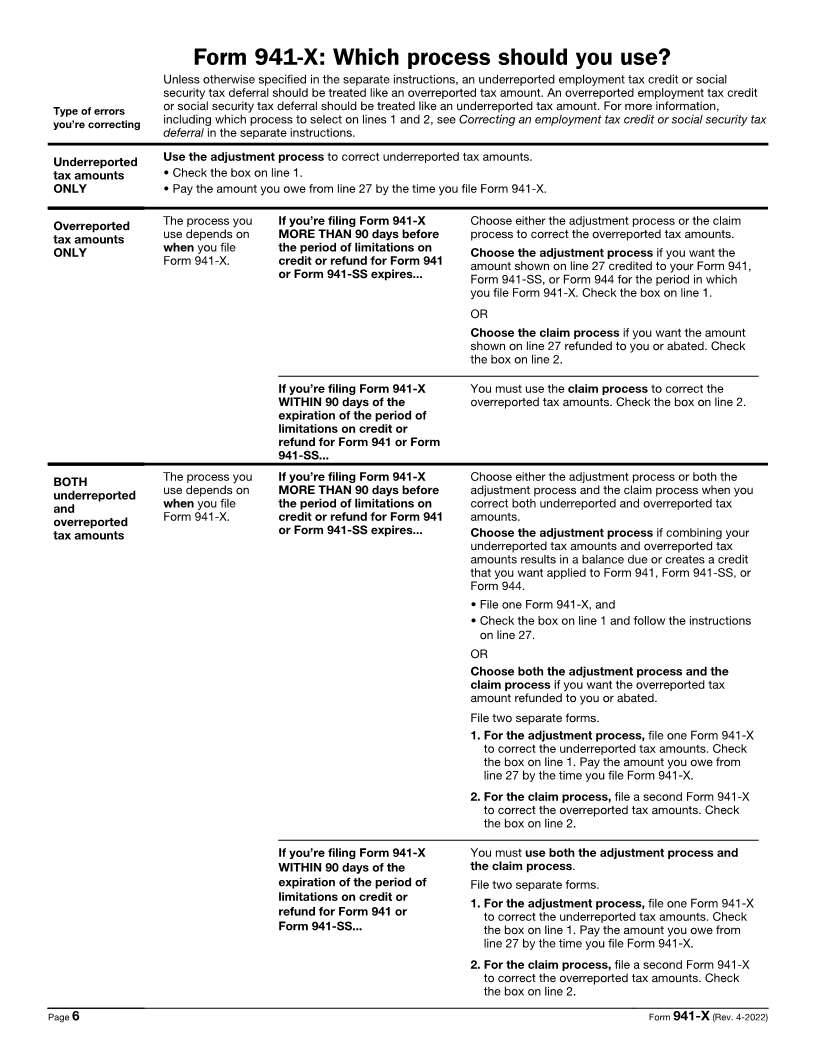

Enlarge image

Form 941-X: Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund

(Rev. April 2022) Department of the Treasury — Internal Revenue Service OMB No. 1545-0029

Employer identification number — Return You’re Correcting...

(EIN)

Check the type of return you’re correcting.

Name (not your trade name) 941

941-SS

Trade name (if any)

Check the ONE quarter you’re correcting.

Address

Number Street Suite or room number 1: January, February, March

2: April, May, June

City State ZIP code 3: July, August, September

4: October, November, December

Foreign country name Foreign province/county Foreign postal code

Read the separate instructions before completing this form. Use this form to correct errors you Enter the calendar year of the

made on Form 941 or 941-SS. Use a separate Form 941-X for each quarter that needs quarter you’re correcting.

correction. Type or print within the boxes. You MUST complete all five pages. Don’t attach this (YYYY)

form to Form 941 or 941-SS unless you’re reclassifying workers; see the instructions for line 42.

Part 1: Select ONLY one process. See page 6 for additional guidance, including information

on how to treat employment tax credits and social security tax deferrals. Enter the date you discovered errors.

1. Adjusted employment tax return. Check this box if you underreported tax amounts. / /

Also check this box if you overreported tax amounts and you would like to use the

adjustment process to correct the errors. You must check this box if you’re correcting (MM / DD / YYYY)

both underreported and overreported tax amounts on this form. The amount shown on

line 27, if less than zero, may only be applied as a credit to your Form 941, Form 941-SS,

or Form 944 for the tax period in which you’re filing this form.

2. Claim. Check this box if you overreported tax amounts only and you would like to use

the claim process to ask for a refund or abatement of the amount shown on line 27.

Don’t check this box if you’re correcting ANY underreported tax amounts on this form.

Part 2: Complete the certifications.

3. I certify that I’ve filed or will file Forms W-2, Wage and Tax Statement, or Forms W-2c, Corrected Wage and Tax Statement,

as required.

Note: If you’re correcting underreported tax amounts only, go to Part 3 on page 2 and skip lines 4 and 5. If you’re correcting overreported

tax amounts, for purposes of the certifications on lines 4 and 5, Medicare tax doesn’t include Additional Medicare Tax. Form 941-X can’t be

used to correct overreported amounts of Additional Medicare Tax unless the amounts weren’t withheld from employee wages or an

adjustment is being made for the current year.

4. If you checked line 1 because you’re adjusting overreported federal income tax, social security tax, Medicare tax, or Additional

Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected federal income tax or Additional Medicare Tax for the current

year and the overcollected social security tax and Medicare tax for current and prior years. For adjustments of employee social

security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating that he

or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

b. The adjustments of social security tax and Medicare tax are for the employer’s share only. I couldn’t find the affected employees or

each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t

claim a refund or credit for the overcollection.

c. The adjustment is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from

employee wages.

5. If you checked line 2 because you’re claiming a refund or abatement of overreported federal income tax, social security tax,

Medicare tax, or Additional Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected social security tax and Medicare tax. For claims of employee

social security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating

that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

b. I have a written consent from each affected employee stating that I may file this claim for the employee’s share of social security

tax and Medicare tax. For refunds of employee social security tax and Medicare tax overcollected in prior years, I also have a

written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a

refund or credit for the overcollection.

c. The claim for social security tax and Medicare tax is for the employer’s share only. I couldn’t find the affected employees, or each

affected employee didn’t give me a written consent to file a claim for the employee’s share of social security tax and Medicare tax,

or each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t

claim a refund or credit for the overcollection.

d. The claim is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from

employee wages.

For Paperwork Reduction Act Notice, see the separate instructions. www.irs.gov/Form941X Cat. No. 17025J Form 941-X (Rev. 4-2022)