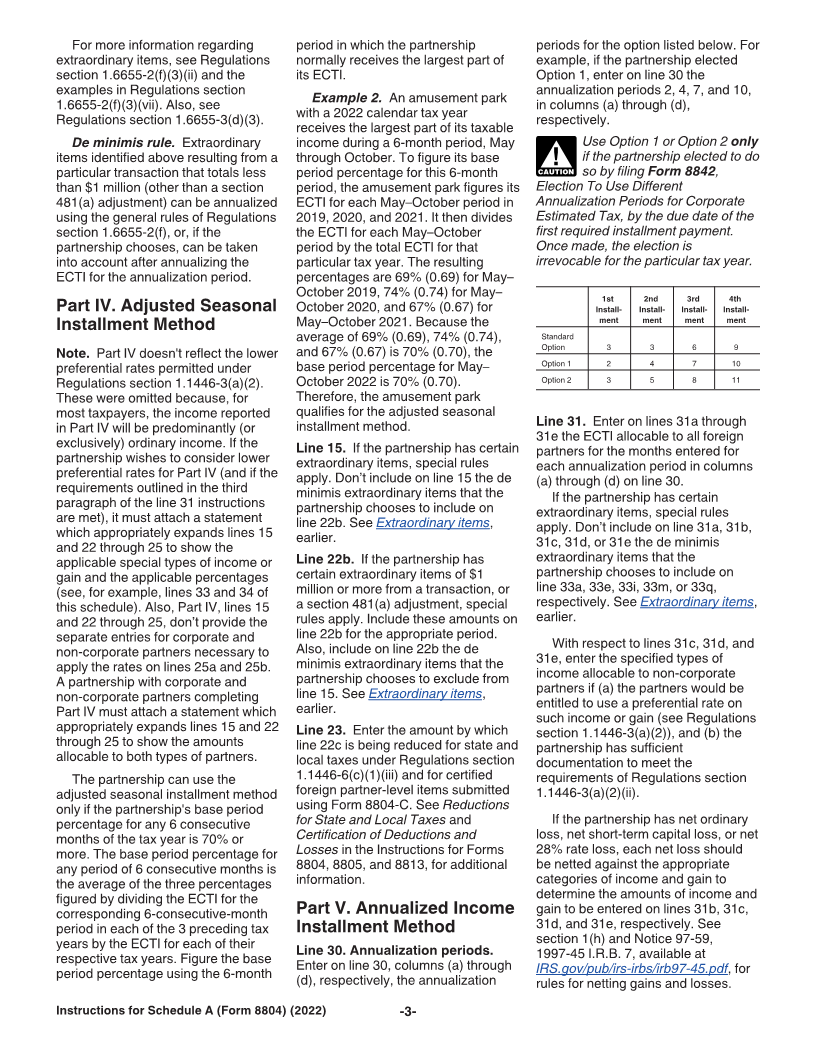

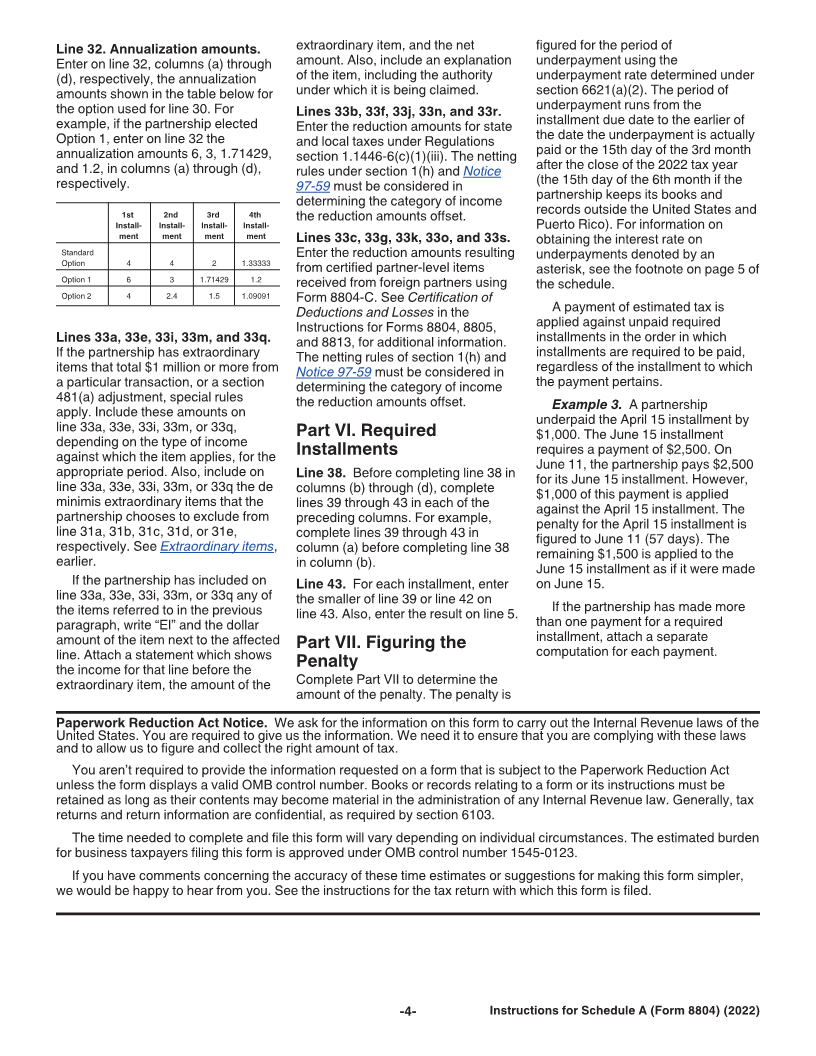

Enlarge image

Userid: CPM Schema: Leadpct: 100% Pt. size: 10 Draft Ok to Print

instrx

AH XSL/XML Fileid: … /i8804scha/2022/a/xml/cycle04/source (Init. & Date) _______

Page 1 of 4 13:54 - 13-Oct-2022

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

2022

Instructions for Schedule A

(Form 8804)

Penalty for Underpayment of Estimated Section 1446 Tax for Partnerships

Section references are to the Internal certified foreign partner-level items, 8804. Be sure to check the box on

Revenue Code unless otherwise noted. on the ECTI allocable to foreign Form 8804, line 8.

partners for 2021, provided that (1) • If the total section 1446 tax, shown

Future Developments this amount is at least 50% of the sum on Part II, line 1, is $500 or more,

For the latest information about of the amounts shown on lines 4d, 4h, complete the rest of page 1 to

developments related to Schedule A 4l, 4p, and 4t of its 2022 Form 8804; determine the underpayment for any

(Form 8804) and its instructions, such and (2) the tax year was for a full 12 of the installment due dates.

as legislation enacted after they were months. See the instructions for line 2, • If there is an underpayment on

published, go to IRS.gov/About- later, for more details. line 12 (column (a), (b), (c), or (d)), go

to Part VII to figure the penalty.

Schedule-A-Form-8804. In these instructions, “Form 8804”

• Complete Parts IV through VI as

generally refers to the partnership's

appropriate if the partnership uses the

General Instructions original Form 8804. However, an

adjusted seasonal installment method

amended Form 8804 is considered

and/or the annualized income

Purpose of Form the original Form 8804 if the amended

installment method.

Partnerships that have effectively Form 8804 is filed by the due date

connected taxable income (ECTI) (including extensions) of the original

allocable to foreign partners use Form 8804. Specific Instructions

Schedule A (Form 8804) to Also, for purposes of determining a

Part I. Reasons for Filing

determine: required installment, if an amended

• Whether they are subject to the Form 8804 is filed for the prior tax Adjusted seasonal installment

penalty for underpayment of year, then “prior tax year” includes the method and/or annualized income

estimated tax and, if so, amended Form 8804, but only if the installment method. If the

• The amount of the underpayment amended Form 8804 is filed before partnership's income varied during the

penalty. the applicable installment due date. year because, for example, it

