Enlarge image

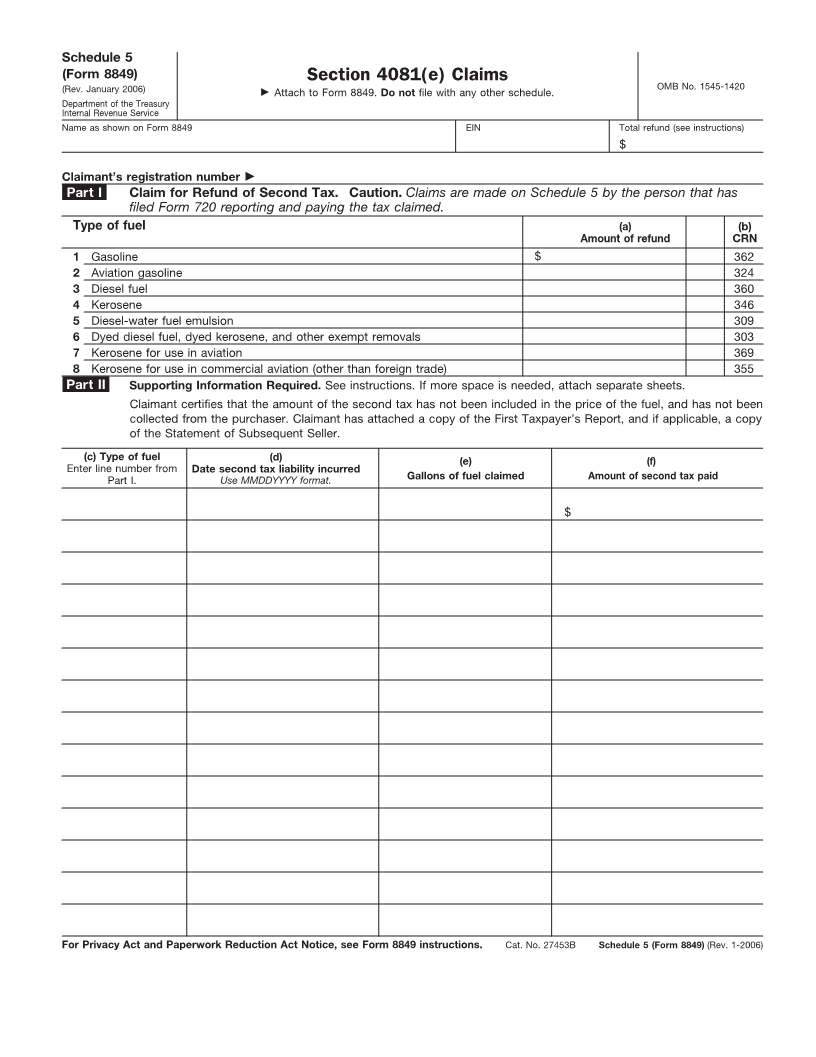

Schedule 5

(Form 8849) Section 4081(e) Claims

(Rev. January 2006) Attach to Form 8849. Do not file with any other schedule. OMB No. 1545-1420

Department of the Treasury

Internal Revenue Service

Name as shown on Form 8849 EIN Total refund (see instructions)

$

Claimant’s registration number

Part I Claim for Refund of Second Tax. Caution. Claims are made on Schedule 5 by the person that has

filed Form 720 reporting and paying the tax claimed.

Type of fuel (a) (b)

Amount of refund CRN

1 Gasoline $ 362

2 Aviation gasoline 324

3 Diesel fuel 360

4 Kerosene 346

5 Diesel-water fuel emulsion 309

6 Dyed diesel fuel, dyed kerosene, and other exempt removals 303

7 Kerosene for use in aviation 369

8 Kerosene for use in commercial aviation (other than foreign trade) 355

Part II Supporting Information Required. See instructions. If more space is needed, attach separate sheets.

Claimant certifies that the amount of the second tax has not been included in the price of the fuel, and has not been

collected from the purchaser. Claimant has attached a copy of the First Taxpayer’s Report, and if applicable, a copy

of the Statement of Subsequent Seller.

(c) Type of fuel (d) (e) (f)

Enter line number from Date second tax liability incurred

Part I. Use MMDDYYYY format. Gallons of fuel claimed Amount of second tax paid

$

For Privacy Act and Paperwork Reduction Act Notice, see Form 8849 instructions. Cat. No. 27453B Schedule 5 (Form 8849) (Rev. 1-2006)