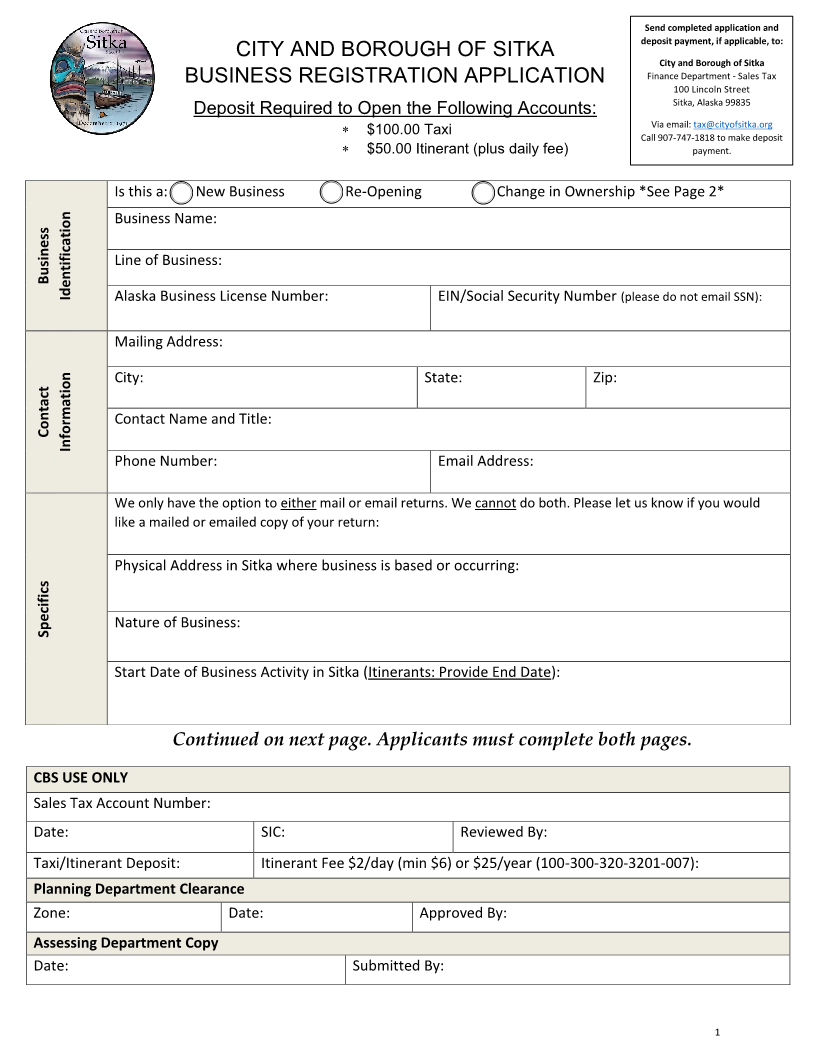

Enlarge image

Send completed application and

deposit payment, if applicable, to:

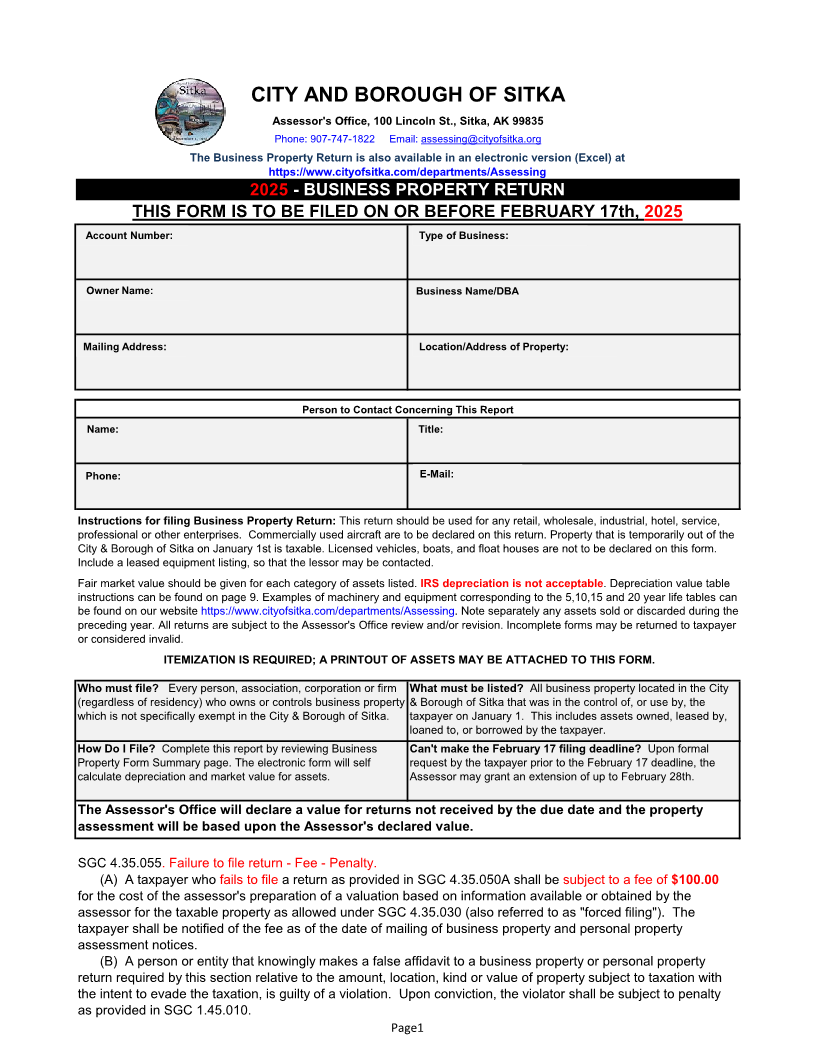

CITY AND BOROUGH OF SITKA

City and Borough of Sitka

Finance Department - Sales Tax

BUSINESS REGISTRATION APPLICATION 100 Lincoln Street

Sitka, Alaska 99835

Deposit Required to Open the Following Accounts:

Via email: tax@cityofsitka.org

$100.00 Taxi Call 907-747-1818 to make deposit

$50.00 Itinerant (plus daily fee) payment.

Is this a: ( ) New Business ( ) Re-Opening ( ) Change in Ownership *See Page 2*

Business Name:

Line of Business:

Business

Identification Alaska Business License Number: EIN/Social Security Number (please do not email SSN):

Mailing Address:

City: State: Zip:

Contact Name and Title:

Contact

Information

Phone Number: Email Address:

We only have the option to either mail or email returns. We cannot do both. Please let us know if you would

like a mailed or emailed copy of your return:

Physical Address in Sitka where business is based or occurring:

Specifics Nature of Business:

Start Date of Business Activity in Sitka (Itinerants: Provide End Date):

Continued on next page. Applicants must complete both pages.

CBS USE ONLY

Sales Tax Account Number:

Date: SIC: Reviewed By:

Taxi/Itinerant Deposit: Itinerant Fee $2/day (min $6) or $25/year (100-300-320-3201-007):

Planning Department Clearance

Zone: Date: Approved By:

Assessing Department Copy

Date: Submitted By:

1