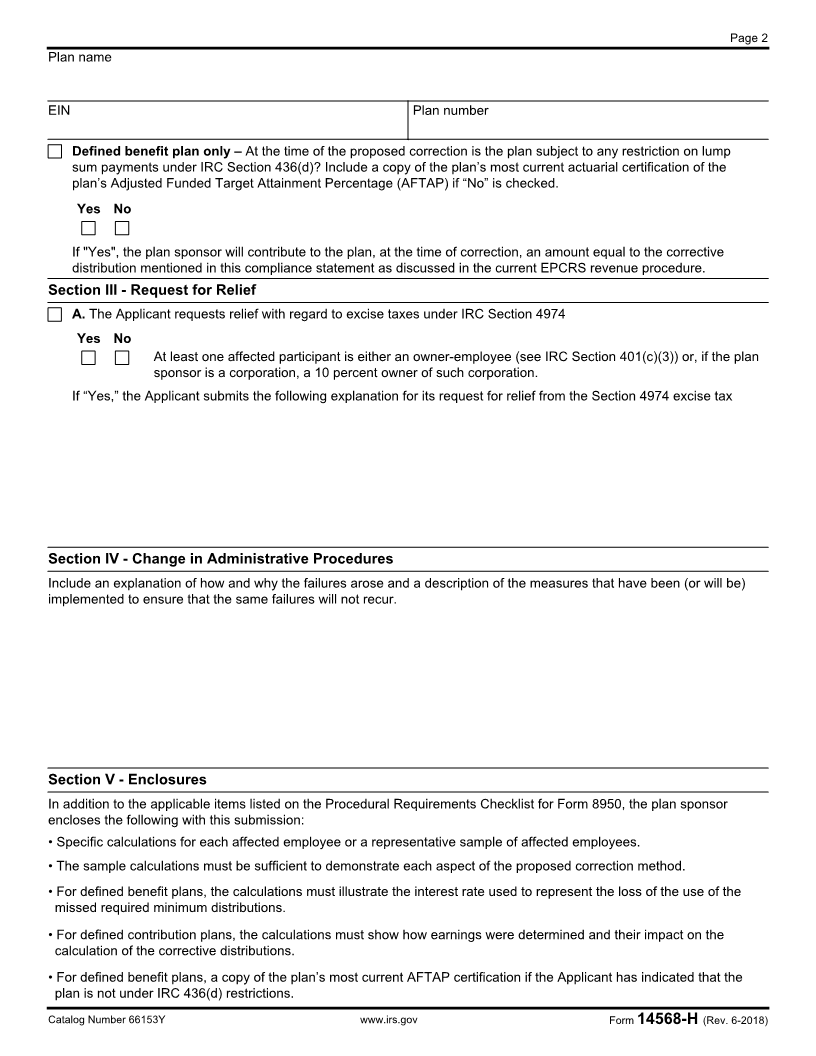

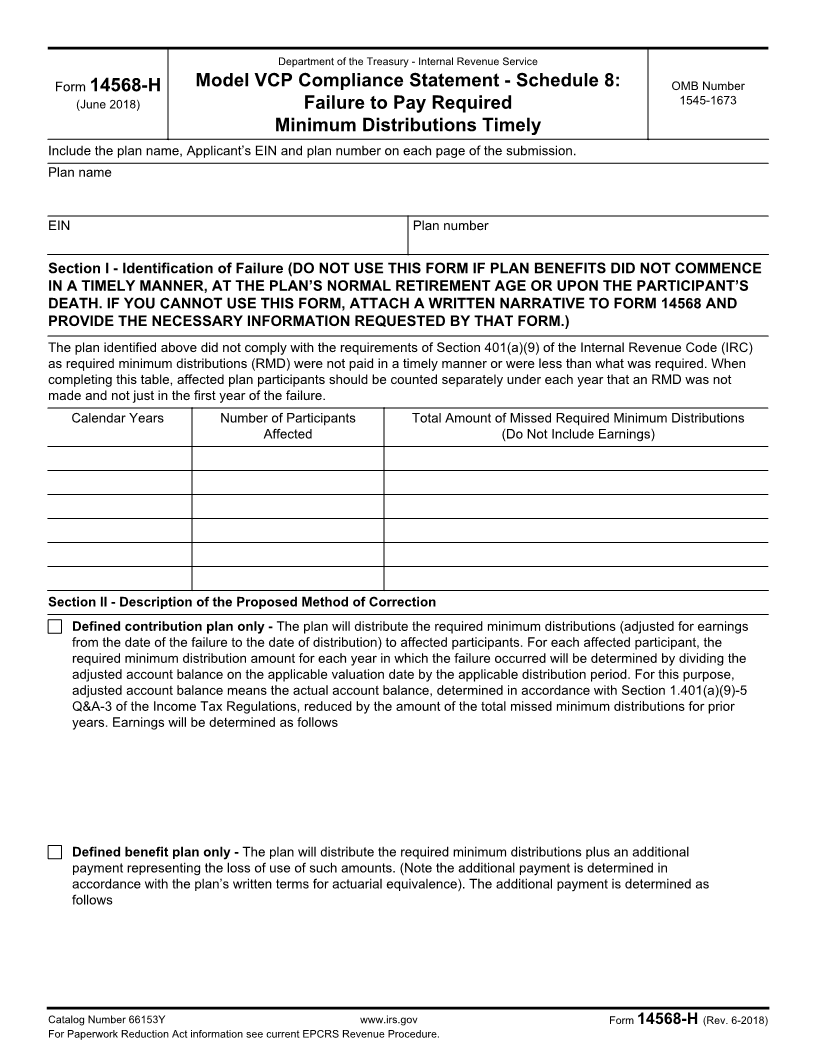

Enlarge image

Department of the Treasury - Internal Revenue Service

Form 14568-H Model VCP Compliance Statement - Schedule 8: OMB Number

1545-1673

(June 2018) Failure to Pay Required

Minimum Distributions Timely

Include the plan name, Applicant’s EIN and plan number on each page of the submission.

Plan name

EIN Plan number

Section I - Identification of Failure (DO NOT USE THIS FORM IF PLAN BENEFITS DID NOT COMMENCE

IN A TIMELY MANNER, AT THE PLAN’S NORMAL RETIREMENT AGE OR UPON THE PARTICIPANT’S

DEATH. IF YOU CANNOT USE THIS FORM, ATTACH A WRITTEN NARRATIVE TO FORM 14568 AND

PROVIDE THE NECESSARY INFORMATION REQUESTED BY THAT FORM.)

The plan identified above did not comply with the requirements of Section 401(a)(9) of the Internal Revenue Code (IRC)

as required minimum distributions (RMD) were not paid in a timely manner or were less than what was required. When

completing this table, affected plan participants should be counted separately under each year that an RMD was not

made and not just in the first year of the failure.

Calendar Years Number of Participants Total Amount of Missed Required Minimum Distributions

Affected (Do Not Include Earnings)

Section II - Description of the Proposed Method of Correction

Defined contribution plan only - The plan will distribute the required minimum distributions (adjusted for earnings

from the date of the failure to the date of distribution) to affected participants. For each affected participant, the

required minimum distribution amount for each year in which the failure occurred will be determined by dividing the

adjusted account balance on the applicable valuation date by the applicable distribution period. For this purpose,

adjusted account balance means the actual account balance, determined in accordance with Section 1.401(a)(9)-5

Q&A-3 of the Income Tax Regulations, reduced by the amount of the total missed minimum distributions for prior

years. Earnings will be determined as follows

Defined benefit plan only - The plan will distribute the required minimum distributions plus an additional

payment representing the loss of use of such amounts. (Note the additional payment is determined in

accordance with the plan’s written terms for actuarial equivalence). The additional payment is determined as

follows

Catalog Number 66153Y www.irs.gov Form 14568-H (Rev. 6-2018)

For Paperwork Reduction Act information see current EPCRS Revenue Procedure.