Enlarge image

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9 Draft Ok to Print

AH XSL/XML Fileid: … ns/I1023/202001/A/XML/Cycle06/source (Init. & Date) _______

Page 1 of 40 12:09 - 30-Jan-2020

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Instructions for Form 1023

(Rev. January 2020)

Application for Recognition of Exemption Under Section 501(c)(3) of the Internal

Revenue Code

Section references are to the Internal Revenue Contents Page How To Get Forms and

Code unless otherwise noted.

Revenue Code Section Publications

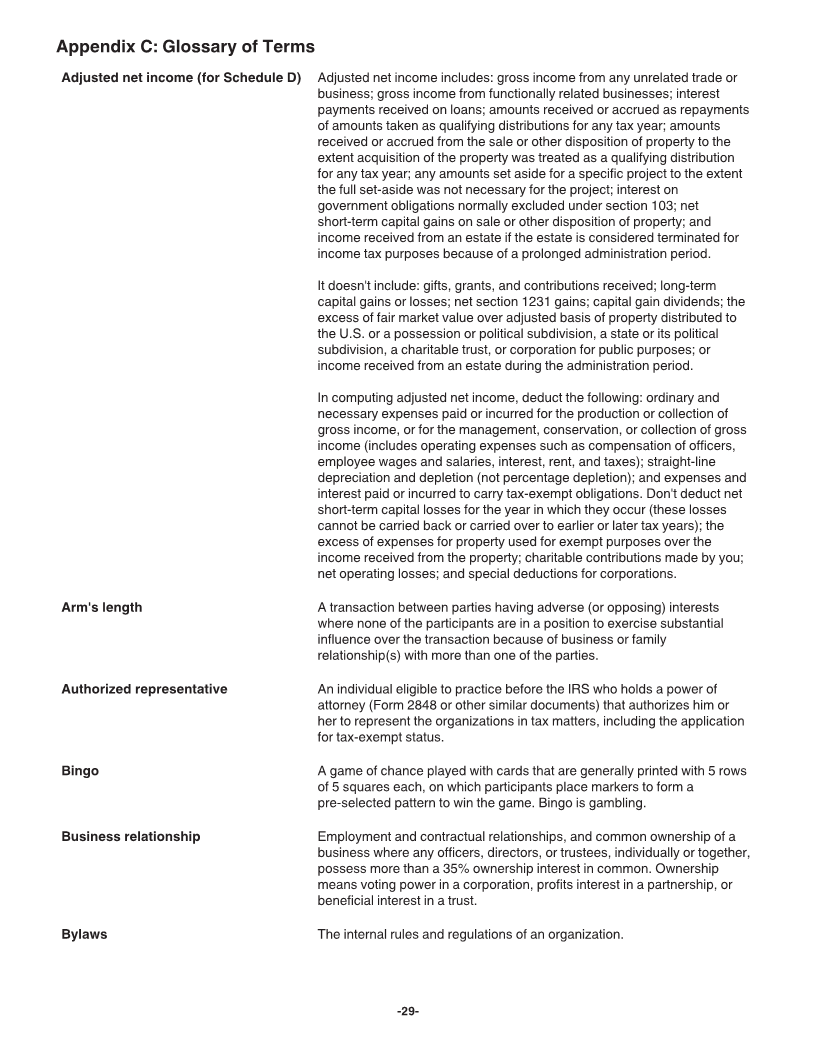

Contents Page 508(e) 27

Future Developments Appendix C: Glossary of Terms 29 Internet. You can access the IRS website

