- 52 -

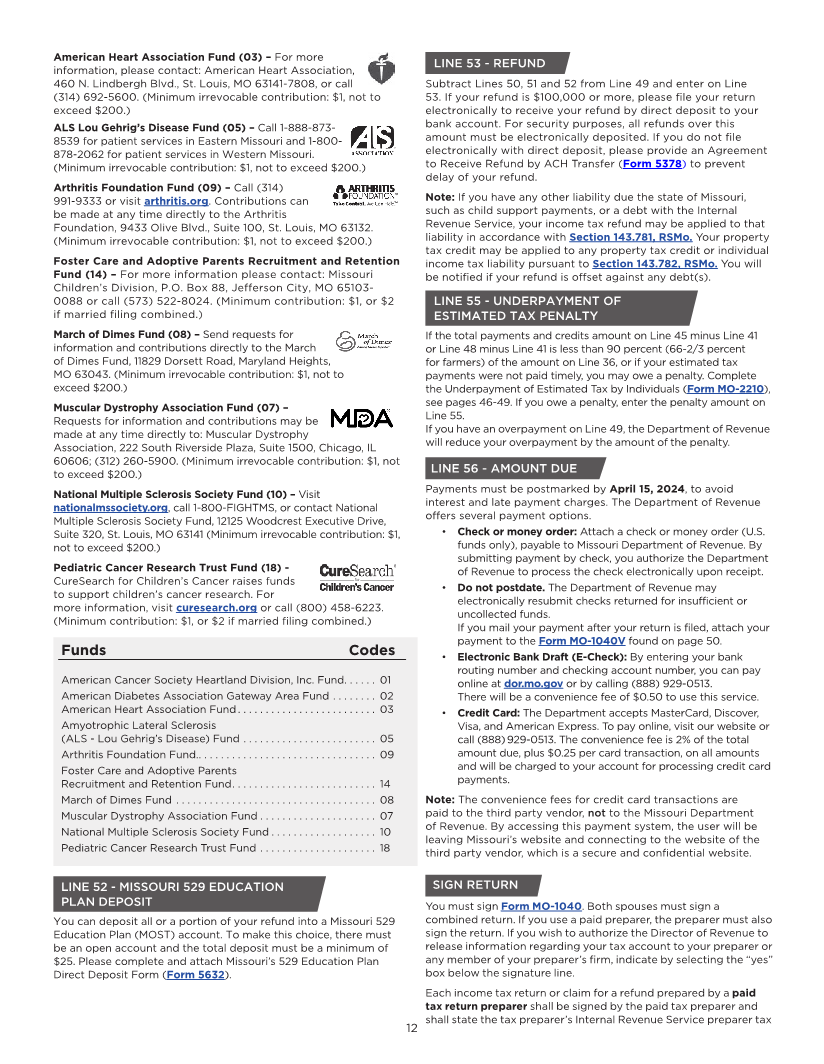

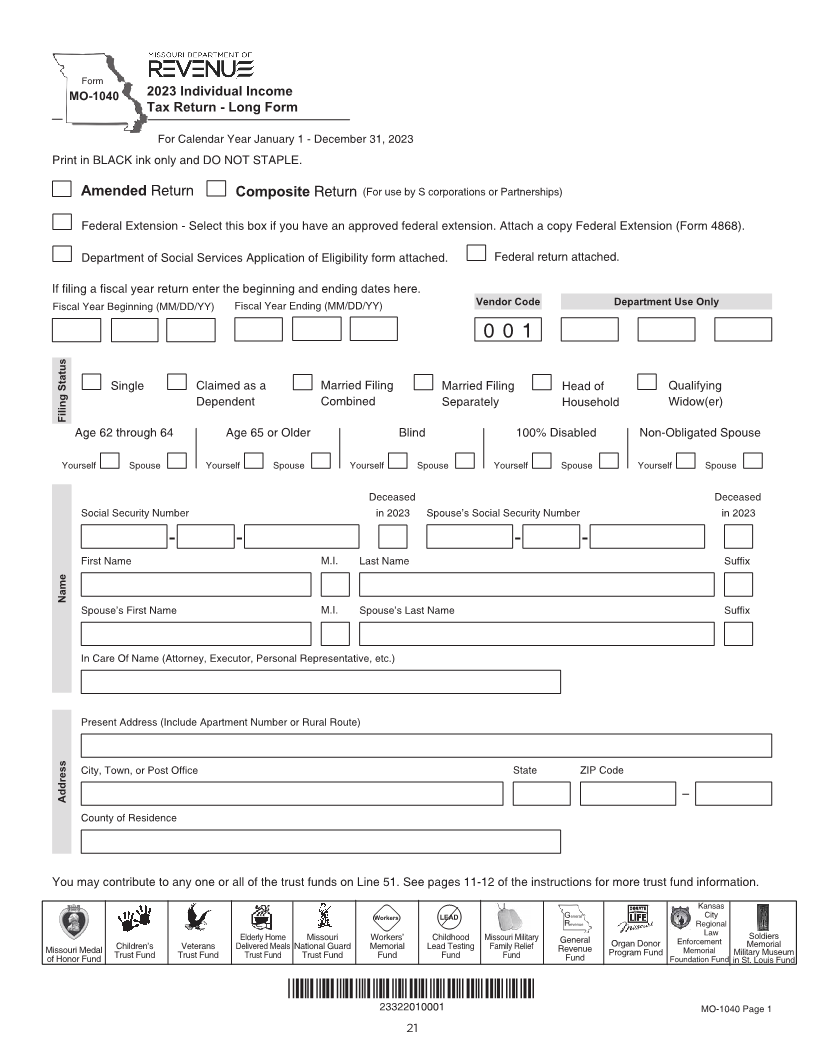

