Enlarge image

Department of the Treasury-Internal Revenue Service In reply refer to:

Form 872

(Rev. January 2014) Consent to Extend the Time to Assess Tax TIN

(Name(s))

taxpayer(s) of

(Address)

and the Commissioner of Internal Revenue consent and agree to the following:

(1) The amount of any Federal income tax due on any return(s) made by or

(Kind of tax)

for the above taxpayer(s) for the period(s) ended

may be assessed at any time on or before December 31, 20__ . If a provision

(Expiration date)

of the Internal Revenue Code suspends the running of the period of limitations to assess such tax, then, when, under the Internal

Revenue Code, the running of the period resumes, the extended period to assess will include the number of days remaining in the

extended period immediately before the suspension began.

(2) The taxpayer(s) may file a claim for credit or refund and the Service may credit or refund the tax within 6 months after this

agreement ends, except with respect to the items in paragraph (4).

(3) Paragraph (4) applies only to any taxpayer who holds an interest, either directly or indirectly, in any partnership subject to

subchapter C of chapter 63 of the Internal Revenue Code.

(4) Without otherwise limiting the applicability of this agreement, this agreement also extends the period of limitations for assessing any

tax (including penalties, additions to tax and interest) attributable to any partnership items (see section 6231 (a)(3)), affected items (see

section 6231(a)(5)), computational adjustments (see section 6231(a)(6)), and partnership items converted to nonpartnership items (see

section 6231(b)). Additionally, this agreement extends the period of limitations for assessing any tax (including penalties, additions to

tax, and interest) relating to any amounts carried over from the taxable year specified in paragraph (1) to any other taxable year(s). This

agreement extends the period for filing a petition for adjustment under section 6228(b) but only if a timely request for administrative

adjustment is filed under section 6227. For partnership items which have converted to nonpartnership items, this agreement extends

the period for filing a suit for refund or credit under section 6532, but only if a timely claim for refund is filed for such items.

(5) This Form contains the entire terms of the Consent to Extend the Time to Assess Tax. There are no representations, promises, or

agreements between the parties except those found or referenced on this Form.

With respect to the returns for the period(s) listed in paragraph (1) above, if the three-year period for assessing tax, under

Internal Revenue Code section 6501(a), ended prior to the date of this consent, then this consent serves to extend the

time to assess tax under any other provision of section 6501 for which the period of time to assess tax has not ended as

of the date of this consent.

This consent does not serve to shorten the statutory period of time to assess tax for any return.

Your Rights as a Taxpayer

You have the right to refuse to extend the period of limitations or limit this extension to a mutually agreed-upon issue(s) or mutually

agreed-upon period of time. Publication 1035, Extending the Tax Assessment Period, provides a more detailed explanation of your

rights and the consequences of the choices you may make. If you have not already received a Publication 1035, the publication can be

obtained, free of charge, from the IRS official who requested that you sign this consent or from the IRS' web site at www.irs.gov or by

calling toll free at 1-800-TAX-FORM (1-800-829-3676). Signing this consent will not deprive you of any appeal rights to which you would

otherwise be entitled.

