- 5 -

Enlarge image

|

Form 5316 (Rev. 12-2021) Page 5

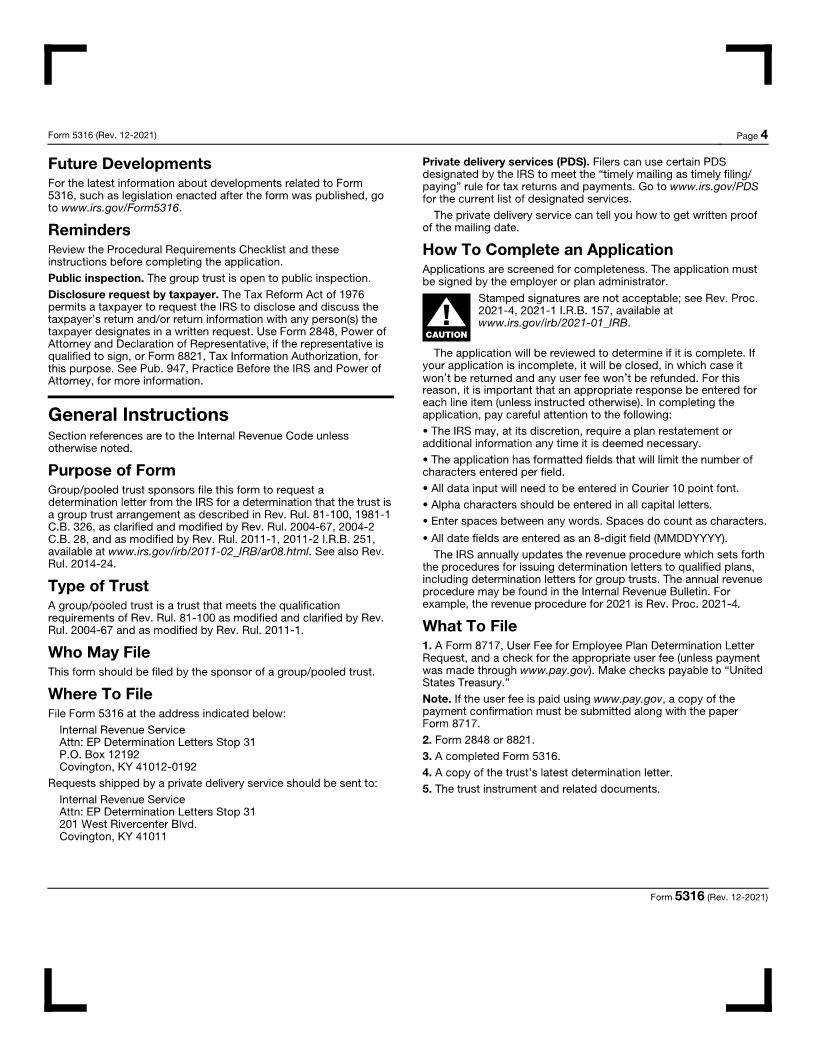

group trust retiree benefit plan may invest directly in the group trust

Specific Instructions or through a separate account maintained by an insurance

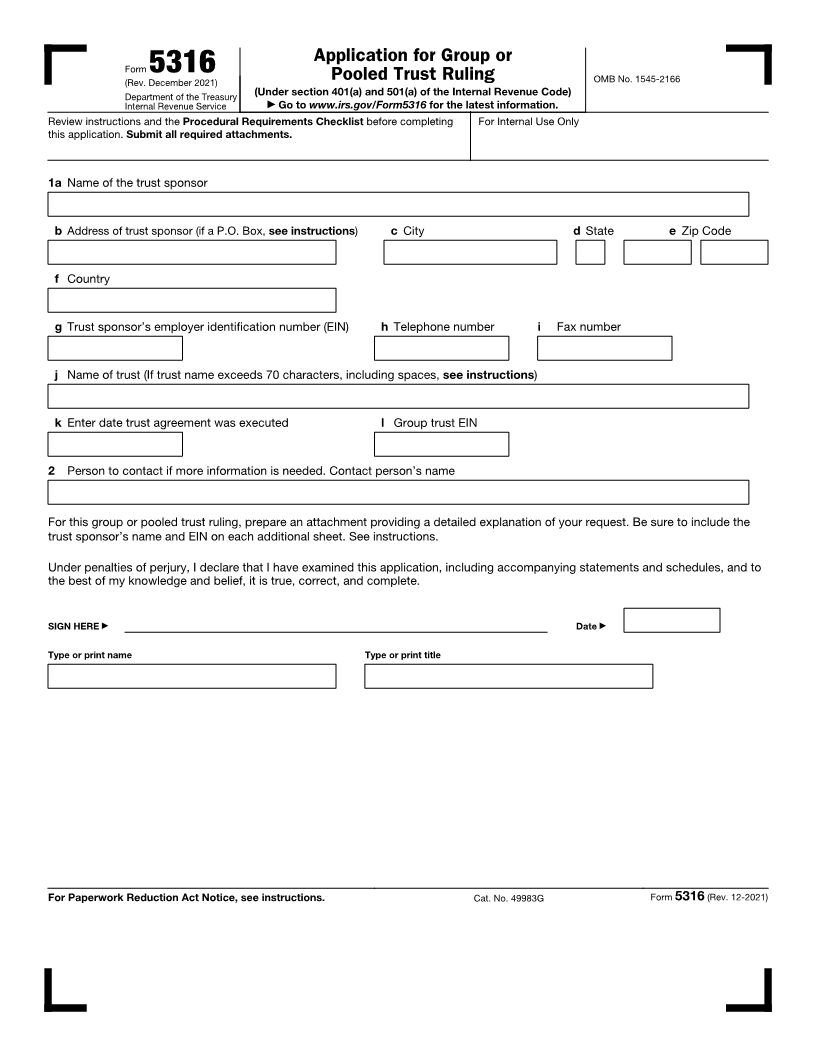

Line 1a and 1b. Enter the name and address of the trust sponsor. company. See Rev. Rul 2014-24. The Path Act section 336(e)

Address should include the suite, room, or other unit number after permits Church Plans to invest in group trusts after December 18,

the street address. If the post office does not deliver mail to the 2015 with the group trust permitted to hold: (1) the assets of a

