Enlarge image

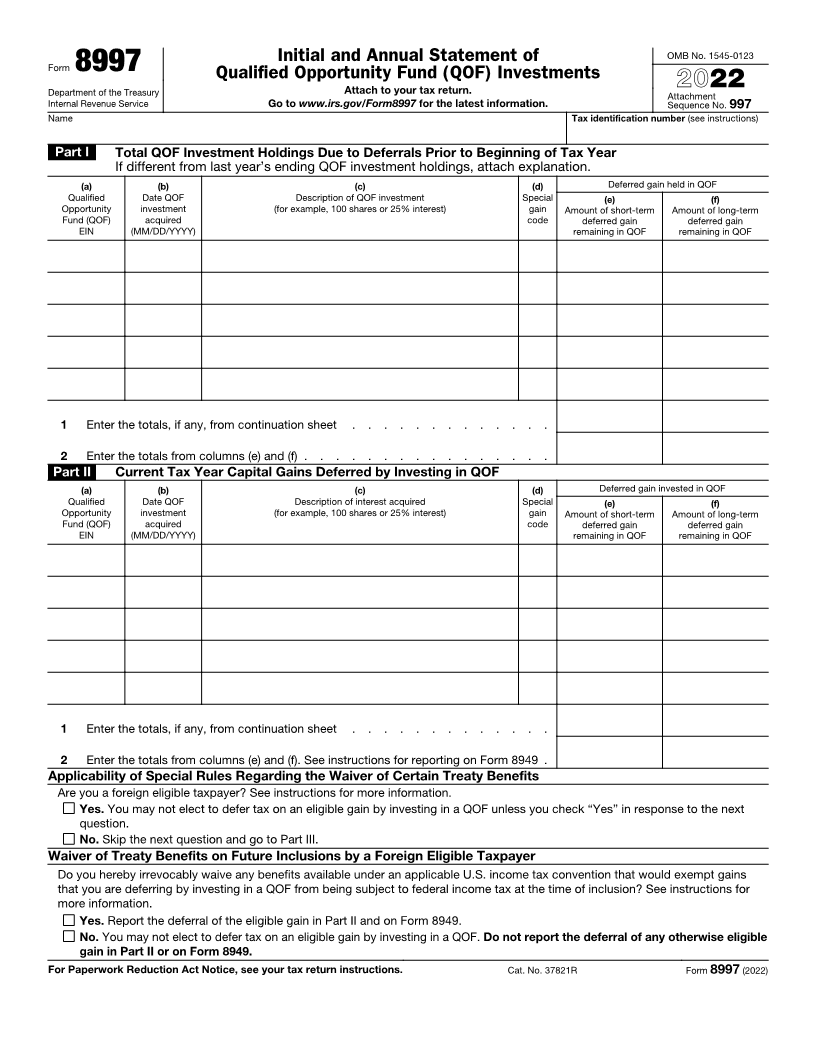

Initial and Annual Statement of OMB No. 1545-0123

Form 8997 Qualified Opportunity Fund (QOF) Investments

Department of the Treasury Attach to your tax return. Attachment 2022

Internal Revenue Service Go to www.irs.gov/Form8997 for the latest information. Sequence No. 997

Name Tax identification number (see instructions)

