Enlarge image

PHONE (406) 444-3834

Montana Relay (TDD): 711

uieservices@mt.gov

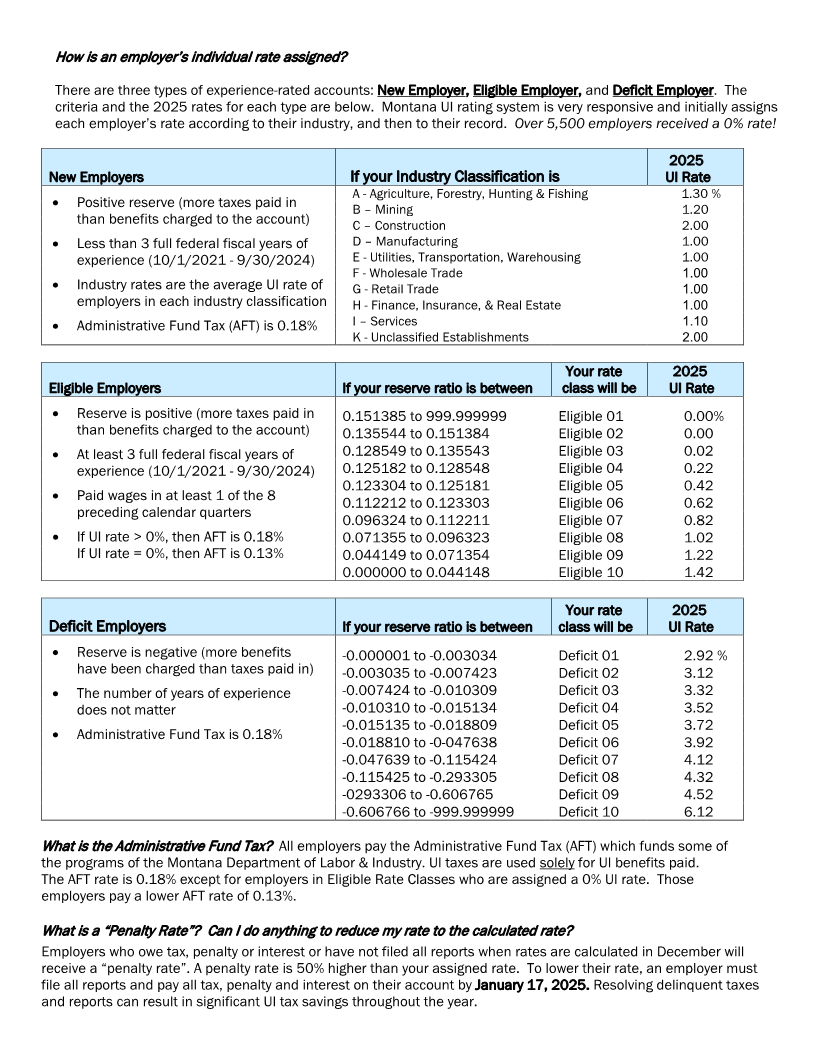

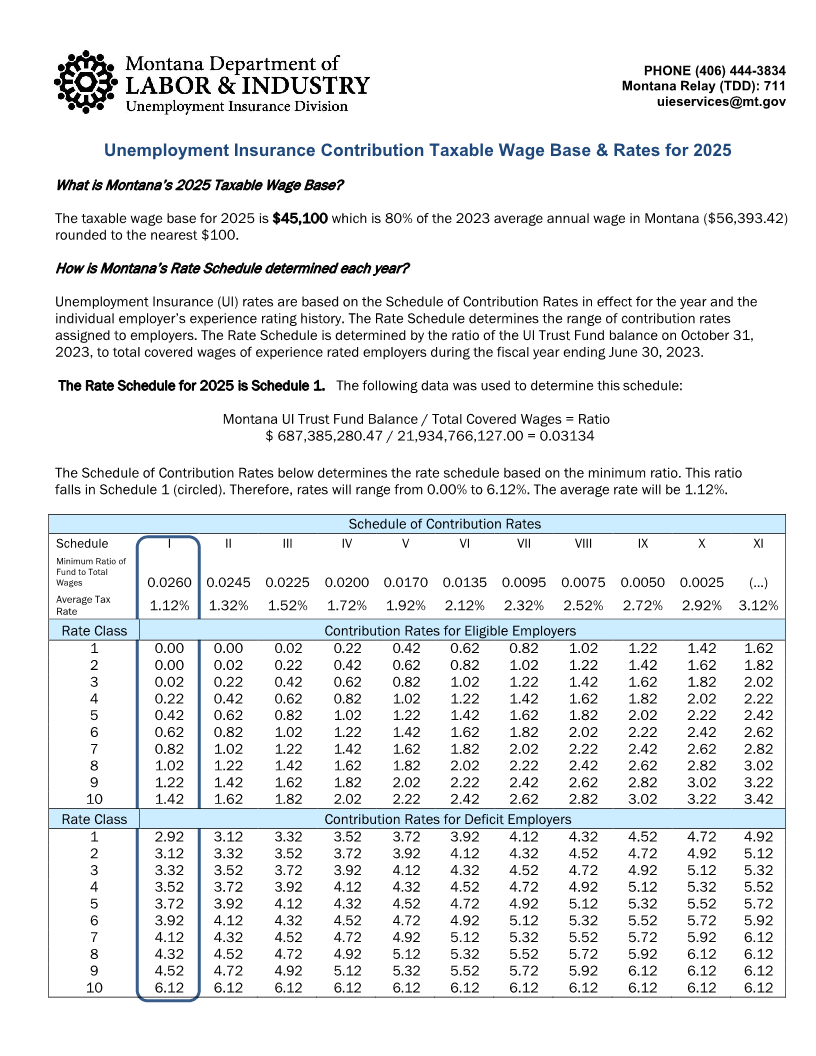

Unemployment Insurance Contribution Taxable Wage Base & Rates for 2025

What is Montana’s 2025 Taxable Wage Base?

The taxable wage base for 2025 is $45,100 which is 80% of the 2023 average annual wage in Montana ($56,393.42)

rounded to the nearest $100.

How is Montana’s Rate Schedule determined each year?

Unemployment Insurance (UI) rates are based on the Schedule of Contribution Rates in effect for the year and the

individual employer’s experience rating history. The Rate Schedule determines the range of contribution rates

assigned to employers. The Rate Schedule is determined by the ratio of the UI Trust Fund balance on October 31,

2023, to total covered wages of experience rated employers during the fiscal year ending June 30, 2023.

The Rate Schedule for 2025 is Schedule 1. The following data was used to determine this schedule:

Montana UI Trust Fund Balance / Total Covered Wages = Ratio

$ 687,385,280.47 / 21,934,766,127.00 = 0.03134

The Schedule of Contribution Rates below determines the rate schedule based on the minimum ratio. This ratio

falls in Schedule 1 (circled). Therefore, rates will range from 0.00% to 6.12%. The average rate will be 1.12%.

Schedule of Contribution Rates

Schedule I II III IV V VI VII VIII IX X XI

Minimum Ratio of

