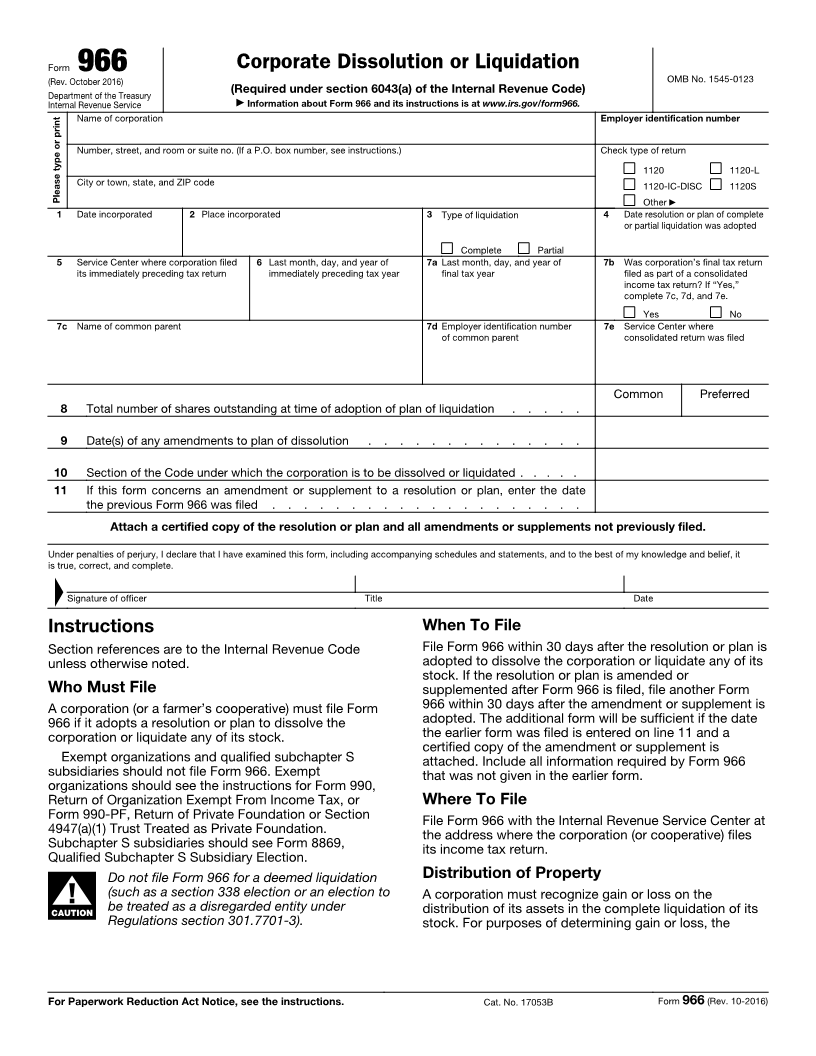

Enlarge image

Corporate Dissolution or Liquidation

Form 966 OMB No. 1545-0123

(Rev. October 2016)

Department of the Treasury (Required under section 6043(a) of the Internal Revenue Code)

Internal Revenue Service ▶ Information about Form 966 and its instructions is at www.irs.gov/form966.

Name of corporation Employer identification number

Number, street, and room or suite no. (If a P.O. box number, see instructions.) Check type of return

1120 1120-L

City or town, state, and ZIP code 1120-IC-DISC 1120S

Please type or print Other ▶

1 Date incorporated 2 Place incorporated 3 Type of liquidation 4 Date resolution or plan of complete

or partial liquidation was adopted

Complete Partial

5 Service Center where corporation filed 6 Last month, day, and year of 7a Last month, day, and year of 7b Was corporation’s final tax return

its immediately preceding tax return immediately preceding tax year final tax year filed as part of a consolidated

income tax return? If “Yes,”

complete 7c, 7d, and 7e.

Yes No

7c Name of common parent 7d Employer identification number 7e Service Center where

of common parent consolidated return was filed

Common Preferred

8 Total number of shares outstanding at time of adoption of plan of liquidation . . . . .

9 Date(s) of any amendments to plan of dissolution . . . . . . . . . . . . . .

10 Section of the Code under which the corporation is to be dissolved or liquidated . . . . .

11 If this form concerns an amendment or supplement to a resolution or plan, enter the date

the previous Form 966 was filed . . . . . . . . . . . . . . . . . . . .

Attach a certified copy of the resolution or plan and all amendments or supplements not previously filed.

Under penalties of perjury, I declare that I have examined this form, including accompanying schedules and statements, and to the best of my knowledge and belief, it

is▲true, correct, and complete.

Signature of officer Title Date

Instructions When To File

Section references are to the Internal Revenue Code File Form 966 within 30 days after the resolution or plan is

unless otherwise noted. adopted to dissolve the corporation or liquidate any of its

stock. If the resolution or plan is amended or

Who Must File supplemented after Form 966 is filed, file another Form

A corporation (or a farmer’s cooperative) must file Form 966 within 30 days after the amendment or supplement is

966 if it adopts a resolution or plan to dissolve the adopted. The additional form will be sufficient if the date

corporation or liquidate any of its stock. the earlier form was filed is entered on line 11 and a

certified copy of the amendment or supplement is

Exempt organizations and qualified subchapter S attached. Include all information required by Form 966

subsidiaries should not file Form 966. Exempt that was not given in the earlier form.

organizations should see the instructions for Form 990,

Return of Organization Exempt From Income Tax, or Where To File

Form 990-PF, Return of Private Foundation or Section File Form 966 with the Internal Revenue Service Center at

4947(a)(1) Trust Treated as Private Foundation. the address where the corporation (or cooperative) files

Subchapter S subsidiaries should see Form 8869, its income tax return.

Qualified Subchapter S Subsidiary Election.

Do not file Form 966 for a deemed liquidation Distribution of Property

(such as a section 338 election or an election to A corporation must recognize gain or loss on the

▲! be treated as a disregarded entity under distribution of its assets in the complete liquidation of its

CAUTION

Regulations section 301.7701-3). stock. For purposes of determining gain or loss, the

For Paperwork Reduction Act Notice, see the instructions. Cat. No. 17053B Form 966 (Rev. 10-2016)