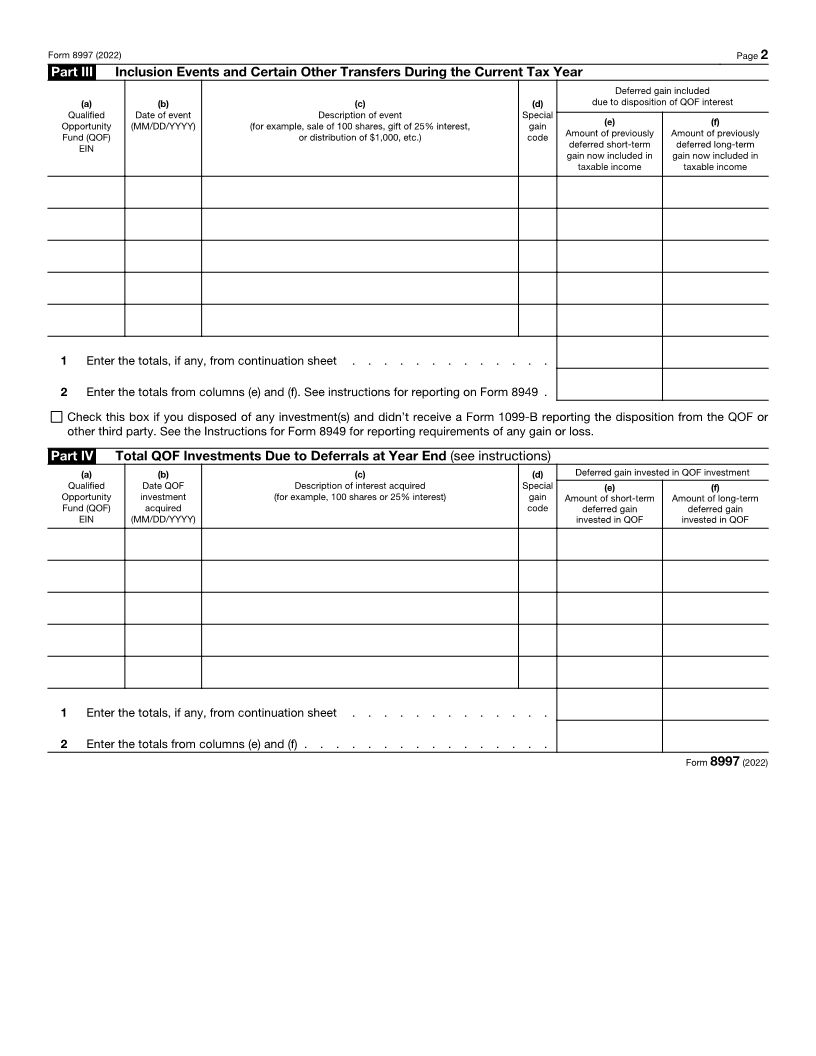

Part I Total QOF Investment Holdings Due to Deferrals Prior to Beginning of Tax Year

If different from last year’s ending QOF investment holdings, attach explanation.

(a) (b) (c) (d) Deferred gain held in QOF

Qualified Date QOF Description of QOF investment Special (e) (f)

Opportunity investment (for example, 100 shares or 25% interest) gain Amount of short-term Amount of long-term

Fund (QOF) acquired code deferred gain deferred gain

EIN (MM/DD/YYYY) remaining in QOF remaining in QOF

1 Enter the totals, if any, from continuation sheet . . . . . . . . . . . . .

2 Enter the totals from columns (e) and (f) . . . . . . . . . . . . . . . .

Part II Current Tax Year Capital Gains Deferred by Investing in QOF

(a) (b) (c) (d) Deferred gain invested in QOF

Qualified Date QOF Description of interest acquired Special (e) (f)

Opportunity investment (for example, 100 shares or 25% interest) gain Amount of short-term Amount of long-term

Fund (QOF) acquired code deferred gain deferred gain

EIN (MM/DD/YYYY) remaining in QOF remaining in QOF

1 Enter the totals, if any, from continuation sheet . . . . . . . . . . . . .

2 Enter the totals from columns (e) and (f). See instructions for reporting on Form 8949 .

Applicability of Special Rules Regarding the Waiver of Certain Treaty Benefits

Are you a foreign eligible taxpayer? See instructions for more information.

Yes. You may not elect to defer tax on an eligible gain by investing in a QOF unless you check “Yes” in response to the next

question.

No. Skip the next question and go to Part III.

Waiver of Treaty Benefits on Future Inclusions by a Foreign Eligible Taxpayer

Do you hereby irrevocably waive any benefits available under an applicable U.S. income tax convention that would exempt gains

that you are deferring by investing in a QOF from being subject to federal income tax at the time of inclusion? See instructions for

more information.

Yes. Report the deferral of the eligible gain in Part II and on Form 8949.

No. You may not elect to defer tax on an eligible gain by investing in a QOF. Do not report the deferral of any otherwise eligible

gain in Part II or on Form 8949.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37821R Form 8997 (2022)