Enlarge image

Michigan Department of Treasury Attachment 07

4577 (Rev. 04-22), Page 1 of 2

2022 MICHIGAN Business Tax Schedule of Shareholders and Officers

For all Corporations claiming the Small Business Alternative or Start-Up Business Credits

Issued under authority of Public Act 36 of 2007.

Taxpayer Name (If Unitary Business Group, Name of Designated Member) Federal Employer Identification Number (FEIN) or TR Number

Unitary Business Groups Only: Name of Unitary Business Group Member Reporting on This Form Federal Employer Identification Number (FEIN) or TR Number

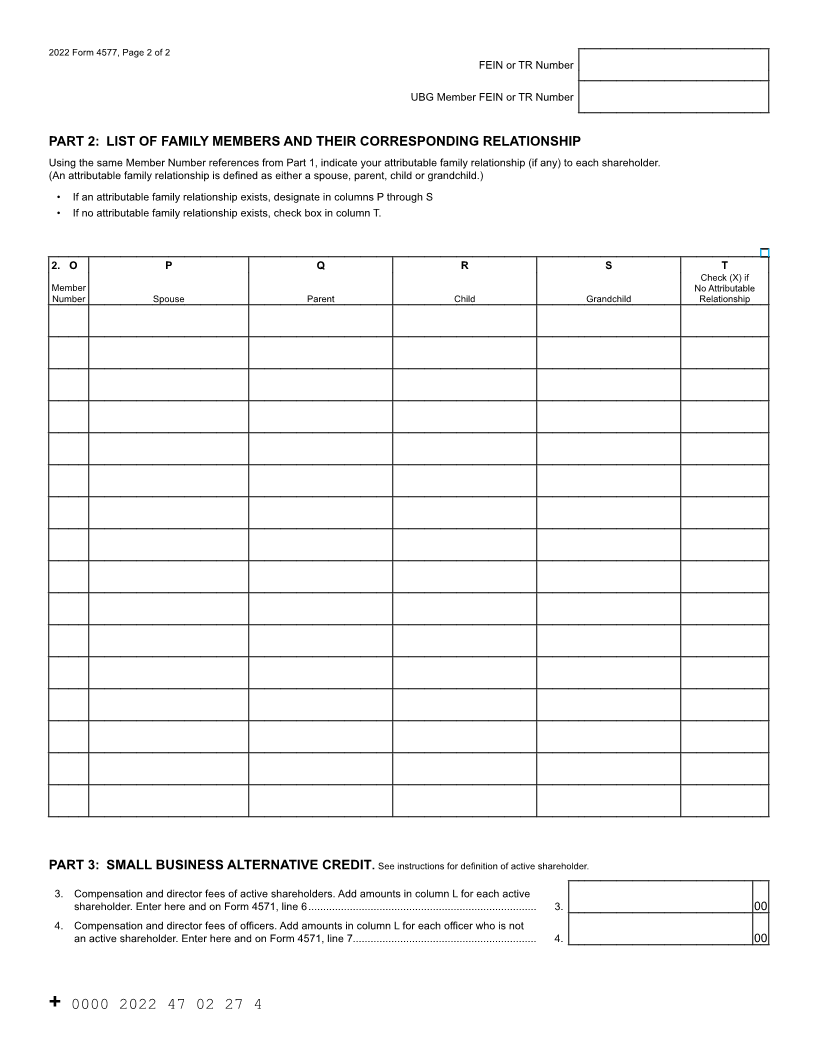

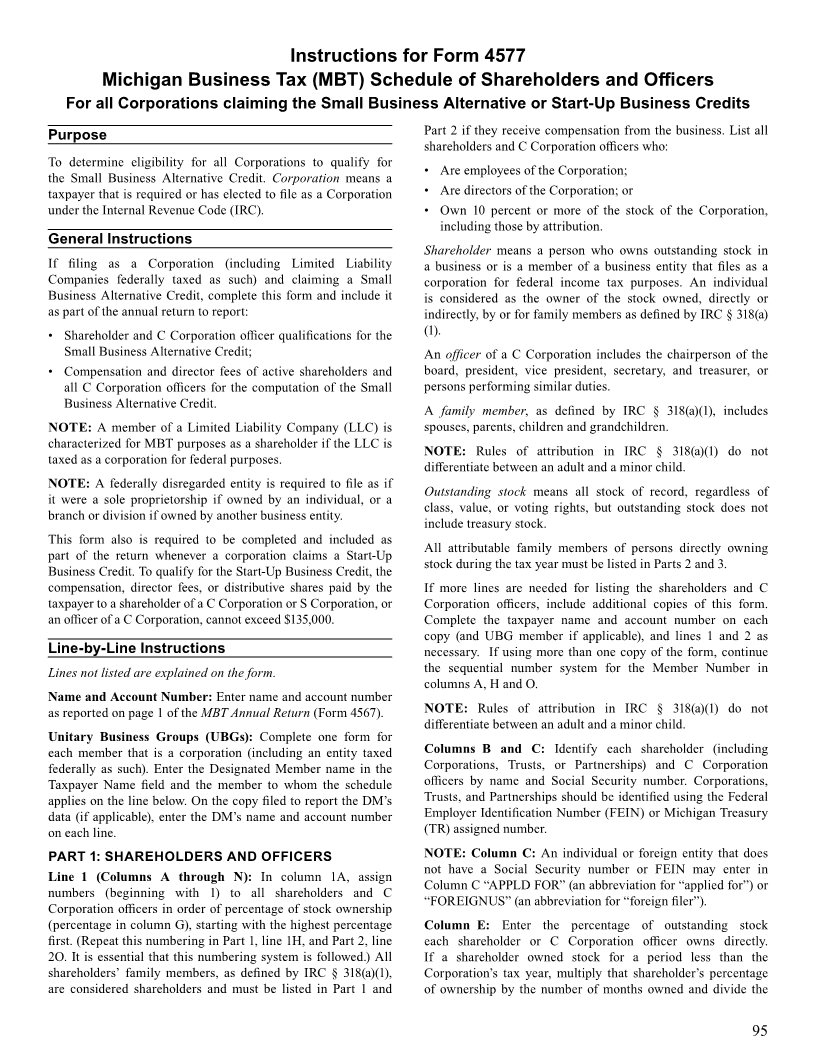

