Enlarge image

RPD-41287 (2021) New Mexico Taxation and Revenue Department

Rev. 10/01/2021

2021 Calculation of Estimated Corporate Income Tax — Method 4

Penalty and Interest on Underpayment (page 1 of 4)

PURPOSE OF THIS FORM: If you calculate estimated corporate income tax payments using Method 4, pursuant to Section 7-2A-9.1 NMSA 1978, and by using

Method 4, you can reduce the amount of penalty and interest on the underpayment of estimated corporate income tax you owe instead of using the lower of Method 1, 2,

or 3, complete this form and attach it to your CIT-1 return. For more information on the methods and whether your corporation qualifies to use Method 4, see Determine

The Amount Of Your Quarterly Estimated Tax Payment and Restrictions On Methods Of Computing The Installment Payment Due on page 3 of the instructions.

To use Method 4, you must also mark the box on CIT-1, page 2, line 19a. If you don’t need to use Method 4, don’t attach this form and don’t mark box 19a on CIT-1, page

2. The Department will compute any underpayment penalty and interest due, if any, using the lower of Method 1, 2, or 3 and issue you an assessment of penalty and

interest for underpayment of estimated tax.

Print your company’s name Enter your federal employer identification number (FEIN)

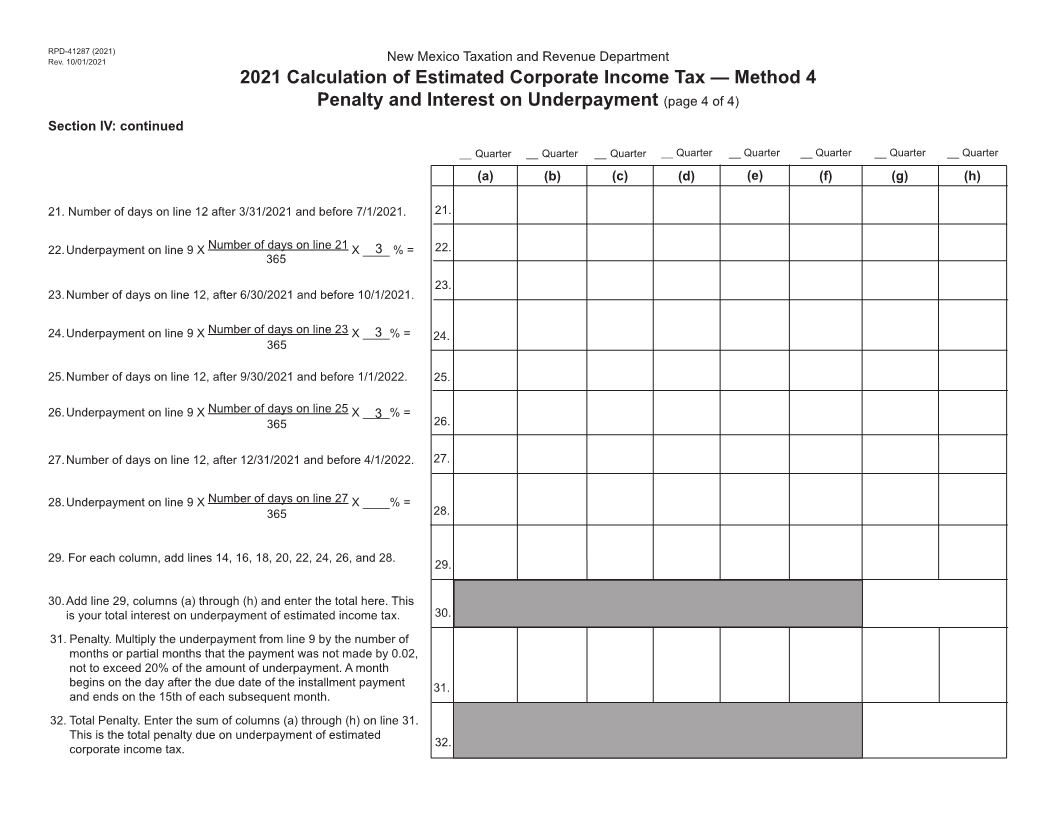

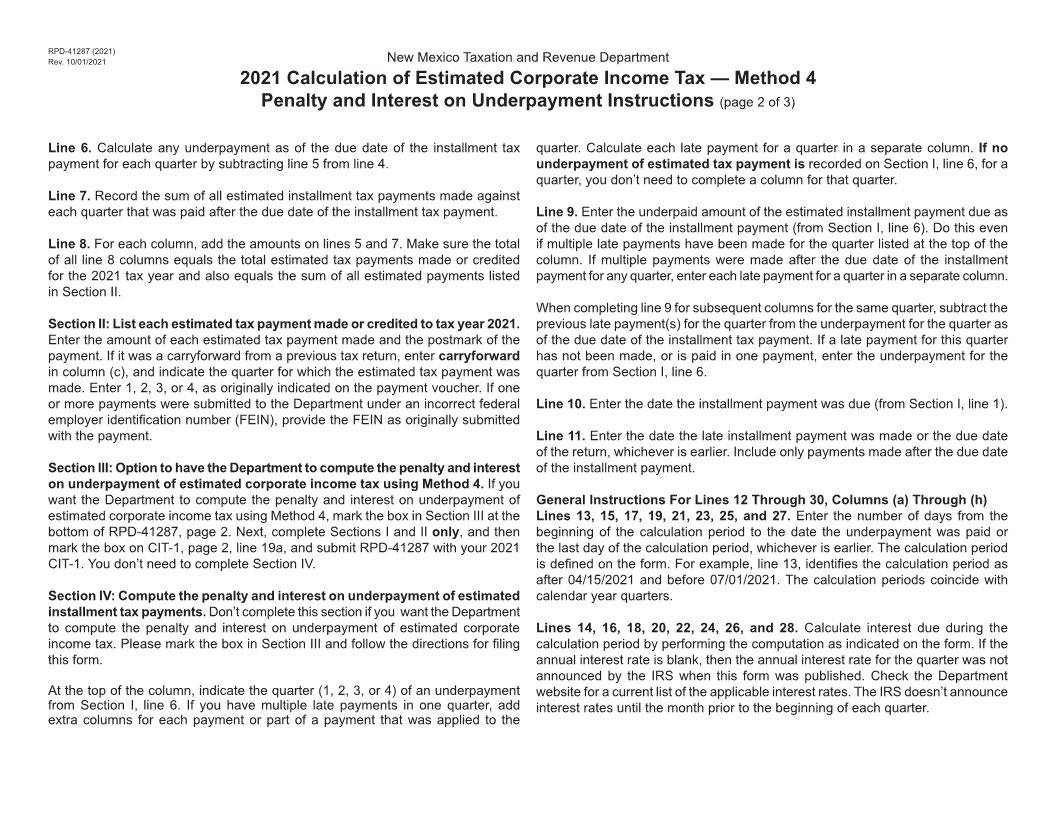

Section I. Calculate the estimated installment payment due for each quarter using Method 4 and calculate the underpayment for each quarter. Using the instructions for

