Enlarge image

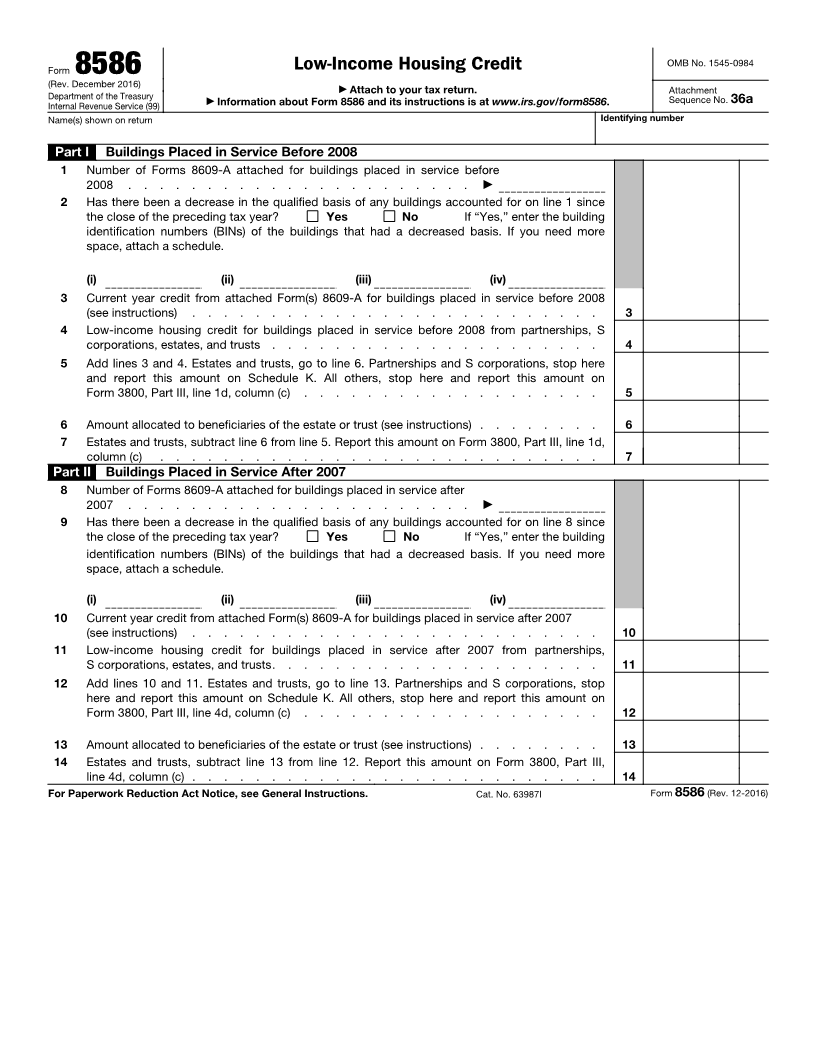

Low-Income Housing Credit OMB No. 1545-0984

Form 8586

(Rev. December 2016) ▶ Attach to your tax return. Attachment

Department of the Treasury ▶ Information about Form 8586 and its instructions is at www.irs.gov/form8586. Sequence No. 36a

Internal Revenue Service (99)

Name(s) shown on return Identifying number

Part I Buildings Placed in Service Before 2008

1 Number of Forms 8609-A attached for buildings placed in service before

2008 . . . . . . . . . . . . . . . . . . . . . . ▶

2 Has there been a decrease in the qualified basis of any buildings accounted for on line 1 since

the close of the preceding tax year? Yes No If “Yes,” enter the building

identification numbers (BINs) of the buildings that had a decreased basis. If you need more

space, attach a schedule.

(i) (ii) (iii) (iv)

3 Current year credit from attached Form(s) 8609-A for buildings placed in service before 2008

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Low-income housing credit for buildings placed in service before 2008 from partnerships, S

corporations, estates, and trusts . . . . . . . . . . . . . . . . . . . . . 4

5 Add lines 3 and 4. Estates and trusts, go to line 6. Partnerships and S corporations, stop here

and report this amount on Schedule K. All others, stop here and report this amount on

Form 3800, Part III, line 1d, column (c) . . . . . . . . . . . . . . . . . . . 5

6 Amount allocated to beneficiaries of the estate or trust (see instructions) . . . . . . . . 6

7 Estates and trusts, subtract line 6 from line 5. Report this amount on Form 3800, Part III, line 1d,

column (c) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Part II Buildings Placed in Service After 2007

8 Number of Forms 8609-A attached for buildings placed in service after

2007 . . . . . . . . . . . . . . . . . . . . . . ▶

9 Has there been a decrease in the qualified basis of any buildings accounted for on line 8 since

the close of the preceding tax year? Yes No If “Yes,” enter the building

identification numbers (BINs) of the buildings that had a decreased basis. If you need more

space, attach a schedule.

(i) (ii) (iii) (iv)

10 Current year credit from attached Form(s) 8609-A for buildings placed in service after 2007

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Low-income housing credit for buildings placed in service after 2007 from partnerships,

S corporations, estates, and trusts. . . . . . . . . . . . . . . . . . . . . 11

12 Add lines 10 and 11. Estates and trusts, go to line 13. Partnerships and S corporations, stop

here and report this amount on Schedule K. All others, stop here and report this amount on

Form 3800, Part III, line 4d, column (c) . . . . . . . . . . . . . . . . . . . 12

13 Amount allocated to beneficiaries of the estate or trust (see instructions) . . . . . . . . 13

14 Estates and trusts, subtract line 13 from line 12. Report this amount on Form 3800, Part III,

line 4d, column (c) . . . . . . . . . . . . . . . . . . . . . . . . . . 14

For Paperwork Reduction Act Notice, see General Instructions. Cat. No. 63987I Form 8586 (Rev. 12-2016)