above

(Check if informational)

2. Enter "X" if nonresident business 2 DOLLARS CENTS

3. KCMO Gross receipts only (See Instructions) 3 $ .

4. Income from business or profession (IF LOSS ENTER 0) (from Schedule C, Y, Z) 4 $ .

(IF LOSS ENTER 0)

5. Other taxable earnings, not included in Schedule C (ATTACH SCHEDULES) 5 $ .

6. Total taxable earnings (Line 4 plus Line 5) 6 $ .

7. Tax Due (1% of Line 6) 7 $ .

(DUE ON OR BEFORE

8. Profits tax paid with extension Form RD-111 and/or credit carried forward FILING DATE) 8 $ .

(RESIDENT BUSINESS ONLY)

9. Profits tax paid to other city, not to exceed Line 7 (ATTACH EVIDENCE OF PAYMENT) 9 $ .

10. Amount Due (Line 7 less Lines 8 and 9, not less than 0) 10 $ .

11. Penalty (5% per month of Line 10, not to exceed 25%) 11 $ .

12. Interest (1% per month of Line 10 until tax is paid in full) 12 $ .

13. Total Amount Due (sum of Lines 10, 11 and 12) 13 $ .

14. Overpayment to be credited (Lines 8 + 9 less Line 7) 14 $ .

15. Overpayment to be refunded (Lines 8 + 9 less Line 7) 15 $ .

16. Amount Paid 16 $ .

17. "X" if amended 17

If no longer conducting business in Kansas City, MO enter date closed

18. DO NOT COMPLETE IF BUSINESS IS STILL OPERATING 18 / /

Notes: MM DD YY

* If Partnership is passing taxable income to partners, enter 0 on Line 4

* Please attach a copy of Federal Tax Return and / or K-1.

DO NOT SEND CASH. Make check payable to: KCMO City Treasurer

Mail to: City of Kansas City, Missouri, Revenue Division, PO Box 843322 Kansas City, MO 64184-3322

For changes to name, address or FEIN/SSN, please contact us at revenue@kcmo.org or (816) 513-1120.

I authorize the Commissioner of Revenue or delegate to discuss my return and attachments with my preparer. Yes No

Under penalties of perjury, I declare this return to be true, correct, and complete accounting for the taxable year

stated.

Print Name of Taxpayer Signature Title Date Phone

Preparer Name (if other than taxpayer) Signature Title Date Phone