this form, complete the schedule below to calculate underpayment of estimated corporate income tax. Complete lines 1 through 8 for each quarter of your tax year.

NOTE: If your corporate income tax less credits for the current taxable year is less 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

than $5,000, don’t file this form. You don’t owe quarterly estimated tax. (a) (b) (c) (d)

1. For each quarter, enter the due date of the quarterly estimated installment tax

payment. Use the 4th, 6th, 9th, and 12th month of the corporation’s tax year.

1.

2. Enter the New Mexico net taxable income earned in the corresponding quarter.

(The portion of CIT-1, line 9, earned in each quarter.) 2.

3. Enter the net New Mexico corporate income tax due (the portion of CIT-1,

line 14) for the corresponding quarter. If less than zero, enter zero. 3.

4. For each quarter, multiply line 3 by 80% (0.80) and enter here. This is the 4.

estimated installment tax payment due.

5. For each quarter, enter the estimated tax payments made on or before the due

date of the installment tax payment. Include payments of tax withheld. See the 5.

instructions.

6. Subtract line 5 from line 4 and enter here. This is the underpayment for the

quarter as of the due date of the installment tax payment. 6.

7. For each quarter, enter any estimated tax payments made after the due date 7.

of the installment tax payment.

8. Add lines 5 and 7 and enter here. This is the total estimated tax paid for the

current quarter. 8.