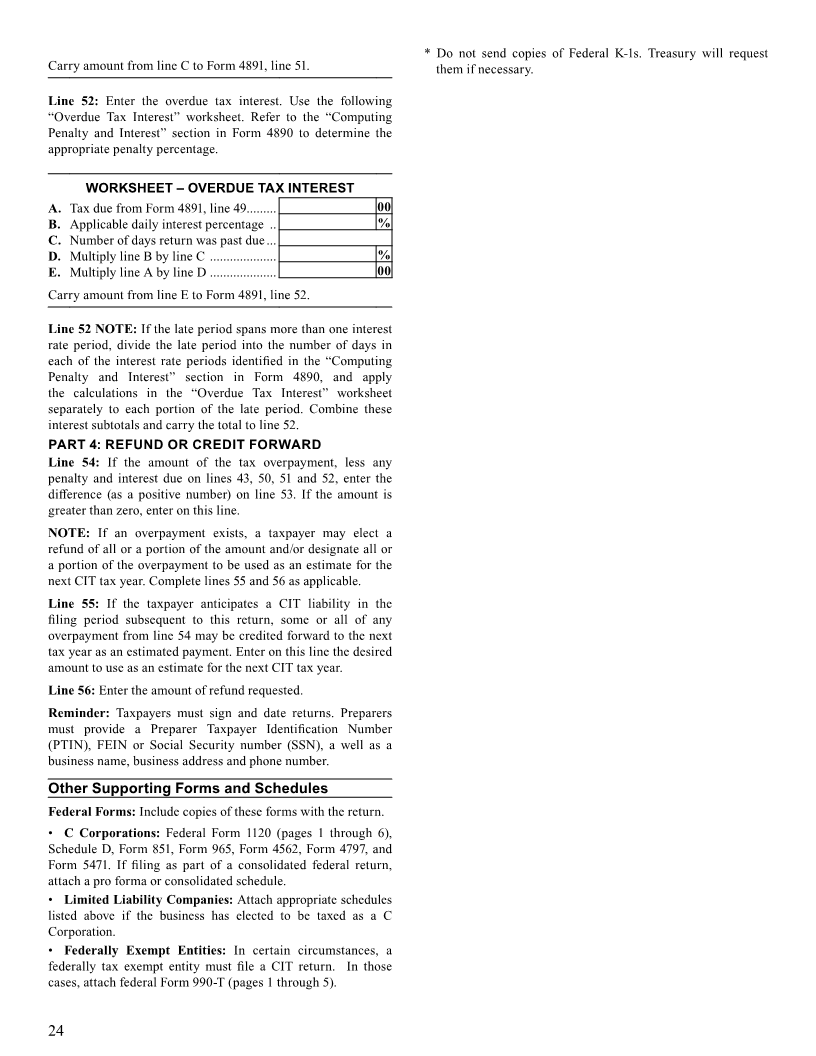

Enlarge image

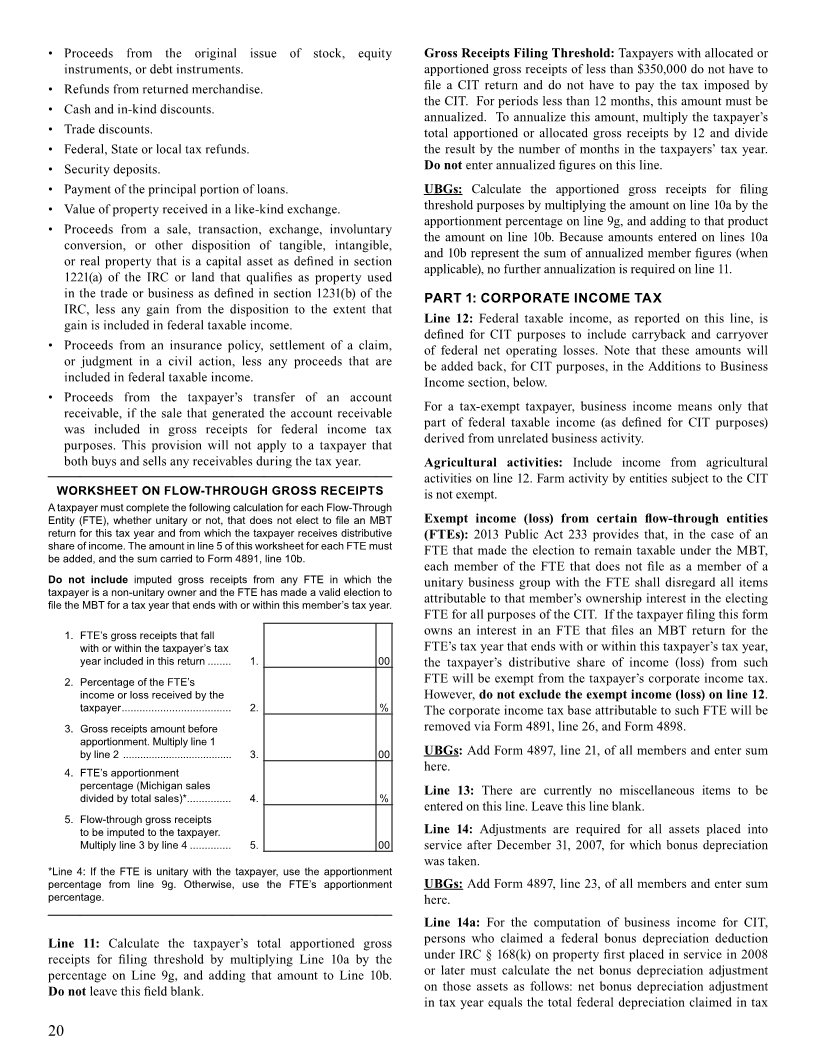

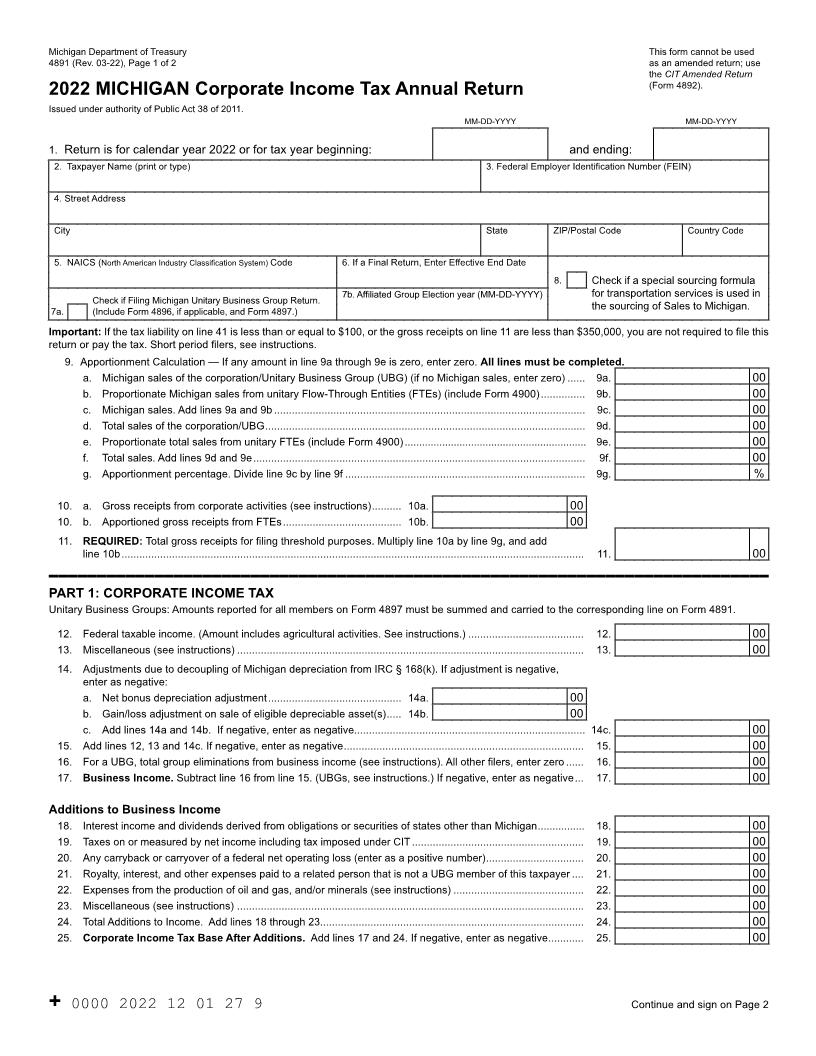

Michigan Department of Treasury This form cannot be used 4891 (Rev. 03-22), Page 1 of 2 as an amended return; use the CIT Amended Return (Form 4892). 2022 MICHIGAN Corporate Income Tax Annual Return Issued under authority of Public Act 38 of 2011. MM-DD-YYYY MM-DD-YYYY 1. Return is for calendar year 2022 or for tax year beginning: and ending: 2. Taxpayer Name (print or type) 3. Federal Employer Identification Number (FEIN) 4. Street Address City State ZIP/Postal Code Country Code 5. NAICS (North American Industry Classification System) Code 6. If a Final Return, Enter Effective End Date 8. Check if a special sourcing formula Check if Filing Michigan Unitary Business Group Return. 7b. Affiliated Group Election year (MM-DD-YYYY) for transportation services is used in 7a. (Include Form 4896, if applicable, and Form 4897.) the sourcing of Sales to Michigan. Important: If the tax liability on line 41 is less than or equal to $100, or the gross receipts on line 11 are less than $350,000, you are not required to file this return or pay the tax. Short period filers, see instructions. 9. Apportionment Calculation — If any amount in line 9a through 9e is zero, enter zero. All lines must be completed. a. Michigan sales of the corporation/Unitary Business Group (UBG) (if no Michigan sales, enter zero) ...... 9a. 00 b. Proportionate Michigan sales from unitary Flow-Through Entities (FTEs) (include Form 4900) ............... 9b. 00 c. Michigan sales. Add lines 9a and 9b ......................................................................................................... 