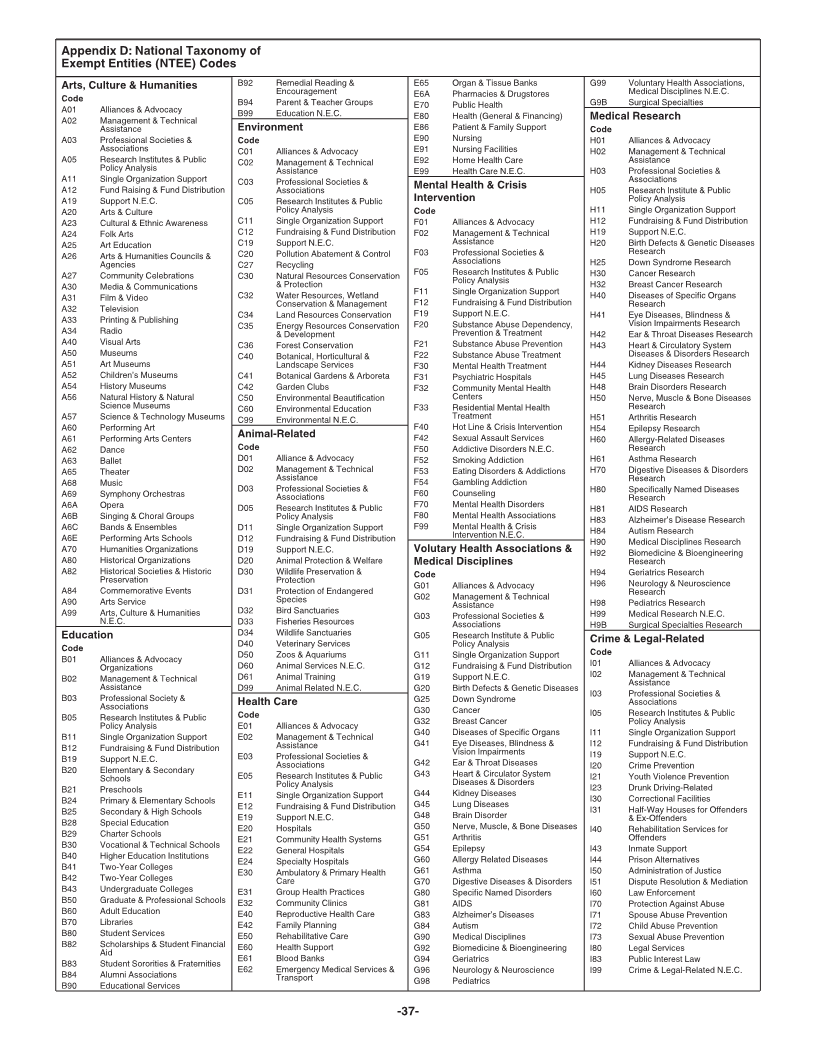

What's New Appendix D: National Taxonomy of 24 hours a day, 7 days a week, at IRS.gov

Overview of Organizations Exempt Entities (NTEE) to do the following.

Described in Section 501(c) Codes 37 • Download forms, instructions, and

(3) Index 40 publications.

General Instructions • Order IRS products online.

Note. Keep a copy of the completed • Research your tax questions online.

Answers Form 1023 for your permanent records. • Search publications by topic or

Purpose of Form

keyword.

What To File Use the online Internal Revenue Code,

•

When To File Future Developments regulations, or other official guidance.

Filing Assistance For the latest information about • View Internal Revenue Bulletins (IRBs)

Signature Requirements developments related to Form 1023 and published since 1995.

Authorized Representative its instructions, such as legislation • Sign up at IRS.gov/Charities-Non-

Public Inspection enacted after they were published, go to Profits to receive local and national tax

Foreign Organizations IRS.gov/Form1023. news by email.

Specific Instructions Reminder Tax forms and publications. You can

Part I. Identification of Applicant download or print all of the forms and

Part II. Organizational Structure Don't include social security numbers

on publicly disclosed forms. Because publications you may need at IRS.gov/

Part III. Required Provisions in the IRS is required to disclose approved FormsPubs. Otherwise, you can go to

Your Organizing Document IRS.gov/OrderForms to place an order

exemption applications and information

Part IV. Your Activities returns, don't include social security and have forms mailed to you. You should

Part V. Compensation and Other numbers on this form. Documents subject receive your order within 10 business

Financial Arrangements 10 days.

to disclosure include supporting

Part VI. Financial Data 11 information filed with the form and

Part VII. Foundation correspondence with the IRS about the

Classification 13 filing. Overview of Organizations

Part VIII. Effective Date 15 Described in Section

Part IX. Annual Filing Phone Help

501(c)(3)

Requirement 15 If you have questions and/or need help

Part X. Signature 16 completing Form 1023, please call How To Request Recognition of

Schedule A. Churches 16 877-829-5500. This toll-free telephone Tax-Exempt Status Under

Schedule B. Schools, Colleges, service is available Monday through

and Universities 17 Friday. Section 501(c)(3)

Schedule C. Hospitals and Section 501(c)(3) describes organizations

Medical Research Email Subscription organized and operated exclusively for

Organizations 18 The IRS provides a subscription-based religious, charitable, scientific, testing for

Schedule D. Section 509(a)(3) email service for tax professionals and public safety, literary, or educational

Supporting Organizations 20 representatives of tax-exempt purposes, or to foster national or

Schedule E. Effective Date 21 organizations. We send subscribers international amateur sports competition,

Schedule F. Low-Income periodic updates regarding exempt or for the prevention of cruelty to children

Housing 22 organization tax law and regulations, or animals. Unless an exception applies,

Schedule G. Successors to Other available services, and other information. an organization must file Form 1023 or

Organizations 22 To subscribe, visit IRS.gov/Charities. Form 1023-EZ (if eligible) to obtain

Schedule H. Organizations recognition of exemption from federal

Providing Scholarships, income tax under section 501(c)(3). You

Fellowships, Educational What's New can find information about eligibility to file

Loans, or Other Educational

Grants to Individuals and Organizations requesting recognition of Form 1023-EZ at IRS.gov/Charities.

