Enlarge image

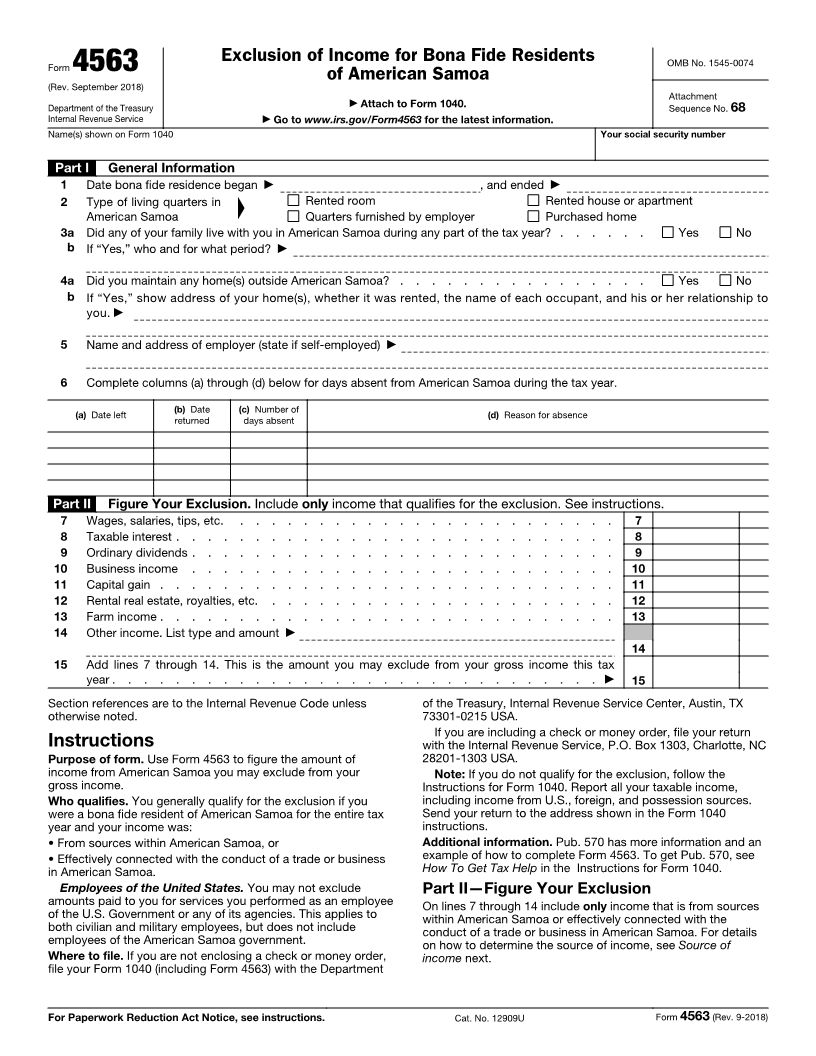

Exclusion of Income for Bona Fide Residents OMB No. 1545-0074

Form 4563 of American Samoa

(Rev. September 2018)

Attachment

Department of the Treasury ▶ Attach to Form 1040. Sequence No. 68

Internal Revenue Service ▶ Go to www.irs.gov/Form4563 for the latest information.

Name(s) shown on Form 1040 Your social security number

Part I General Information

1 Date bona fide residence began ▲ ▶ , and ended ▶

2 Type of living quarters in Rented room Rented house or apartment

American Samoa Quarters furnished by employer Purchased home

3 a Did any of your family live with you in American Samoa during any part of the tax year? . . . . . . Yes No

b If “Yes,” who and for what period? ▶

4 a Did you maintain any home(s) outside American Samoa? . . . . . . . . . . . . . . . . Yes No

b If “Yes,” show address of your home(s), whether it was rented, the name of each occupant, and his or her relationship to

you. ▶

5 Name and address of employer (state if self-employed) ▶

6 Complete columns (a) through (d) below for days absent from American Samoa during the tax year.

(a) Date left (b) Date (c) Number of (d) Reason for absence

returned days absent

Part II Figure Your Exclusion. Include only income that qualifies for the exclusion. See instructions.

7 Wages, salaries, tips, etc. . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Taxable interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9 Ordinary dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 Business income . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Capital gain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

12 Rental real estate, royalties, etc. . . . . . . . . . . . . . . . . . . . . . . 12

13 Farm income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Other income. List type and amount ▶

14

15 Add lines 7 through 14. This is the amount you may exclude from your gross income this tax

year. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ 15

Section references are to the Internal Revenue Code unless of the Treasury, Internal RevenueService Center, Austin, TX

otherwise noted. 73301-0215 USA.

If you are including a check or money order, file your return

Instructions with the Internal Revenue Service, P.O. Box 1303, Charlotte, NC

Purpose of form. Use Form 4563 to figure the amount of 28201-1303 USA.

income from American Samoa you may exclude from your Note: If you do not qualify for the exclusion, follow the

gross income. Instructions for Form 1040. Report all your taxable income,

Who qualifies. You generally qualify for the exclusion if you including income from U.S., foreign, and possession sources.

were a bona fide resident of American Samoa for the entire tax Send your return to the address shown in the Form 1040

year and your income was: instructions.

• From sources within American Samoa, or Additional information. Pub. 570 has more information and an

• Effectively connected with the conduct of a trade or business example of how to complete Form 4563. To get Pub. 570, see

in American Samoa. How To Get Tax Help in the Instructions for Form 1040.

Employees of the United States. You may not exclude Part II—Figure Your Exclusion

amounts paid to you for services you performed as anemployee On lines 7 through 14 include only income that is from sources

of the U.S. Government or any of its agencies. This applies to within American Samoa or effectively connected with the

both civilian and military employees, but does not include conduct of a trade or business in American Samoa. For details

employees of the American Samoa government. on how to determine the source of income, see Source of

Where to file. If you are not enclosing a check or moneyorder, income next.

file your Form 1040 (including Form 4563)with the Department

For Paperwork Reduction Act Notice, see instructions. Cat. No. 12909U Form 4563 (Rev. 9-2018)