Enlarge image

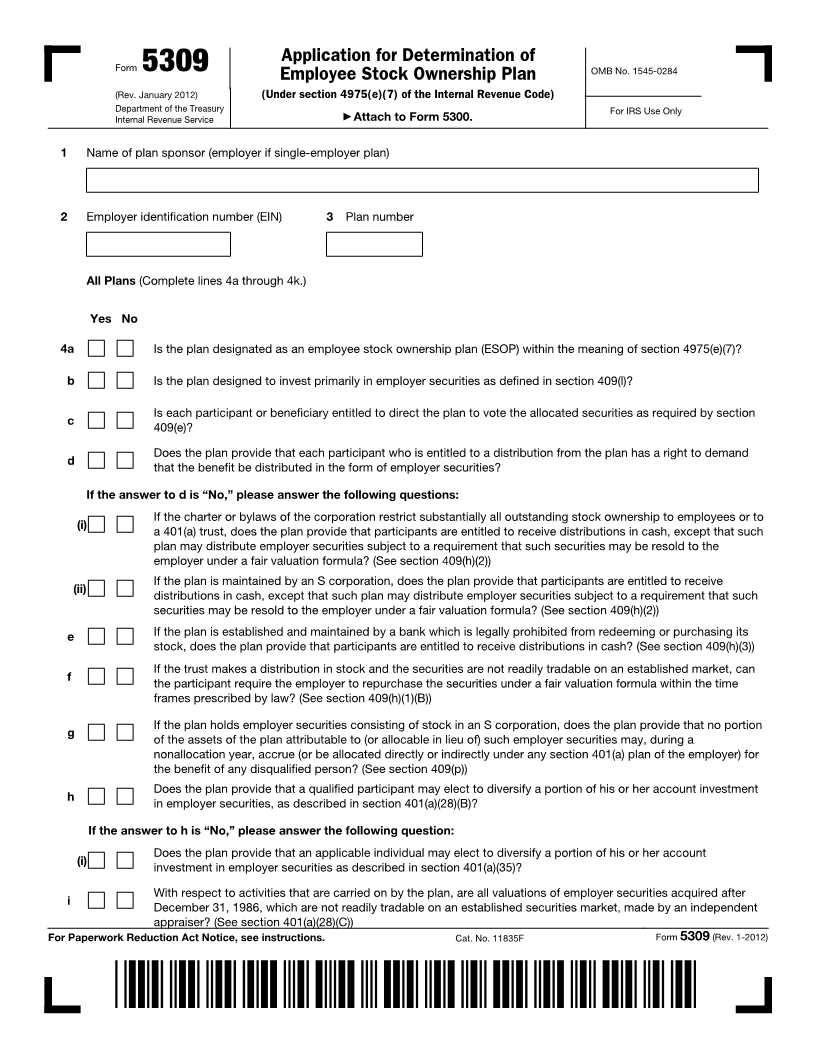

Application for Determination of

OMB No. 1545-0284

Form 5309 Employee Stock Ownership Plan

(Rev. January 2012) (Under section 4975(e)(7) of the Internal Revenue Code)

Department of the Treasury For IRS Use Only

Internal Revenue Service ▶ Attach to Form 5300.

1 Name of plan sponsor (employer if single-employer plan)

2 Employer identification number (EIN) 3 Plan number

All Plans (Complete lines 4a through 4k.)

Yes No

4a Is the plan designated as an employee stock ownership plan (ESOP) within the meaning of section 4975(e)(7)?

b Is the plan designed to invest primarily in employer securities as defined in section 409(l)?

Is each participant or beneficiary entitled to direct the plan to vote the allocated securities as required by section

c

409(e)?

Does the plan provide that each participant who is entitled to a distribution from the plan has a right to demand

d

that the benefit be distributed in the form of employer securities?

If the answer to d is “No,” please answer the following questions:

If the charter or bylaws of the corporation restrict substantially all outstanding stock ownership to employees or to

(i) a 401(a) trust, does the plan provide that participants are entitled to receive distributions in cash, except that such

plan may distribute employer securities subject to a requirement that such securities may be resold to the

employer under a fair valuation formula? (See section 409(h)(2))

If the plan is maintained by an S corporation, does the plan provide that participants are entitled to receive

(ii) distributions in cash, except that such plan may distribute employer securities subject to a requirement that such

securities may be resold to the employer under a fair valuation formula? (See section 409(h)(2))

e If the plan is established and maintained by a bank which is legally prohibited from redeeming or purchasing its

stock, does the plan provide that participants are entitled to receive distributions in cash? (See section 409(h)(3))

If the trust makes a distribution in stock and the securities are not readily tradable on an established market, can

f

the participant require the employer to repurchase the securities under a fair valuation formula within the time

frames prescribed by law? (See section 409(h)(1)(B))

If the plan holds employer securities consisting of stock in an S corporation, does the plan provide that no portion

g

of the assets of the plan attributable to (or allocable in lieu of) such employer securities may, during a

nonallocation year, accrue (or be allocated directly or indirectly under any section 401(a) plan of the employer) for

the benefit of any disqualified person? (See section 409(p))

Does the plan provide that a qualified participant may elect to diversify a portion of his or her account investment

h

in employer securities, as described in section 401(a)(28)(B)?

If the answer to h is “No,” please answer the following question:

Does the plan provide that an applicable individual may elect to diversify a portion of his or her account

(i) investment in employer securities as described in section 401(a)(35)?

With respect to activities that are carried on by the plan, are all valuations of employer securities acquired after

i

December 31, 1986, which are not readily tradable on an established securities market, made by an independent

appraiser? (See section 401(a)(28)(C))

For Paperwork Reduction Act Notice, see instructions. Cat. No. 11835F Form 5309 (Rev. 1-2012)