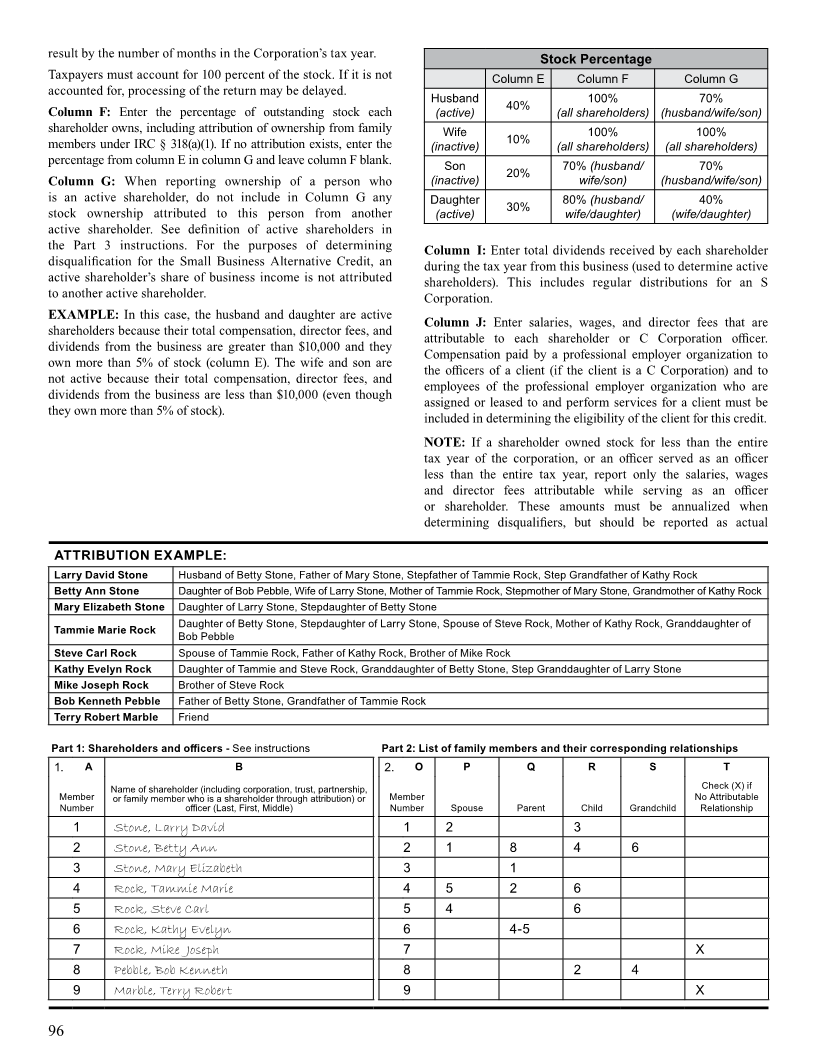

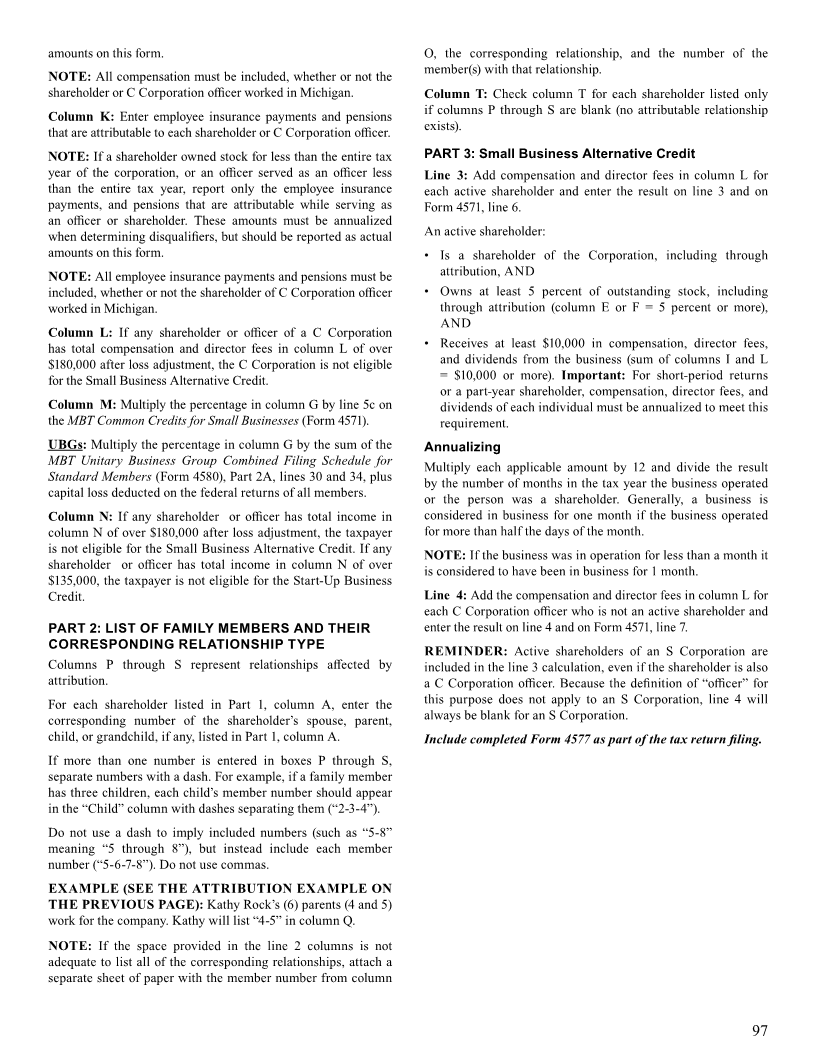

PART 1: SHAREHOLDERS AND OFFICERS. See instructions.

1. A B C D E F G

FEIN or Check % Stock with % Stock from Col. F less

Member Name of shareholder (including corporation, trust, partnership, or family member Social Security number (X) if an % Stock attribution any attribution between

Number who is a shareholder through attribution) or officer (Last, First, Middle) of shareholder or officer officer directly owned (See instructions.) two active shareholders

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

% % %

Percent of stock (not listed above) owned by shareholders who own less than 10% and receive no compensation: %

Total: 100 %

Continue below using the same Member Number references from column 1A.

H I J K L M N

Dividends Total compensation and director

Member (used to determine Salaries, wages and/ Employee insurance fees for officers and/or share- Share of business income/loss Total shareholder/officer

Number active shareholders) or director fees plans, pensions, etc. holders. Add columns J and K. (See instructions.) income. Add columns L and M.

If more space is needed, include additional 4577 forms. Identify taxpayer and complete Part 1 and Part 2 on each additional form. (See instructions.)

+ 0000 2022 47 01 27 6 Continue on Page 2.