Private Foundations tax-exempt status under section 501(c)(3)

Requesting Advance must complete and submit their Form Organizations not required to

Approval of Individual Grant 1023 (or Form 1023-EZ, if eligible) obtain recognition of exemption. The

Procedures 22 applications electronically (including following types of organizations may be

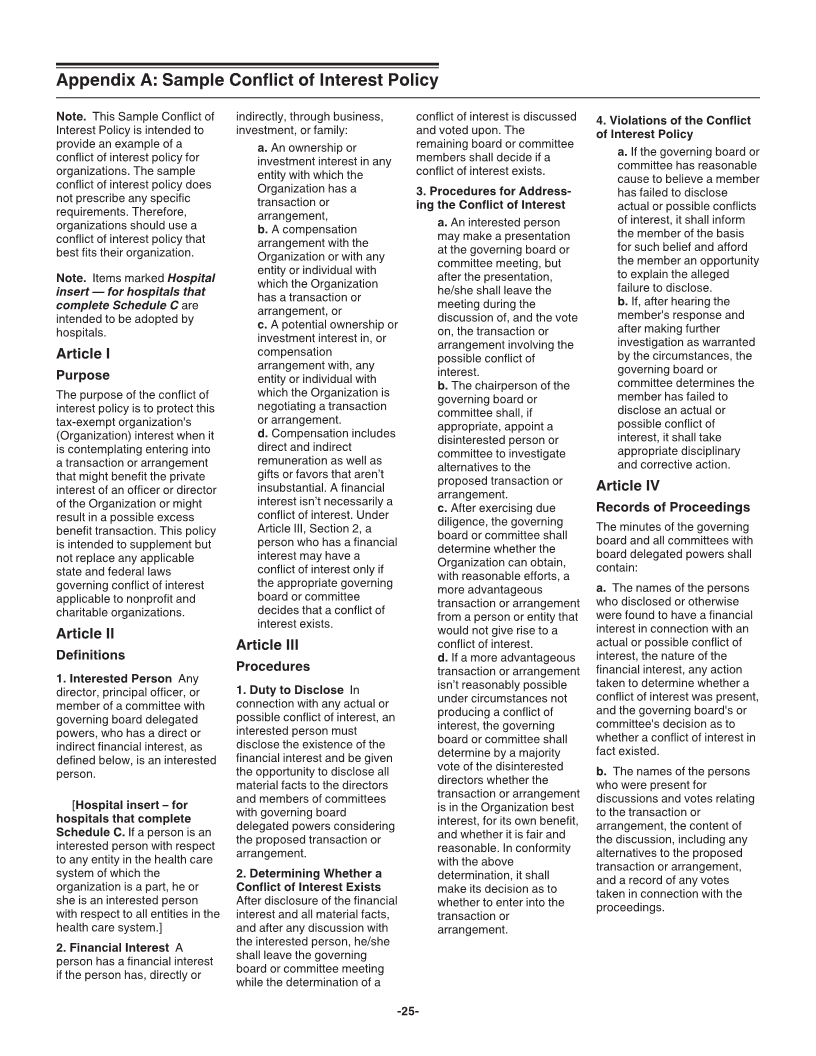

Appendix A: Sample Conflict of paying the correct user fee) using considered tax exempt under section

