Enlarge image

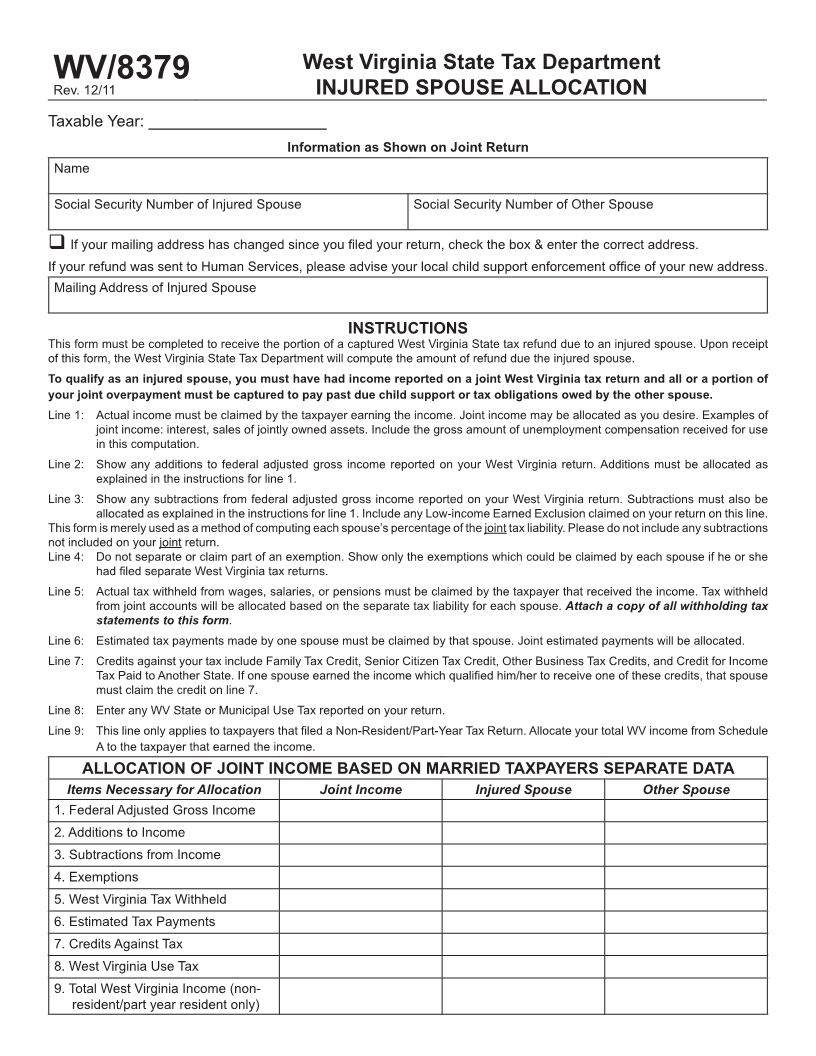

West Virginia State Tax Department

WV/8379

Rev. 12/11 INJURED SPOUSE ALLOCATION

Taxable Year: ____________________

Information as Shown on Joint Return

Name

Social Security Number of Injured Spouse Social Security Number of Other Spouse

If your mailing address has changed since you filed your return, check the box & enter the correct address.

If your refund was sent to Human Services, please advise your local child support enforcement office of your new address.

Mailing Address of Injured Spouse

INSTRUCTIONS

This form must be completed to receive the portion of a captured West Virginia State tax refund due to an injured spouse. Upon receipt

of this form, the West Virginia State Tax Department will compute the amount of refund due the injured spouse.

To qualify as an injured spouse, you must have had income reported on a joint West Virginia tax return and all or a portion of

your joint overpayment must be captured to pay past due child support or tax obligations owed by the other spouse.

Line 1: Actual income must be claimed by the taxpayer earning the income. Joint income may be allocated as you desire. Examples of

joint income: interest, sales of jointly owned assets. Include the gross amount of unemployment compensation received for use

in this computation.

Line 2: Show any additions to federal adjusted gross income reported on your West Virginia return. Additions must be allocated as

explained in the instructions for line 1.

Line 3: Show any subtractions from federal adjusted gross income reported on your West Virginia return. Subtractions must also be

allocated as explained in the instructions for line 1. Include any Low-income Earned Exclusion claimed on your return on this line.

This form is merely used as a method of computing each spouse’s percentage of the joint tax liability. Please do not include any subtractions

not included on your joint return.

Line 4: Do not separate or claim part of an exemption. Show only the exemptions which could be claimed by each spouse if he or she

had filed separate West Virginia tax returns.

Line 5: Actual tax withheld from wages, salaries, or pensions must be claimed by the taxpayer that received the income. Tax withheld

from joint accounts will be allocated based on the separate tax liability for each spouse. Attach a copy of all withholding tax

statements to this form.

Line 6: Estimated tax payments made by one spouse must be claimed by that spouse. Joint estimated payments will be allocated.

Line 7: Credits against your tax include Family Tax Credit, Senior Citizen Tax Credit, Other Business Tax Credits, and Credit for Income

Tax Paid to Another State. If one spouse earned the income which qualified him/her to receive one of these credits, that spouse

must claim the credit on line 7.

Line 8: Enter any WV State or Municipal Use Tax reported on your return.

Line 9: This line only applies to taxpayers that filed a Non-Resident/Part-Year Tax Return. Allocate your total WV income from Schedule

A to the taxpayer that earned the income.

ALLOCATION OF JOINT INCOME BASED ON MARRIED TAXPAYERS SEPARATE DATA

Items Necessary for Allocation Joint Income Injured Spouse Other Spouse

1. Federal Adjusted Gross Income

2. Additions to Income

3. Subtractions from Income

4. Exemptions

5. West Virginia Tax Withheld

6. Estimated Tax Payments

7. Credits Against Tax

8. West Virginia Use Tax

9. Total West Virginia Income (non-

resident/part year resident only)