Fund to Total

Wages 0.0260 0.0245 0.0225 0.0200 0.0170 0.0135 0.0095 0.0075 0.0050 0.0025 (…)

Average Tax

Rate 1.12% 1.32% 1.52% 1.72% 1.92% 2.12% 2.32% 2.52% 2.72% 2.92% 3.12%

Rate Class Contribution Rates for Eligible Employers

1 0.00 0.00 0.02 0.22 0.42 0.62 0.82 1.02 1.22 1.42 1.62

2 0.00 0.02 0.22 0.42 0.62 0.82 1.02 1.22 1.42 1.62 1.82

3 0.02 0.22 0.42 0.62 0.82 1.02 1.22 1.42 1.62 1.82 2.02

4 0.22 0.42 0.62 0.82 1.02 1.22 1.42 1.62 1.82 2.02 2.22

5 0.42 0.62 0.82 1.02 1.22 1.42 1.62 1.82 2.02 2.22 2.42

6 0.62 0.82 1.02 1.22 1.42 1.62 1.82 2.02 2.22 2.42 2.62

7 0.82 1.02 1.22 1.42 1.62 1.82 2.02 2.22 2.42 2.62 2.82

8 1.02 1.22 1.42 1.62 1.82 2.02 2.22 2.42 2.62 2.82 3.02

9 1.22 1.42 1.62 1.82 2.02 2.22 2.42 2.62 2.82 3.02 3.22

10 1.42 1.62 1.82 2.02 2.22 2.42 2.62 2.82 3.02 3.22 3.42

Rate Class Contribution Rates for Deficit Employers

1 2.92 3.12 3.32 3.52 3.72 3.92 4.12 4.32 4.52 4.72 4.92

2 3.12 3.32 3.52 3.72 3.92 4.12 4.32 4.52 4.72 4.92 5.12

3 3.32 3.52 3.72 3.92 4.12 4.32 4.52 4.72 4.92 5.12 5.32

4 3.52 3.72 3.92 4.12 4.32 4.52 4.72 4.92 5.12 5.32 5.52

5 3.72 3.92 4.12 4.32 4.52 4.72 4.92 5.12 5.32 5.52 5.72

6 3.92 4.12 4.32 4.52 4.72 4.92 5.12 5.32 5.52 5.72 5.92

7 4.12 4.32 4.52 4.72 4.92 5.12 5.32 5.52 5.72 5.92 6.12

8 4.32 4.52 4.72 4.92 5.12 5.32 5.52 5.72 5.92 6.12 6.12

9 4.52 4.72 4.92 5.12 5.32 5.52 5.72 5.92 6.12 6.12 6.12

10 6.12 6.12 6.12 6.12 6.12 6.12 6.12 6.12 6.12 6.12 6.12