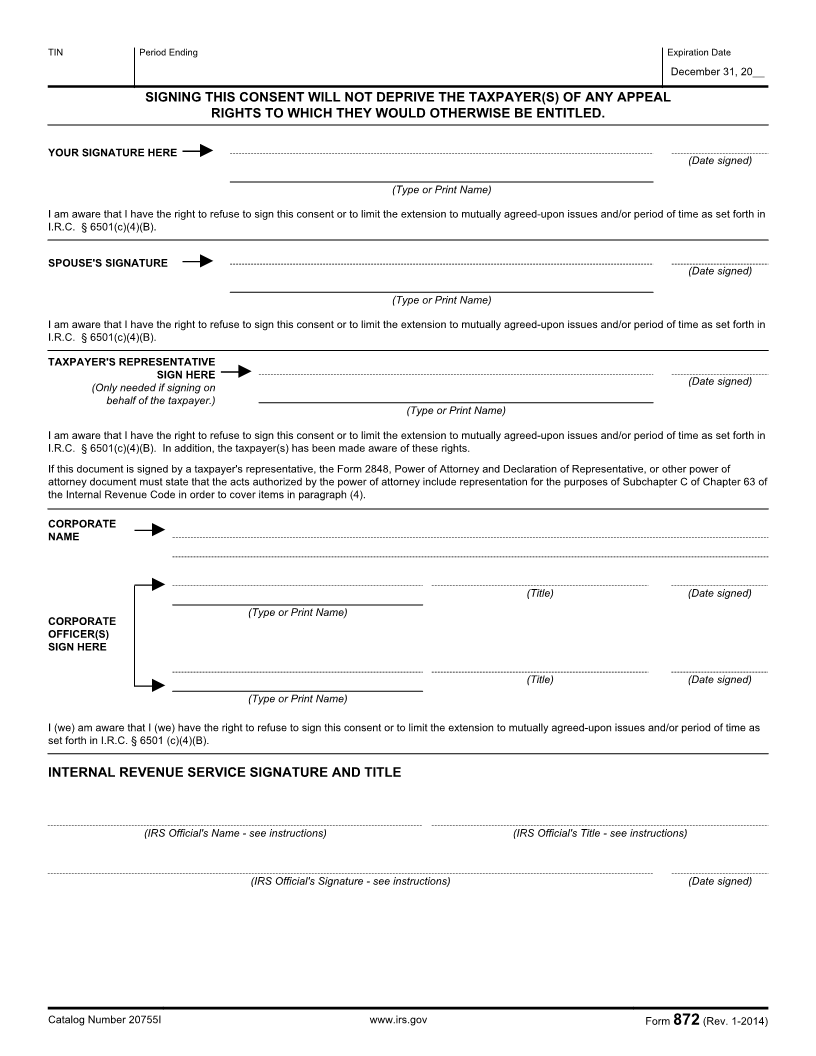

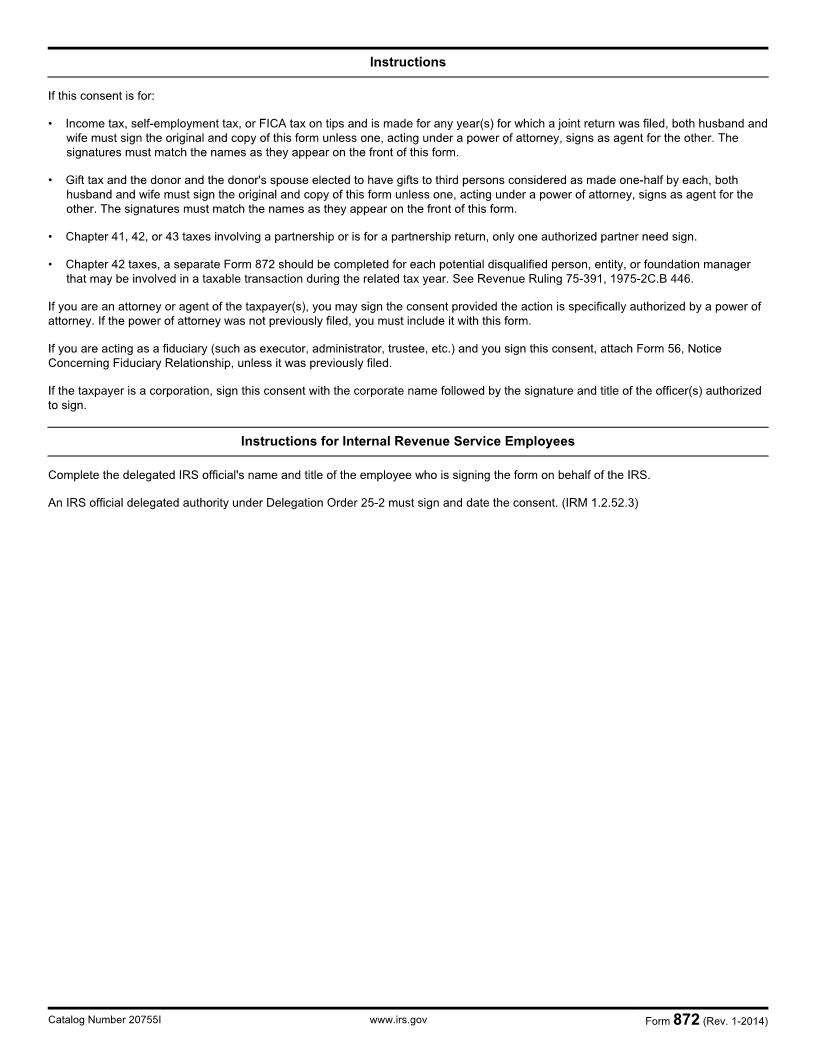

(Space for signature is on the back of this form and signature instructions are attached)

Catalog Number 20755I www.irs.gov Form 872 (Rev. 1-2014)