Enlarge image

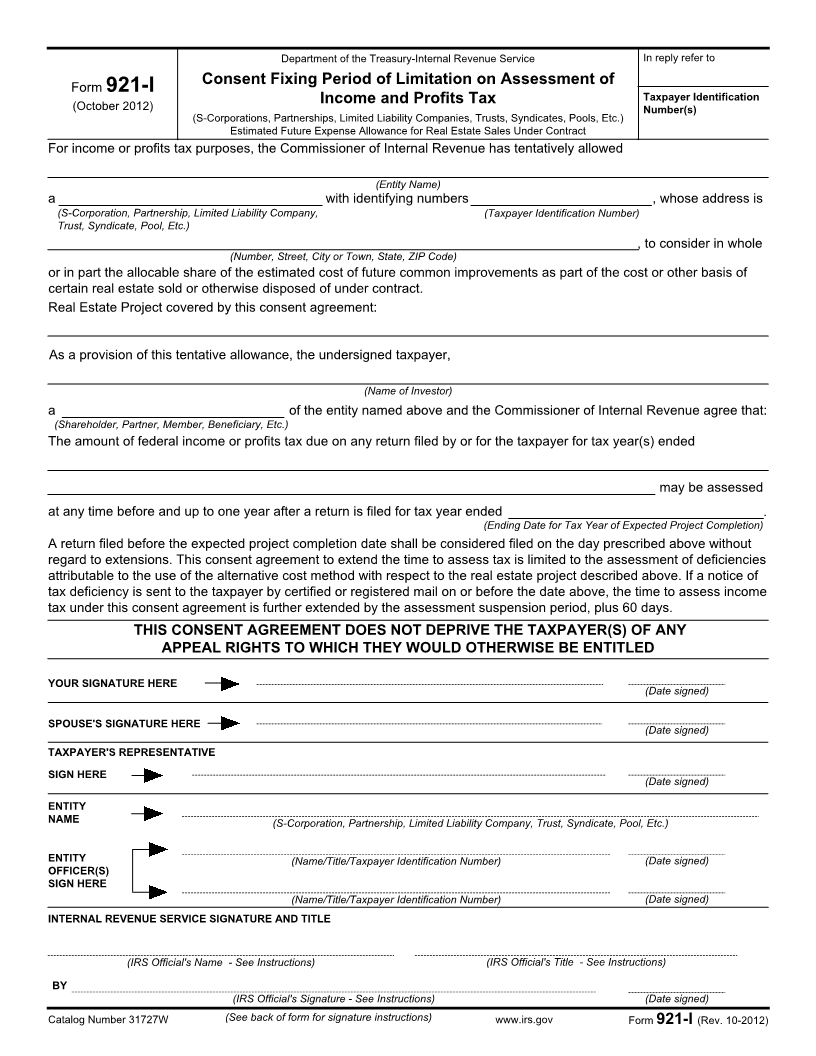

Department of the Treasury-Internal Revenue Service In reply refer to

Form 921-I Consent Fixing Period of Limitation on Assessment of

(October 2012) Income and Profits Tax Taxpayer Identification

Number(s)

(S-Corporations, Partnerships, Limited Liability Companies, Trusts, Syndicates, Pools, Etc.)

Estimated Future Expense Allowance for Real Estate Sales Under Contract

For income or profits tax purposes, the Commissioner of Internal Revenue has tentatively allowed

(Entity Name)

a with identifying numbers , whose address is

(S-Corporation, Partnership, Limited Liability Company, (Taxpayer Identification Number)

Trust, Syndicate, Pool, Etc.)

, to consider in whole

(Number, Street, City or Town, State, ZIP Code)

or in part the allocable share of the estimated cost of future common improvements as part of the cost or other basis of

certain real estate sold or otherwise disposed of under contract.

Real Estate Project covered by this consent agreement:

As a provision of this tentative allowance, the undersigned taxpayer,

(Name of Investor)

a of the entity named above and the Commissioner of Internal Revenue agree that:

(Shareholder, Partner, Member, Beneficiary, Etc.)

The amount of federal income or profits tax due on any return filed by or for the taxpayer for tax year(s) ended

may be assessed

at any time before and up to one year after a return is filed for tax year ended .

(Ending Date for Tax Year of Expected Project Completion)

A return filed before the expected project completion date shall be considered filed on the day prescribed above without

regard to extensions. This consent agreement to extend the time to assess tax is limited to the assessment of deficiencies

attributable to the use of the alternative cost method with respect to the real estate project described above. If a notice of

tax deficiency is sent to the taxpayer by certified or registered mail on or before the date above, the time to assess income

tax under this consent agreement is further extended by the assessment suspension period, plus 60 days.

THIS CONSENT AGREEMENT DOES NOT DEPRIVE THE TAXPAYER(S) OF ANY

APPEAL RIGHTS TO WHICH THEY WOULD OTHERWISE BE ENTITLED

YOUR SIGNATURE HERE

(Date signed)

SPOUSE'S SIGNATURE HERE (Date signed)

TAXPAYER'S REPRESENTATIVE

SIGN HERE (Date signed)

ENTITY

NAME (S-Corporation, Partnership, Limited Liability Company, Trust, Syndicate, Pool, Etc.)

ENTITY (Name/Title/Taxpayer Identification Number) (Date signed)

OFFICER(S)

SIGN HERE

(Name/Title/Taxpayer Identification Number) (Date signed)

INTERNAL REVENUE SERVICE SIGNATURE AND TITLE

(IRS Official's Name - See Instructions) (IRS Official's Title - See Instructions)

BY

(IRS Official's Signature - See Instructions) (Date signed)

Catalog Number 31727W (See back of form for signature instructions) www.irs.gov Form 921-I (Rev. 10-2012)