Enlarge image

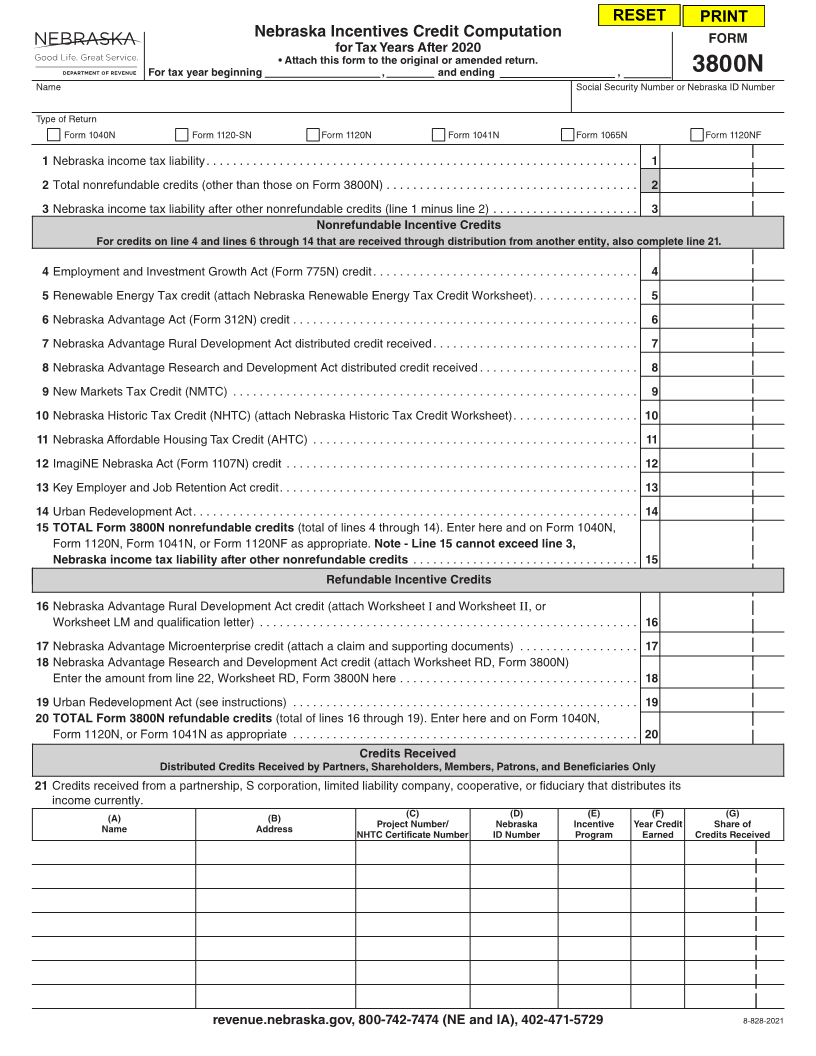

RESET PRINT

Nebraska Incentives Credit Computation FORM

for Tax Years After 2020

• Attach this form to the original or amended return.

For tax year beginning , and ending , 3800N

Name Social Security Number or Nebraska ID Number

Type of Return

Form 1040N Form 1120-SN Form 1120N Form 1041N Form 1065N Form 1120NF

1 Nebraska income tax liability ................................................................. 1

2 Total nonrefundable credits (other than those on Form 3800N) ...................................... 2

3 Nebraska income tax liability after other nonrefundable credits (line 1 minus line 2) ...................... 3

Nonrefundable Incentive Credits

For credits on line 4 and lines 6 through 14 that are received through distribution from another entity, also complete line 21.

4 Employment and Investment Growth Act (Form 775N) credit ........................................ 4

5 Renewable Energy Tax credit (attach Nebraska Renewable Energy Tax Credit Worksheet) ................ 5

6 Nebraska Advantage Act (Form 312N) credit .................................................... 6

7 Nebraska Advantage Rural Development Act distributed credit received ............................... 7

8 Nebraska Advantage Research and Development Act distributed credit received ........................ 8

9 New Markets Tax Credit (NMTC) ............................................................. 9

10 Nebraska Historic Tax Credit (NHTC) (attach Nebraska Historic Tax Credit Worksheet) ................... 10

11 Nebraska Affordable Housing Tax Credit (AHTC) ................................................. 11

12 ImagiNE Nebraska Act (Form 1107N) credit ..................................................... 12

13 Key Employer and Job Retention Act credit ...................................................... 13

14 Urban Redevelopment Act ................................................................... 14

15 TOTAL Form 3800N nonrefundable credits (total of lines 4 through 14). Enter here and on Form 1040N,

Form 1120N, Form 1041N, or Form 1120NF as appropriate. Note - Line 15 cannot exceed line 3,

Nebraska income tax liability after other nonrefundable credits .................................. 15

Refundable Incentive Credits

16 Nebraska Advantage Rural Development Act credit (attach Worksheet Iand Worksheet II, or

Worksheet LM and qualification letter) ......................................................... 16

17 Nebraska Advantage Microenterprise credit (attach a claim and supporting documents) .................. 17

18 Nebraska Advantage Research and Development Act credit (attach Worksheet RD, Form 3800N)

Enter the amount from line 22, Worksheet RD, Form 3800N here .................................... 18

19 Urban Redevelopment Act (see instructions) .................................................... 19

20 TOTAL Form 3800N refundable credits (total of lines 16 through 19). Enter here and on Form 1040N,

Form 1120N, or Form 1041N as appropriate .................................................... 20

Credits Received

Distributed Credits Received by Partners, Shareholders, Members, Patrons, and Beneficiaries Only

21 Credits received from a partnership, S corporation, limited liability company, cooperative, or fiduciary that distributes its

income currently.

(A) (B) (C) (D) (E) (F) (G)

Name Address Project Number/ Nebraska Incentive Year Credit Share of

NHTC Certificate Number ID Number Program Earned Credits Received

revenue.nebraska.gov, 800-742-7474 (NE and IA), 402-471-5729 8-828-2021