9c. 00 d. Total sales of the corporation/UBG ............................................................................................................ 9d. 00 e. Proportionate total sales from unitary FTEs (include Form 4900) ............................................................... 9e. 00 f. Total sales. Add lines 9d and 9e ................................................................................................................ 9f. 00 g. Apportionment percentage. Divide line 9c by line 9f ................................................................................. 9g. % 10. a. Gross receipts from corporate activities (see instructions) .......... 10a. 00 10. b. Apportioned gross receipts from FTEs ........................................ 10b. 00 11. REQUIRED: Total gross receipts for filing threshold purposes. Multiply line 10a by line 9g, and add line 10b ............................................................................................................................................................ 11. 00 PART 1: CORPORATE INCOME TAX Unitary Business Groups: Amounts reported for all members on Form 4897 must be summed and carried to the corresponding line on Form 4891. 12. Federal taxable income. (Amount includes agricultural activities. See instructions.) ....................................... 12. 00 13. Miscellaneous (see instructions) ..................................................................................................................... 13. 00 14. Adjustments due to decoupling of Michigan depreciation from IRC § 168(k). If adjustment is negative, enter as negative: a. Net bonus depreciation adjustment ............................................. 14a. 00 b. Gain/loss adjustment on sale of eligible depreciable asset(s) ..... 