Enlarge image

Rev. 02-17

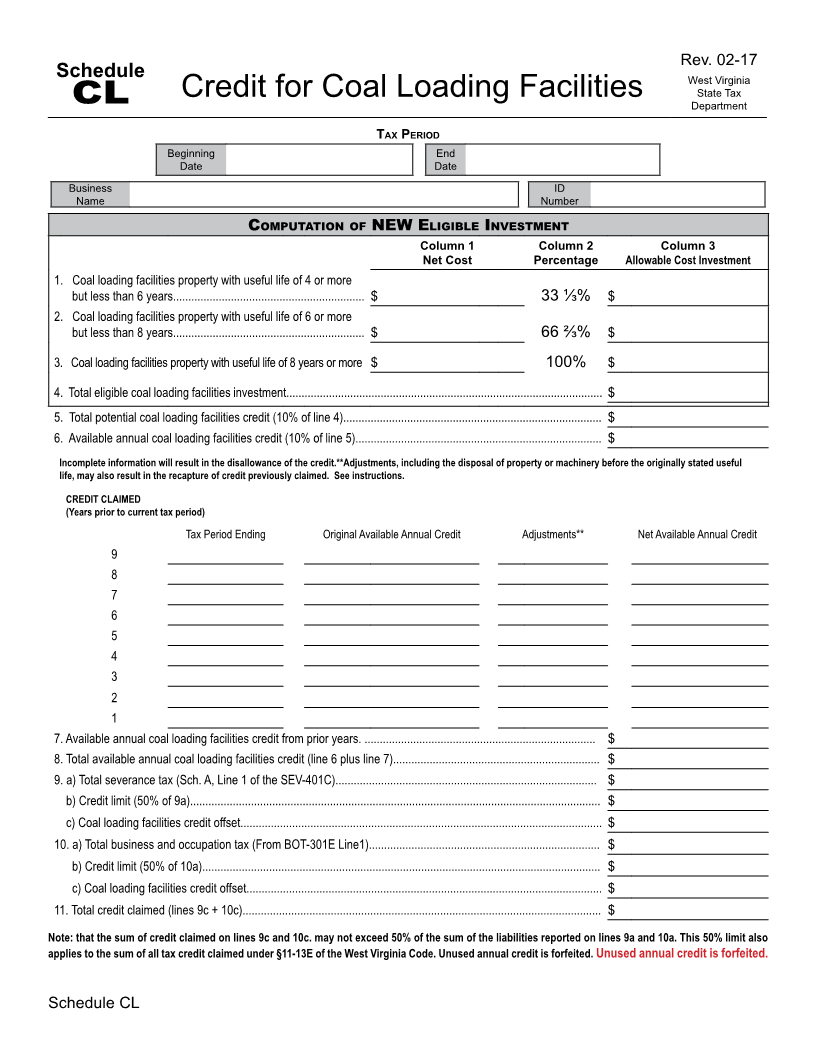

Schedule West Virginia

State Tax

CL Credit for Coal Loading Facilities Department

T axPeriod

Beginning End

Date Date

Business ID

Name Number

Computation of nEW E ligiblE invEstmEnt

Column 1 Column 2 Column 3

Net Cost Percentage Allowable Cost Investment

1. Coal loading facilities property with useful life of 4 or more

but less than 6 years............................................................... $ 33 ⅓% $

2. Coal loading facilities property with useful life of 6 or more

but less than 8 years............................................................... $ 66 ⅔% $

3. Coal loading facilities property with useful life of 8 years or more $ 100% $

4. Total eligible coal loading facilities investment........................................................................................................ $

5. Total potential coal loading facilities credit (10% of line 4)..................................................................................... $

6. Available annual coal loading facilities credit (10% of line 5)................................................................................. $

Incomplete information will result in the disallowance of the credit.**Adjustments, including the disposal of property or machinery before the originally stated useful

life, may also result in the recapture of credit previously claimed. See instructions.

CredIt ClAImed

(Years prior to current tax period)

Tax Period Ending Original Available Annual Credit Adjustments** Net Available Annual Credit

9

8

7

6

5

4

3

2

1

7. Available annual coal loading facilities credit from prior years. ............................................................................ $

8. Total available annual coal loading facilities credit (line 6 plus line 7).................................................................... $

9. a) Total severance tax (Sch. A, Line 1 of the SEV-401C)...................................................................................... $

b) Credit limit (50% of 9a)....................................................................................................................................... $

c) Coal loading facilities credit offset....................................................................................................................... $

10. a) Total business and occupation tax (From BOT-301E Line1)............................................................................ $

b) Credit limit (50% of 10a)................................................................................................................................... $

c) Coal loading facilities credit offset..................................................................................................................... $

11. Total credit claimed (lines 9c + 10c)...................................................................................................................... $

Note: that the sum of credit claimed on lines 9c and 10c. may not exceed 50% of the sum of the liabilities reported on lines 9a and 10a. this 50% limit also

applies to the sum of all tax credit claimed under §11-13e of the West Virginia Code. Unused annual credit is forfeited. Unused annual credit is forfeited.

Schedule CL