street address and the plan has a P.O. box, show the box number church plan, and (2) the assets of a church-controlled organization

instead of the street address. The address should be the address of described in IRC section 414(e)(3)(A) if the principal purpose or

the sponsor/employer. function is the administration of the plan described in (1). The assets

eligible for investment in a group trust also include church assets

Line 1g. Enter the 9-digit trust employer identification number (EIN) eligible to be commingled for investment purposes.

assigned to the trust sponsor.

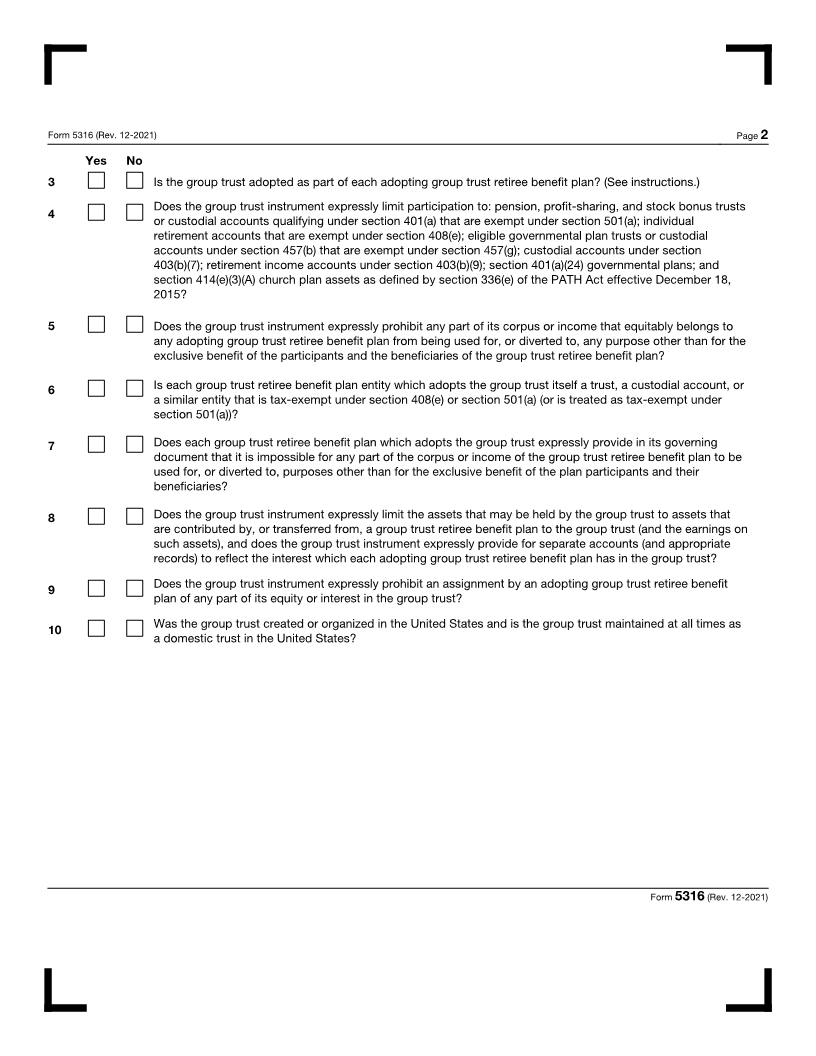

Line 5. The group trust instrument must expressly prohibit any part

The trust sponsor must have an EIN. To apply for an EIN: of its corpus or income that equitably belongs to any adopting

