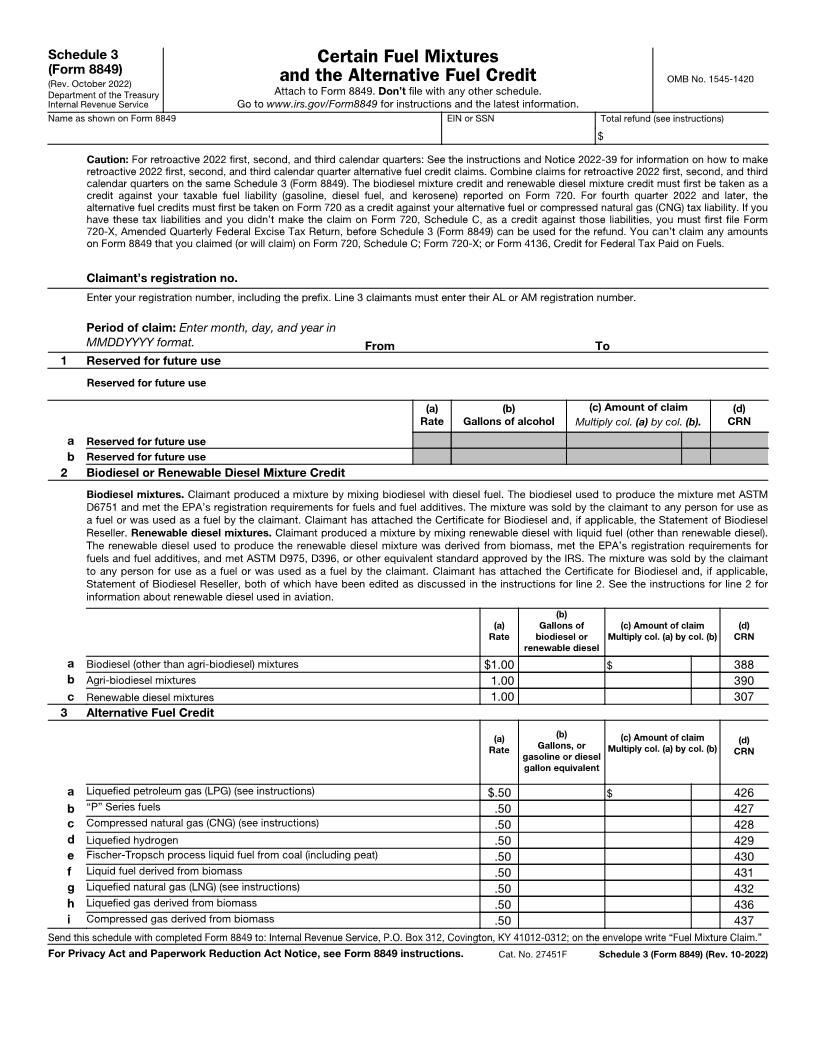

Enlarge image

Schedule 3 Certain Fuel Mixtures

(Form 8849)

(Rev. October 2022) and the Alternative Fuel Credit OMB No. 1545-1420

Department of the Treasury Attach to Form 8849. Don’t file with any other schedule.

Internal Revenue Service Go to www.irs.gov/Form8849 for instructions and the latest information.

Name as shown on Form 8849 EIN or SSN Total refund (see instructions)

$

Caution: For retroactive 2022 first, second, and third calendar quarters: See the instructions and Notice 2022-39 for information on how to make

retroactive 2022 first, second, and third calendar quarter alternative fuel credit claims. Combine claims for retroactive 2022 first, second, and third

calendar quarters on the same Schedule 3 (Form 8849). The biodiesel mixture credit and renewable diesel mixture credit must first be taken as a

credit against your taxable fuel liability (gasoline, diesel fuel, and kerosene) reported on Form 720. For fourth quarter 2022 and later, the

alternative fuel credits must first be taken on Form 720 as a credit against your alternative fuel or compressed natural gas (CNG) tax liability. If you

have these tax liabilities and you didn’t make the claim on Form 720, Schedule C, as a credit against those liabilities, you must first file Form

720-X, Amended Quarterly Federal Excise Tax Return, before Schedule 3 (Form 8849) can be used for the refund. You can’t claim any amounts

on Form 8849 that you claimed (or will claim) on Form 720, Schedule C; Form 720-X; or Form 4136, Credit for Federal Tax Paid on Fuels.

Claimant’s registration no.

Enter your registration number, including the prefix. Line 3 claimants must enter their AL or AM registration number.

Period of claim: Enter month, day, and year in

MMDDYYYY format. From To

1 Reserved for future use

Reserved for future use

(a) (b) (c) Amount of claim (d)

Rate Gallons of alcohol Multiply col. (a) by col. (b). CRN

a Reserved for future use

b Reserved for future use

2 Biodiesel or Renewable Diesel Mixture Credit

Biodiesel mixtures. Claimant produced a mixture by mixing biodiesel with diesel fuel. The biodiesel used to produce the mixture met ASTM

D6751 and met the EPA’s registration requirements for fuels and fuel additives. The mixture was sold by the claimant to any person for use as

a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable, the Statement of Biodiesel

Reseller. Renewable diesel mixtures. Claimant produced a mixture by mixing renewable diesel with liquid fuel (other than renewable diesel).

The renewable diesel used to produce the renewable diesel mixture was derived from biomass, met the EPA’s registration requirements for

fuels and fuel additives, and met ASTM D975, D396, or other equivalent standard approved by the IRS. The mixture was sold by the claimant

to any person for use as a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable,

Statement of Biodiesel Reseller, both of which have been edited as discussed in the instructions for line 2. See the instructions for line 2 for

information about renewable diesel used in aviation.

(b)

(a) Gallons of (c) Amount of claim (d)

Rate biodiesel or Multiply col. (a) by col. (b) CRN

renewable diesel

a Biodiesel (other than agri-biodiesel) mixtures $1.00 $ 388

b Agri-biodiesel mixtures 1.00 390

c Renewable diesel mixtures 1.00 307

3 Alternative Fuel Credit

(a) (b) (c) Amount of claim (d)

Rate Gallons, or Multiply col. (a) by col. (b) CRN

gasoline or diesel

gallon equivalent

a Liquefied petroleum gas (LPG) (see instructions) $.50 $ 426

b “P” Series fuels .50 427

c Compressed natural gas (CNG) (see instructions) .50 428

d Liquefied hydrogen .50 429

e Fischer-Tropsch process liquid fuel from coal (including peat) .50 430

f Liquid fuel derived from biomass .50 431

g Liquefied natural gas (LNG) (see instructions) .50 432

h Liquefied gas derived from biomass .50 436

i Compressed gas derived from biomass .50 437

Send this schedule with completed Form 8849 to: Internal Revenue Service, P.O. Box 312, Covington, KY 41012-0312; on the envelope write “Fuel Mixture Claim.”

For Privacy Act and Paperwork Reduction Act Notice, see Form 8849 instructions. Cat. No. 27451F Schedule 3 (Form 8849) (Rev. 10-2022)