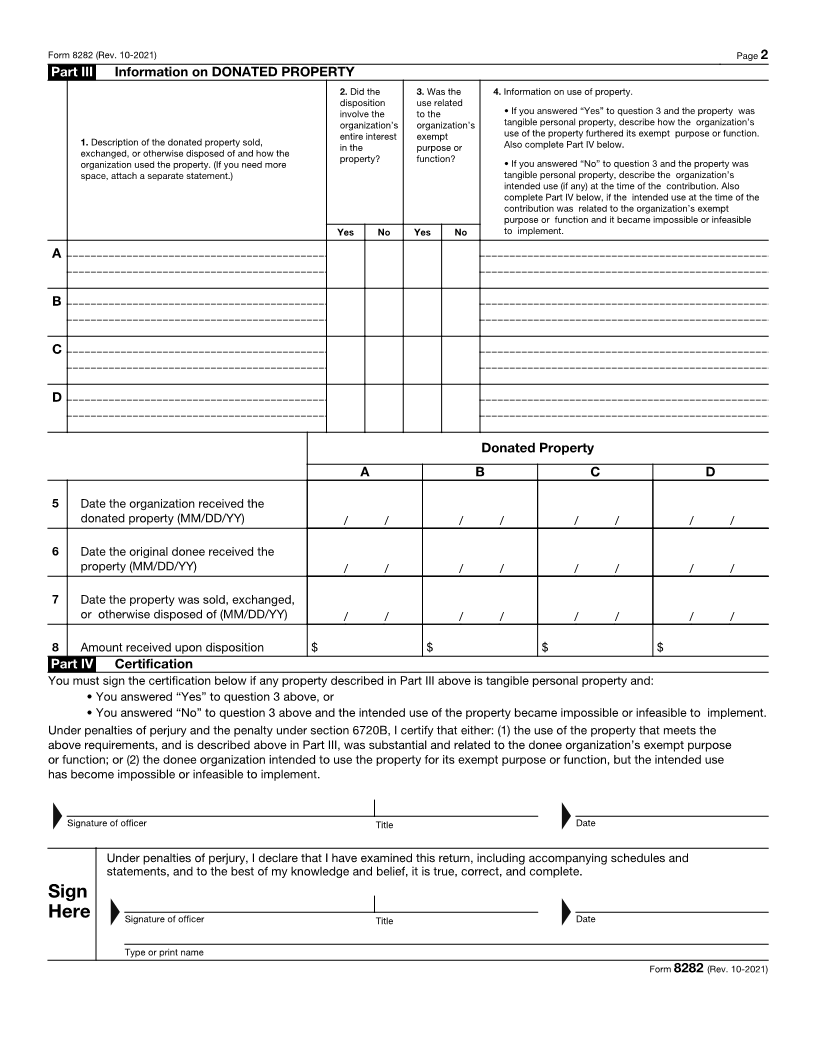

Enlarge image

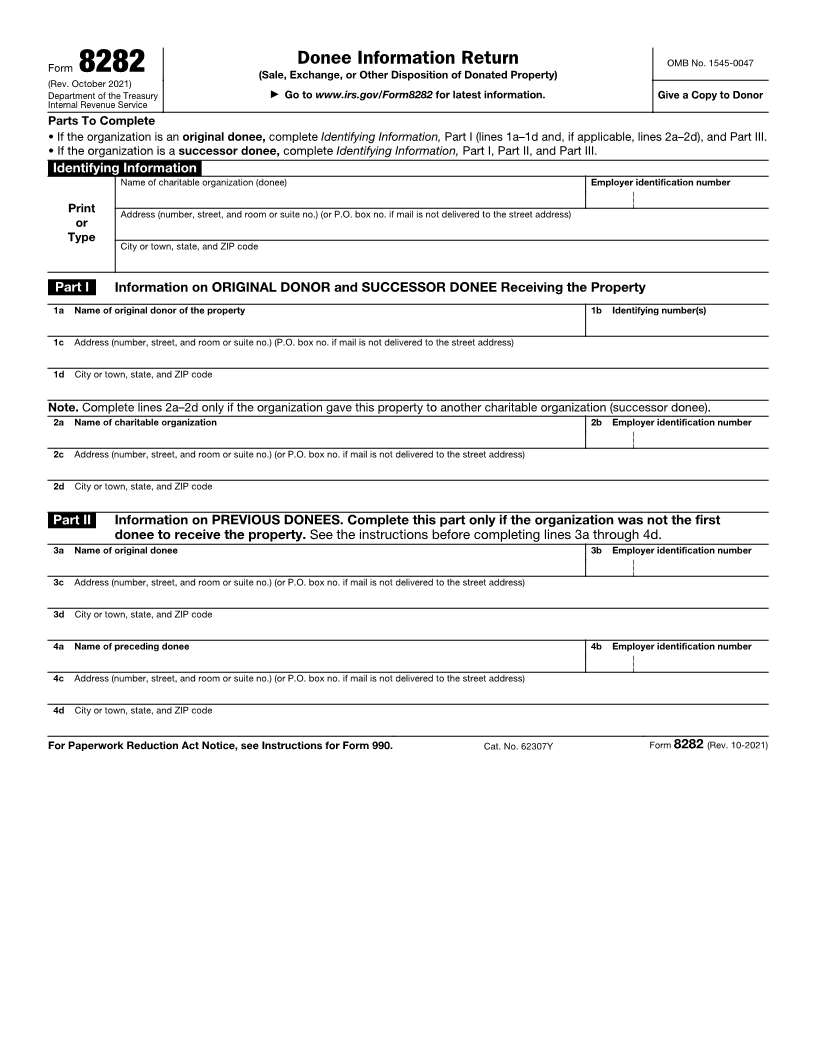

Donee Information Return OMB No. 1545-0047

Form 8282 (Sale, Exchange, or Other Disposition of Donated Property)

(Rev. October 2021)

Department of the Treasury ▶ Go to www.irs.gov/Form8282 for latest information. Give a Copy to Donor

Internal Revenue Service

Parts To Complete

• If the organization is an original donee, complete Identifying Information, Part I (lines 1a–1d and, if applicable, lines 2a–2d), and Part III.

• If the organization is a successor donee, complete Identifying Information, Part I, Part II, and Part III.

Identifying Information

Name of charitable organization (donee) Employer identification number

Print Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

or

Type

City or town, state, and ZIP code

Part I Information on ORIGINAL DONOR and SUCCESSOR DONEE Receiving the Property

1a Name of original donor of the property 1b Identifying number(s)

1c Address (number, street, and room or suite no.) (P.O. box no. if mail is not delivered to the street address)

1d City or town, state, and ZIP code

Note. Complete lines 2a–2d only if the organization gave this property to another charitable organization (successor donee).

2a Name of charitable organization 2b Employer identification number

2c Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

2d City or town, state, and ZIP code

Part II Information on PREVIOUS DONEES. Complete this part only if the organization was not the first

donee to receive the property. See the instructions before completing lines 3a through 4d.

3a Name of original donee 3b Employer identification number

3c Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

3d City or town, state, and ZIP code

4a Name of preceding donee 4b Employer identification number

4c Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

4d City or town, state, and ZIP code

For Paperwork Reduction Act Notice, see Instructions for Form 990. Cat. No. 62307Y Form 8282 (Rev. 10-2021)