Enlarge image

OMB No. 1545-0074

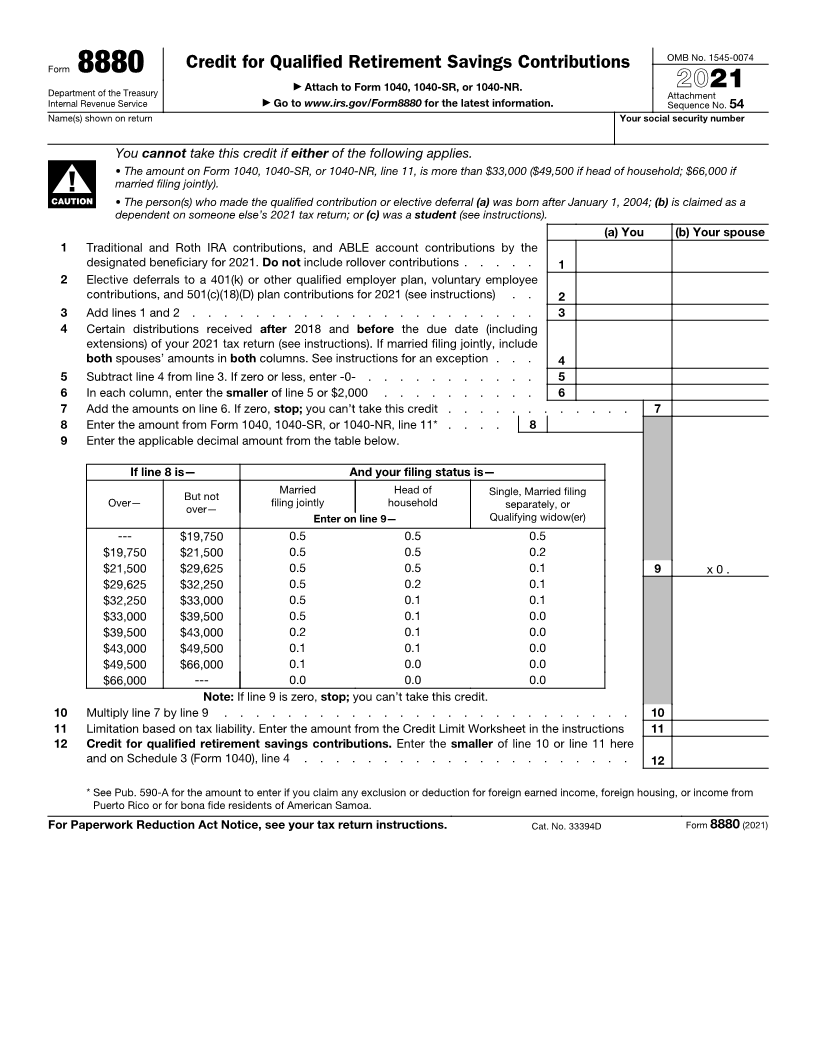

Credit for Qualified Retirement Savings Contributions

Form 8880

▶

Department of the Treasury Attach to Form 1040, 1040-SR, or 1040-NR. 2021

Attachment

Internal Revenue Service ▶ Go to www.irs.gov/Form8880 for the latest information. Sequence No. 54

Name(s) shown on return Your social security number

You cannot take this credit if either of the following applies.

• The amount on Form 1040, 1040-SR, or 1040-NR, line 11, is more than $33,000 ($49,500 if head of household; $66,000 if

married filing jointly).

▲!

CAUTION • The person(s) who made the qualified contribution or elective deferral (a) was born after January 1, 2004; (b) is claimed as a

dependent on someone else’s 2021 tax return; or (c) was a student (see instructions).

(a) You (b) Your spouse

1 Traditional and Roth IRA contributions, and ABLE account contributions by the

designated beneficiary for 2021. Do not include rollover contributions . . . . . 1

2 Elective deferrals to a 401(k) or other qualified employer plan, voluntary employee

contributions, and 501(c)(18)(D) plan contributions for 2021 (see instructions) . . 2

3 Add lines 1 and 2 . . . . . . . . . . . . . . . . . . . . . . 3

4 Certain distributions received after 2018 and before the due date (including

extensions) of your 2021 tax return (see instructions). If married filing jointly, include

both spouses’ amounts in both columns. See instructions for an exception . . . 4

5 Subtract line 4 from line 3. If zero or less, enter -0- . . . . . . . . . . . 5

6 In each column, enter the smaller of line 5 or $2,000 . . . . . . . . . . 6

7 Add the amounts on line 6. If zero, stop; you can’t take this credit . . . . . . . . . . . . 7

8 Enter the amount from Form 1040, 1040-SR, or 1040-NR, line 11* . . . . 8

9 Enter the applicable decimal amount from the table below.

If line 8 is— And your filing status is—

Married Head of Single, Married filing

Over— But not filing jointly household separately, or

over—

Enter on line 9— Qualifying widow(er)

--- $19,750 0.5 0.5 0.5

$19,750 $21,500 0.5 0.5 0.2

$21,500 $29,625 0.5 0.5 0.1 9 x 0 .

$29,625 $32,250 0.5 0.2 0.1

$32,250 $33,000 0.5 0.1 0.1

$33,000 $39,500 0.5 0.1 0.0

$39,500 $43,000 0.2 0.1 0.0

$43,000 $49,500 0.1 0.1 0.0

$49,500 $66,000 0.1 0.0 0.0

$66,000 --- 0.0 0.0 0.0

Note: If line 9 is zero, stop; you can’t take this credit.

10 Multiply line 7 by line 9 . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Limitation based on tax liability. Enter the amount from the Credit Limit Worksheet in the instructions 11

12 Credit for qualified retirement savings contributions. Enter the smaller of line 10 or line 11 here

and on Schedule 3 (Form 1040), line 4 . . . . . . . . . . . . . . . . . . . . . 12

* See Pub. 590-A for the amount to enter if you claim any exclusion or deduction for foreign earned income, foreign housing, or income from

Puerto Rico or for bona fide residents of American Samoa.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 33394D Form 8880 (2021)