operated its business on a seasonal

Who Must File The penalty is figured separately basis, it may be able to lower or

Generally, the partnership doesn’t for each installment due date. eliminate the amount of one or more

have to file this schedule because the Therefore, the partnership may owe a required installments by using the

IRS will figure the amount of the penalty for an earlier due date even if adjusted seasonal installment method

penalty and notify the partnership of it paid enough tax later to make up the and/or the annualized income

any amount due. However, even if the underpayment. This is true even if the installment method.

partnership doesn’t owe a penalty, partnership is due a refund when its

complete and attach this schedule to return is filed. However, the Example 1. A ski shop, which

the partnership's Form 8804 if the Part partnership may be able to reduce or receives most of its income during the

II, line 1, amount on page 1 is $500 or eliminate the penalty by using the winter months, may benefit from using

more and any of the following apply. annualized income installment one or both of these methods to figure

method or the adjusted seasonal its required installments. The

1. The adjusted seasonal installment method. See the annualized income installment or

installment method is used. instructions for Parts IV and V for adjusted seasonal installment may be

2. The annualized income details. less than the required installment

installment method is used. under the current year safe harbor

Exception to the Penalty (increased by any reduction

Who Must Pay the A partnership won’t have to pay a recaptured under section 6655(e)(1)

Underpayment Penalty penalty if the tax shown on line 5f of (B)) for one or more due dates. Using

Generally, a partnership is subject to its 2022 Form 8804 is less than $500. one or both of these methods may

the penalty if it didn’t timely pay in reduce or eliminate the penalty for

installments at least the smaller of: How To Use Schedule A those due dates.

1. The tax shown on line 5f of its Complete this schedule as follows. Use Parts IV through VI of

Schedule A (Form 8804) to figure one

2022 Form 8804; or • Check one or both of the boxes in or more required installments. If Parts

2. The total section 1446 tax that Part I that apply. If the partnership IV through VI are used for any

would have been due for 2021, checks a box in Part I, attach payment due date, Parts IV through VI

without regard to reductions for Schedule A (Form 8804) to Form

Aug 31, 2022 Cat. No. 36325U