• Online—Generally, a plan sponsor can receive an EIN by Internet group trust retiree benefit plan from being used for, or diverted to,

and use it immediately to file a return. Go to www.irs.gov/EIN. any purpose other than for the exclusive benefit of the participants

• By mail or fax—Send in a completed Form SS-4, Application for and the beneficiaries of the group trust retiree benefit plan. Plan

Employer Identification Number, to apply for an EIN. assets are treated as used for, or diverted to, a purpose other than

for the exclusive benefit of the plan participants or beneficiaries if

Note. This EIN must be used in all subsequent filings of the trust the assets of one group trust retiree benefit plan are used to provide

determination letter requests. benefits under another group trust retiree benefit plan even if the

Line 1j. Due to space restrictions this field is limited to 70 plan participant or beneficiary receiving the benefits is a participant

characters, including spaces. Please complete this item with how or beneficiary under both plans. The Path Act effective December

the trust name should read on the trust determination letter to the 18, 2015 permits assets that are permitted to be commingled with

extent permitted. Due to this restriction, please keep in mind that Church Plan assets to be held in a group trust.

“Employees” and “Trust” are not needed and will be left off if space Line 6. A group trust retiree benefit plan that is a governmental plan

does not permit. for purposes of section 401(a)(24) is treated as meeting the

Line 1k. Enter the date the trust agreement was executed. requirement to be tax exempt if it is not subject to federal income

Line 1l. Identify the EIN of the group trust. Enter “N/A” if the trust taxation.

does not have a separate EIN. Line 7. Each group trust retiree benefit plan which adopts the group

Line 2. Complete this line with the contact person, and attach a trust must expressly provide in its governing document that it is

power of attorney or other written designation. The contact person impossible for any part of the corpus or income of the group trust

will receive copies of all correspondence as authorized. See retiree benefit plan to be used for, or diverted to, purposes other

instructions for Form 2848 or Form 8821. than for the exclusive benefit of the plan participants and their

beneficiaries. For more information see Rev. Rul. 2011-1.

Line 3. A group trust retiree benefit plan is defined as a pension,

profit-sharing, and stock bonus trust or custodial account qualifying Line 8. The group trust instrument must expressly limit the assets

under section 401(a) that is exempt under section 501(a); an that may be held by the group trust to assets that are contributed

individual retirement account that is exempt under section 408(e); by, or transferred from, a group trust retiree benefit plan to the

an eligible governmental plan trust or custodial account under group trust (and the earnings on the assets), and the group trust

section 457(b) that is exempt under section 457(g); a custodial instrument must expressly provide for the separate accounts (and

account under section 403(b)(7); a retirement income account under appropriate records) to reflect the interest which each adopting

section 403(b)(9); a section 401(a)(24) governmental plan; and a group trust retiree benefit plan has in the group trust. This includes

retirement plan that is qualified under the Puerto Rico Code and separate accounting for contributions to the group trust from the

described in section 1022(i)(1) of the Employee Retirement Income adopting plan, disbursements made from the adopting plan's

Security Act of 1974. account in the group trust, and investment experience of the group

trust allocable to that account. A transaction or accounting method

Line 4. The group trust instrument must expressly limit participation which has the effect of directly or indirectly transferring value from

in the group trust to group trust retiree benefit plans. The group the account of one adopting plan into the account of another

trust instrument may also limit participation in the group trust to adopting plan violates this separate accounting requirement.

certain types of group trust retiree benefit plans. For example, the However, a transaction that merely exchanges investments at fair

group trust instrument may limit participation in the group trust to market value between the accounts of one adopting plan to another

pension, profit-sharing, and stock bonus trusts qualifying under account of that adopting plan does not violate this separate

section 401(a) that are exempt under section 501(a), and individual accounting requirement.

retirement accounts exempt under section 408(e). See Rev. Rul.

2011-1 for information on the assets of commingled trust funds. A

Form 5316 (Rev. 12-2021)

|