Enlarge image

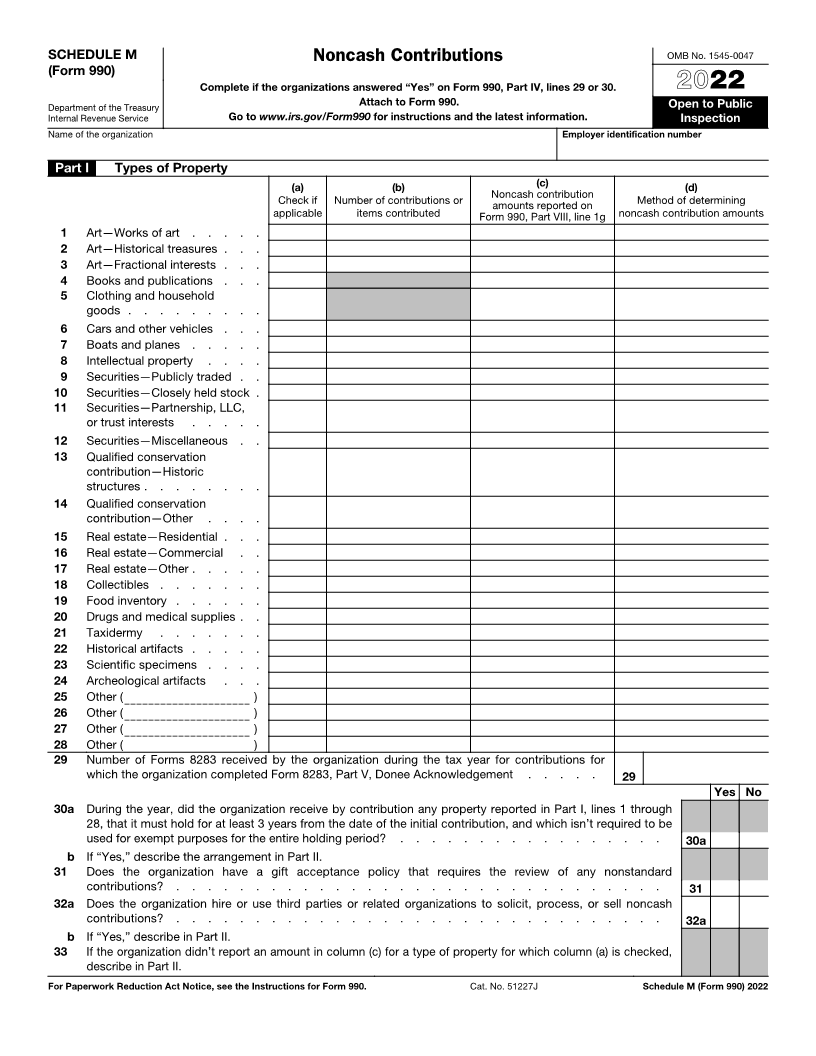

SCHEDULE M Noncash Contributions OMB No. 1545-0047

(Form 990)

Complete if the organizations answered “Yes” on Form 990, Part IV, lines 29 or 30. 2022

Department of the Treasury Attach to Form 990. Open to Public

Internal Revenue Service Go to www.irs.gov/Form990 for instructions and the latest information. Inspection

Name of the organization Employer identification number

Part I Types of Property

(a) (b) (c) (d)

Check if Number of contributions or Noncash contribution Method of determining

amounts reported on

applicable items contributed Form 990, Part VIII, line 1g noncash contribution amounts

1 Art—Works of art . . . . .

2 Art—Historical treasures . . .

3 Art—Fractional interests . . .

4 Books and publications . . .

5 Clothing and household

goods . . . . . . . . .

6 Cars and other vehicles . . .

7 Boats and planes . . . . .

8 Intellectual property . . . .

9 Securities—Publicly traded . .

10 Securities—Closely held stock .

11 Securities—Partnership, LLC,

or trust interests . . . . .

12 Securities—Miscellaneous . .

13 Qualified conservation

contribution—Historic

structures . . . . . . . .

14 Qualified conservation

contribution—Other . . . .

15 Real estate—Residential . . .

16 Real estate—Commercial . .

17 Real estate—Other . . . . .

18 Collectibles . . . . . . .

19 Food inventory . . . . . .

20 Drugs and medical supplies . .

21 Taxidermy . . . . . . .

22 Historical artifacts . . . . .

23 Scientific specimens . . . .

24 Archeological artifacts . . .

25 Other ( )

26 Other ( )

27 Other ( )

28 Other ( )

29 Number of Forms 8283 received by the organization during the tax year for contributions for

which the organization completed Form 8283, Part V, Donee Acknowledgement . . . . . 29

Yes No

30 a During the year, did the organization receive by contribution any property reported in Part I, lines 1 through

28, that it must hold for at least 3 years from the date of the initial contribution, and which isn’t required to be

used for exempt purposes for the entire holding period? . . . . . . . . . . . . . . . . . 30a

b If “Yes,” describe the arrangement in Part II.

31 Does the organization have a gift acceptance policy that requires the review of any nonstandard

contributions? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

32 a Does the organization hire or use third parties or related organizations to solicit, process, or sell noncash

contributions? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32a

b If “Yes,” describe in Part II.

33 If the organization didn’t report an amount in column (c) for a type of property for which column (a) is checked,

describe in Part II.

For Paperwork Reduction Act Notice, see the Instructions for Form 990. Cat. No. 51227J Schedule M (Form 990) 2022