14b. 00 c. Add lines 14a and 14b. If negative, enter as negative.............................................................................. 14c. 00 15. Add lines 12, 13 and 14c. If negative, enter as negative ................................................................................. 15. 00 16. For a UBG, total group eliminations from business income (see instructions). All other filers, enter zero ...... 16. 00 17. Business Income. Subtract line 16 from line 15. (UBGs, see instructions.) If negative, enter as negative ... 17. 00 Additions to Business Income 18. Interest income and dividends derived from obligations or securities of states other than Michigan ................ 18. 00 19. Taxes on or measured by net income including tax imposed under CIT .......................................................... 19. 00 20. Any carryback or carryover of a federal net operating loss (enter as a positive number) ................................. 20. 00 21. Royalty, interest, and other expenses paid to a related person that is not a UBG member of this taxpayer .... 21. 00 22. Expenses from the production of oil and gas, and/or minerals (see instructions) ............................................ 22. 00 23. Miscellaneous (see instructions) ..................................................................................................................... 23. 00 24. Total Additions to Income. Add lines 18 through 23......................................................................................... 24. 00 25. Corporate Income Tax Base After Additions. Add lines 17 and 24. If negative, enter as negative............ 25. 00 + 0000 2022 12 01 27 9 Continue and sign on Page 2