Interest Policy 25 Pay.gov. 501(c)(3) without filing Form 1023 (or

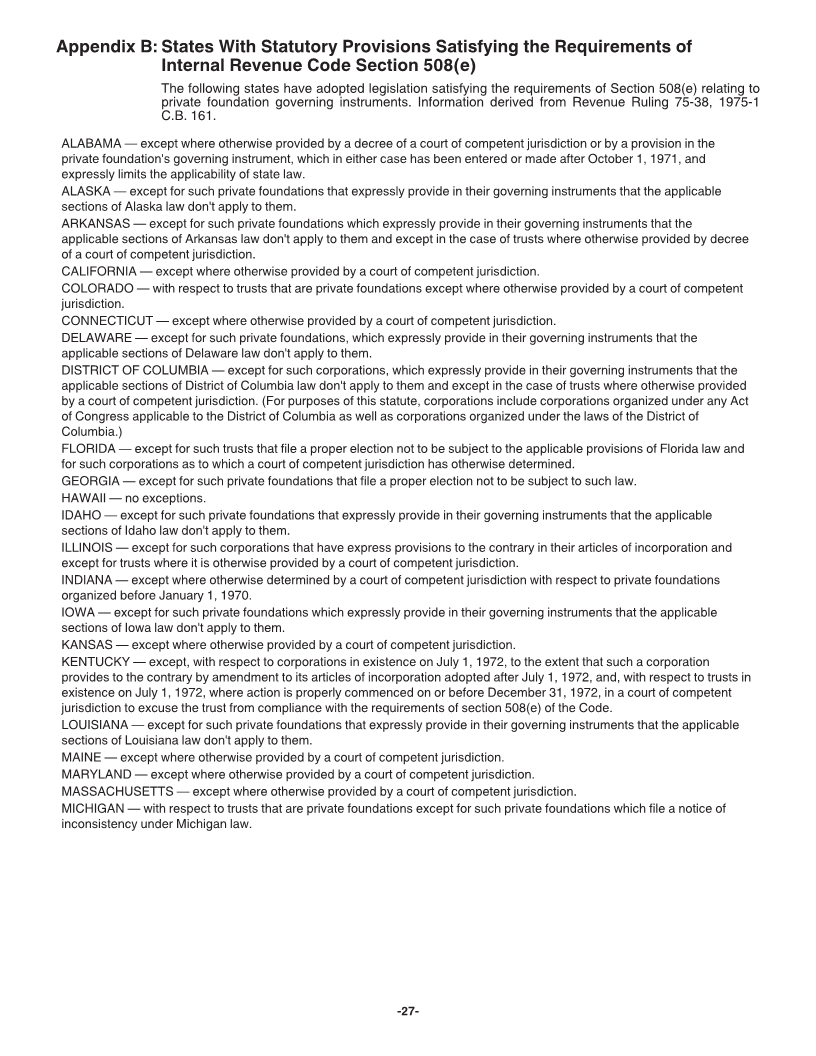

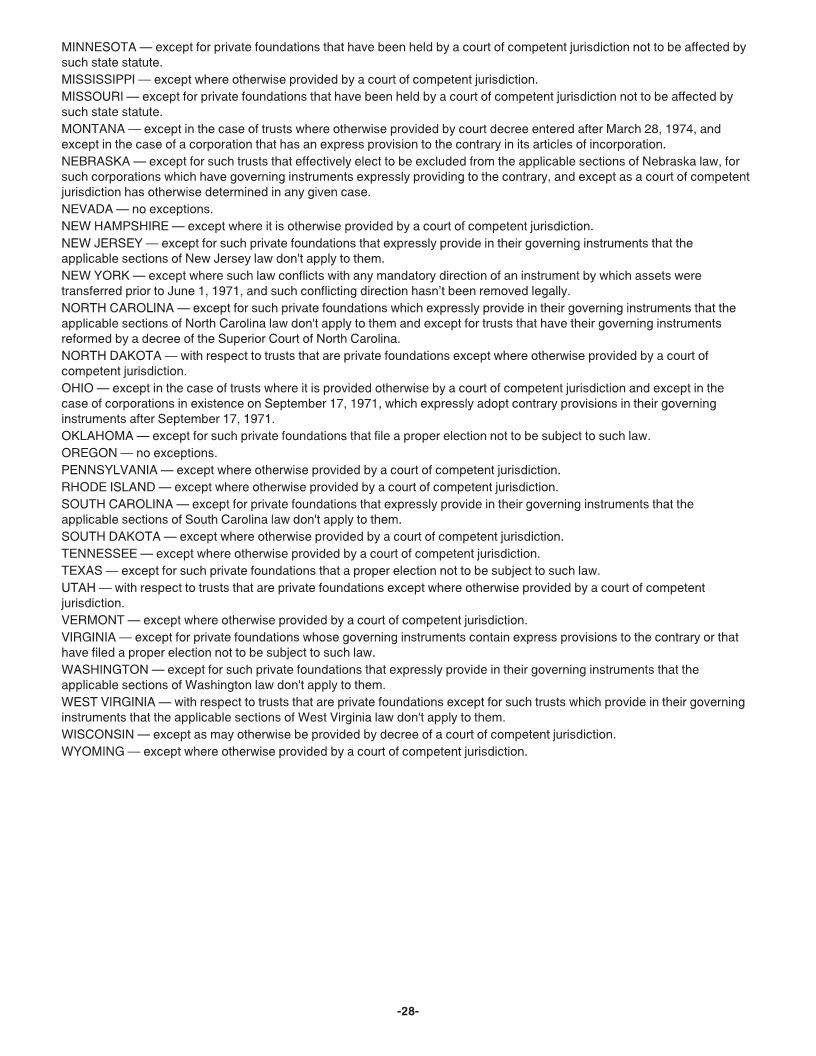

Appendix B: States With Statutory Form 1023-EZ).

Provisions Satisfying the • Churches, including synagogues,

Requirements of Internal temples, and mosques.

Jan 30, 2020 Cat. No. 17132z