- 4 -

Enlarge image

|

Form 4461-A (Rev. 11-2019) Page 4

Flexible plan. A flexible plan is a plan A provider also includes any person If multiple adoption agreements are

submitted by a mass submitter which that has an established place of linked to the same basic plan document,

contains certainoptional provisions as business in the United States where it is the same two-digit basic plan document

allowed by section 10.03(1) of Rev. Proc. accessible during every business day number should be used for all

2017-41. Providers that adopta flexible and offers a plan as a word-for-word applications.

plan may include or delete any optional identical adopter or minor modifier Line 5b. Enter the three-digit number

provision designated as such in the adopter of a plan of a mass submitter, you have assigned to the adoption

mass submitter’s plan. A flexible plan regardless of the number of employers agreement for which this application is

adopted by a provider which differsfrom that are expected to adopt the plan. submitted. Each different adoption

the mass submitter plan onlybecause of Standardized plan. A standardized plan agreement designed to accompany a

the deletion of certainoptional is a pre-approved plan (other than a single basic plan document should be

provisions will be treated as a plan that statutory hybrid plan) that meets the given a different three-digit number

isword-for-word identical to the mass requirements set forth in section 5.16 of beginning with “001.” For example, if the

submitter plan. Rev. Proc. 2017-41. first basic plan document of a sponsor

Mass submitter. As set forth in Rev. Nonstandardized plan. A has four different adoption agreements,

Proc. 2017-41, any entity that submits nonstandardized plan is a pre-approved they should be numbered “001” through

applications on behalf of at least 30 plan that isn’t a standardized plan and “004,” and the provider should submit

unaffiliated providers each of which is that satisfies section 5.15 of Rev. Proc. four separate Forms 4461-A. Adoption

sponsoring, on a word-for-word identical 2017-41. agreements submitted with the second

basis, the same plan is a mass or any subsequent basic plan

submitter. A mass submitter is treated as Statutory hybrid plan. A statutory documents (that aren’t word-for-word

a mass submitter with respect to all of its hybrid plan is a defined benefit plan that identical to a previously submitted basic

plans, provided the 30-unaffiliated- contains a statutory hybrid benefit plan document) should be similarly

provider requirement is met with respect formula, as defined in Regulations numbered beginning with “001.”

to at least one plan. section 1.411(a)(13)-1(d)(4). Section 6.03

of Rev. Proc. 2017-41 (as revised by Line 9. Procedural requirements.

Affiliation is determined under sections Rev. Proc. 2018-21, 2018-14 I.R.B. 467) Submit a separate application for each

414(b) and (c). Additionally, the following provides a list of areas not covered by different plan/adoption agreement

will be considered to be affiliated: any opinion letters. This list includes combination or single document plan.

law firm, accounting firm, consulting statutory hybrid plans with certain Line 9c. If you checked “Yes,” submit a

firm, etc., with its partners, members, features, such as a statutory hybrid copy of such plan with language

associates, etc. For purposes of benefit formula that isn’t a cash balance differences highlighted. Attach a cover

determining whether 30 unaffiliated formula. See section 6.03 of Rev. Proc. letter that includes the following.

providers sponsor on a word-for-word 2017-41 for the complete list. • The name and file folder number of the

