Enlarge image

OMB No. 1545-0177

Casualties and Thefts

Form 4684 Go to www.irs.gov/Form4684 for instructions and the latest information.

Department of the Treasury Attach to your tax return. 2022

Internal Revenue Service Use a separate Form 4684 for each casualty or theft. Attachment

Sequence No. 26

Name(s) shown on tax return Identifying number

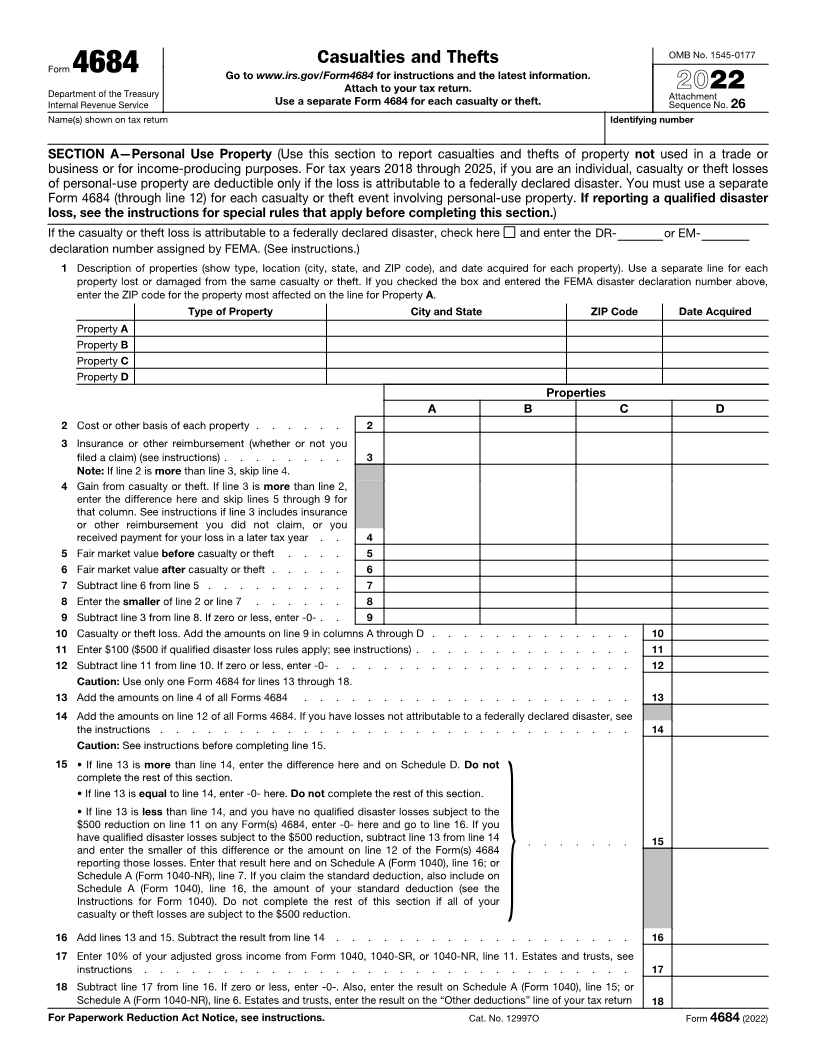

SECTION A—Personal Use Property (Use this section to report casualties and thefts of property not used in a trade or

business or for income-producing purposes. For tax years 2018 through 2025, if you are an individual, casualty or theft losses

of personal-use property are deductible only if the loss is attributable to a federally declared disaster. You must use a separate

Form 4684 (through line 12) for each casualty or theft event involving personal-use property. If reporting a qualified disaster

loss, see the instructions for special rules that apply before completing this section.)

If the casualty or theft loss is attributable to a federally declared disaster, check here and enter the DR- or EM-

declaration number assigned by FEMA. (See instructions.)

1 Description of properties (show type, location (city, state, and ZIP code), and date acquired for each property). Use a separate line for each

property lost or damaged from the same casualty or theft. If you checked the box and entered the FEMA disaster declaration number above,

enter the ZIP code for the property most affected on the line for Property A.

Type of Property City and State ZIP Code Date Acquired

Property A

Property B

Property C

Property D

Properties

A B C D

2 Cost or other basis of each property . . . . . . 2

3 Insurance or other reimbursement (whether or not you

filed a claim) (see instructions) . . . . . . . . 3

Note: If line 2 is more than line 3, skip line 4.

4 Gain from casualty or theft. If line 3 is more than line 2,

enter the difference here and skip lines 5 through 9 for

that column. See instructions if line 3 includes insurance

or other reimbursement you did not claim, or you

received payment for your loss in a later tax year . . 4

5 Fair market value before casualty or theft . . . . 5

6 Fair market value after casualty or theft . . . . . 6

7 Subtract line 6 from line 5 . . . . . . . . . 7

8 Enter the smaller of line 2 or line 7 . . . . . . 8

9 Subtract line 3 from line 8. If zero or less, enter -0- . . 9

10 Casualty or theft loss. Add the amounts on line 9 in columns A through D . . . . . . . . . . . . . 10

11 Enter $100 ($500 if qualified disaster loss rules apply; see instructions) . . . . . . . . . . . . . . 11

12 Subtract line 11 from line 10. If zero or less, enter -0- . . . . . . . . . . . . . . . . . . . 12

Caution: Use only one Form 4684 for lines 13 through 18.

13 Add the amounts on line 4 of all Forms 4684 . . . . . . . . . . . . . . . . . . . . . 13

14 Add the amounts on line 12 of all Forms 4684. If you have losses not attributable to a federally declared disaster, see

the instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Caution: See instructions before completing line 15.

15 • If line 13 is more than line 14, enter the difference here and on Schedule D. Do not

complete the rest of this section.

• If line 13 is equal to line 14, enter -0- here. Do not complete the rest of this section.

• If line 13 is less than line 14, and you have no qualified disaster losses subject to the

$500 reduction on line 11 on any Form(s) 4684, enter -0- here and go to line 16. If you

have qualified disaster losses subject to the $500 reduction, subtract line 13 from line 14 . . . . . . . 15

and enter the smaller of this difference or the amount on line 12 of the Form(s) 4684

reporting those losses. Enter that result here and on Schedule A (Form 1040), line 16; or

Schedule A (Form 1040-NR), line 7. If you claim the standard deduction, also include on

Schedule A (Form 1040), line 16, the amount of your standard deduction (see the

Instructions for Form 1040). Do not complete the rest of this section if all of your

casualty or theft losses are subject to the $500 reduction.

}

16 Add lines 13 and 15. Subtract the result from line 14 . . . . . . . . . . . . . . . . . . . 16

17 Enter 10% of your adjusted gross income from Form 1040, 1040-SR, or 1040-NR, line 11. Estates and trusts, see

instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 Subtract line 17 from line 16. If zero or less, enter -0-. Also, enter the result on Schedule A (Form 1040), line 15; or

Schedule A (Form 1040-NR), line 6. Estates and trusts, enter the result on the “Other deductions” line of your tax return 18

For Paperwork Reduction Act Notice, see instructions. Cat. No. 12997O Form 4684 (2022)