identical basis the same plan document,

the mass submitter is treated as an plan, including the name and EIN of the

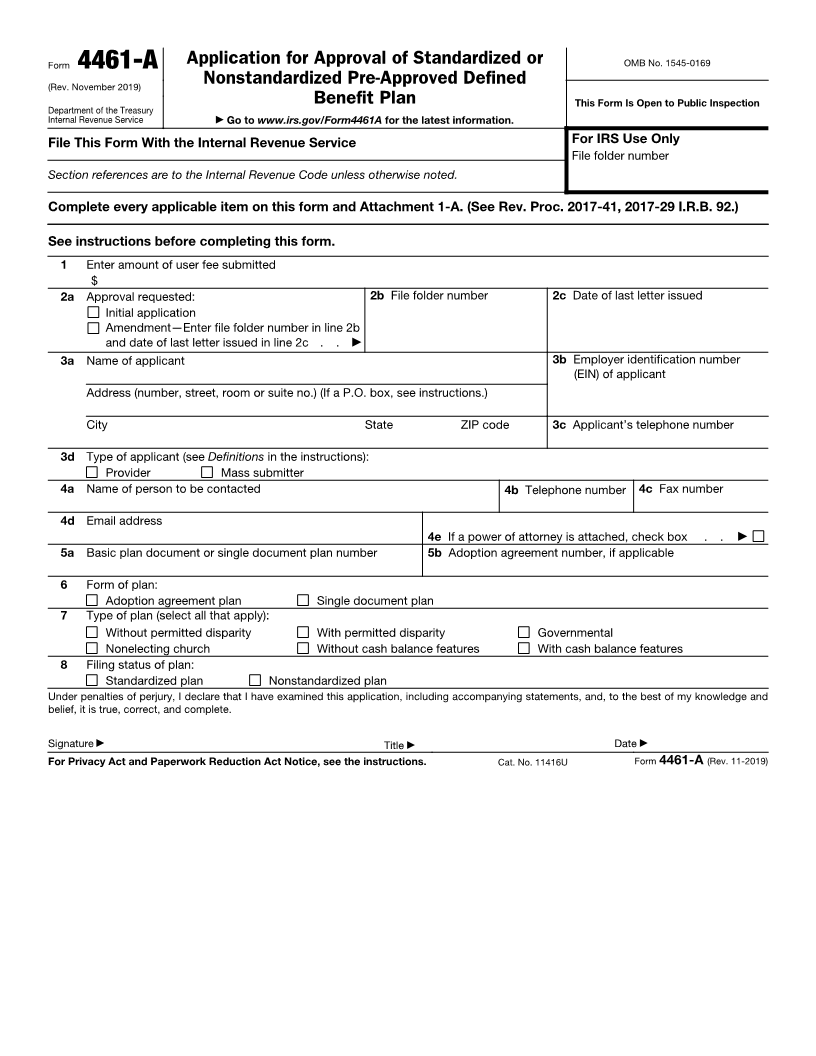

unaffiliated provider. Specific Instructions provider.

Pre-approved plan. A pre-approved Line 1. All applications submitted must • A list of all plans written by the plan

plan is a plan (including a plan covering be accompanied by the appropriate user drafter that are substantially identical to

self-employed individuals) that is made fee and Form 8717-A, User Fee for the lead plan, including the information

available by a provider for adoption by Employee Plan Opinion Letter Request, described above.

employers. The term pre-approved plan as determined from the schedule in Rev. • A description of each place where the

includes both standardized and Proc. 2019-4, 2019-1 I.R.B. 146 (or the plan for which the application is being

nonstandardized plans. A pre-approved latest annual update). Applications submitted isn’t word-for-word identical

plan may be an adoption agreement plan submitted without the proper user fee to the language of the lead plan,

or a single document plan. An adoption won’t be processed and will be returned including an explanation of the purpose

agreement plan consists of a basic plan to the applicant. and effect of each difference.

document and an adoption agreement. A Line 3a. Enter the name and address of • A certification made under penalty of

single document plan consists of a the applicant. If the Post Office doesn’t perjury by the plan drafter that the

single plan document offered by a deliver mail to the street address and information describing where the plan

provider without an adoption agreement. the applicant has a P.O. box number, language isn’t word-for-word identical is

Provider. A provider is any person show the P.O. box number instead of the true and complete.

(including a mass submitter, if street address. Line 9e. In addition to filing Form

applicable) that (1) has an established Line 4a. If the person to be contacted is 4461-A, the mass submitter should use

place of business in the United States other than an employee of the applicant, Form 4461-B, when submitting

where it is accessible during every please enclose an authorized power of applications on behalf of its adopting

business day; and (2) represents to the attorney. See Disclosure requested by providers, and submit Form 8717-A.

IRS that it has at least 15 employer- taxpayer, earlier.

clients, each of which is reasonably

expected to adopt the same pre- Line 4c. Enter a fax number to receive

approved plan of the provider. notice of preliminary approval of the

applicable plan, subject to final approval

A provider may request an opinion by opinion letter.

letter for more than one plan provided it

represents to the IRS that it has at least Line 5a. Enter the two-digit number you

30 employer-clients in the aggregate, have assigned to your single document

each of which is reasonably expected to plan or basic plan document that

adopt at least one of the provider’s accompanies theadoption agreement

plans. for which you arerequesting approval.

|