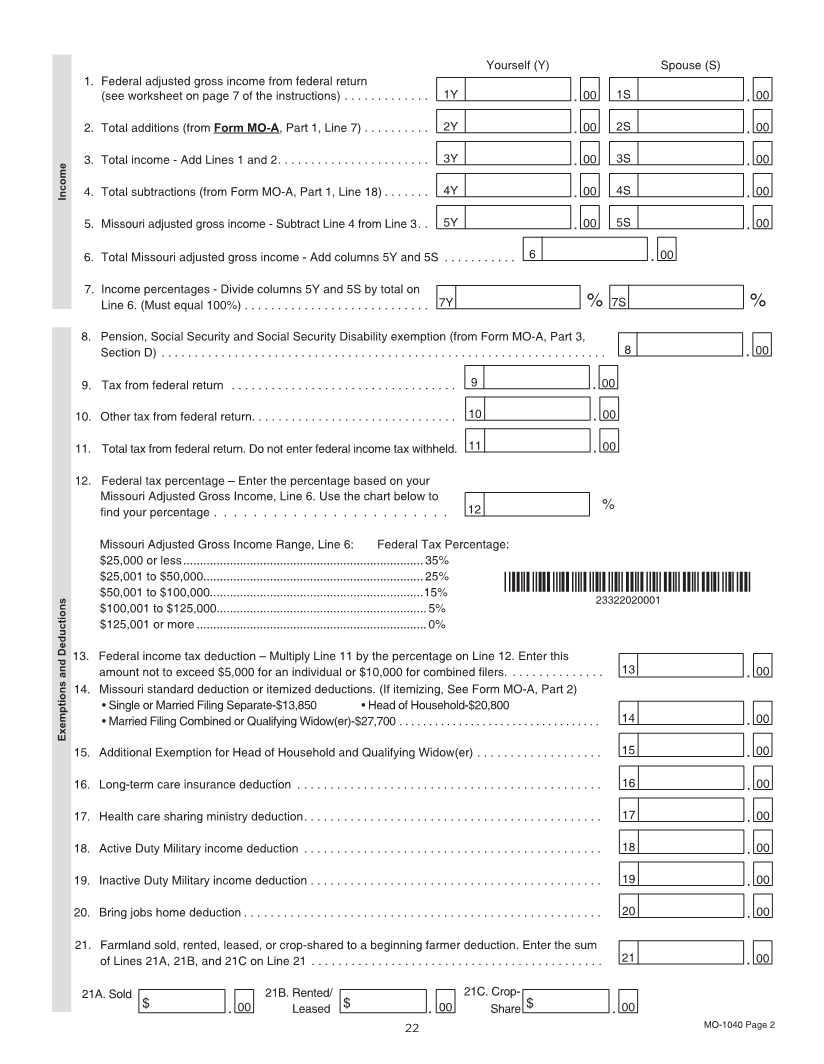

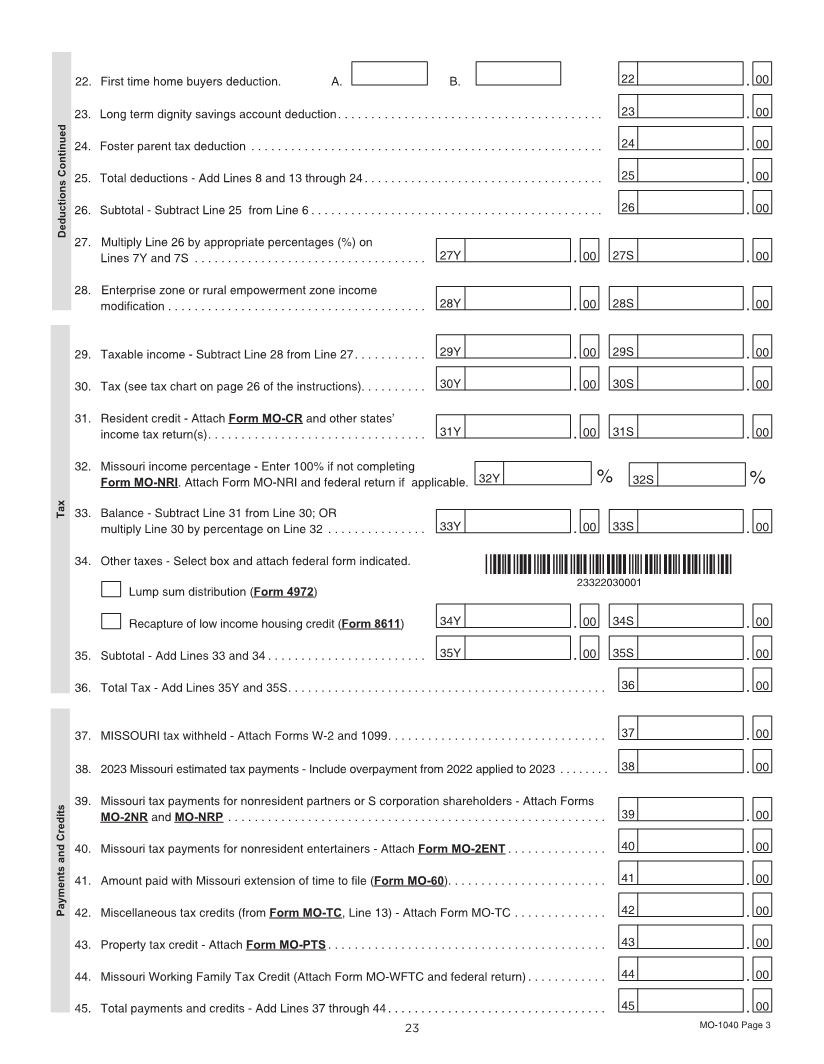

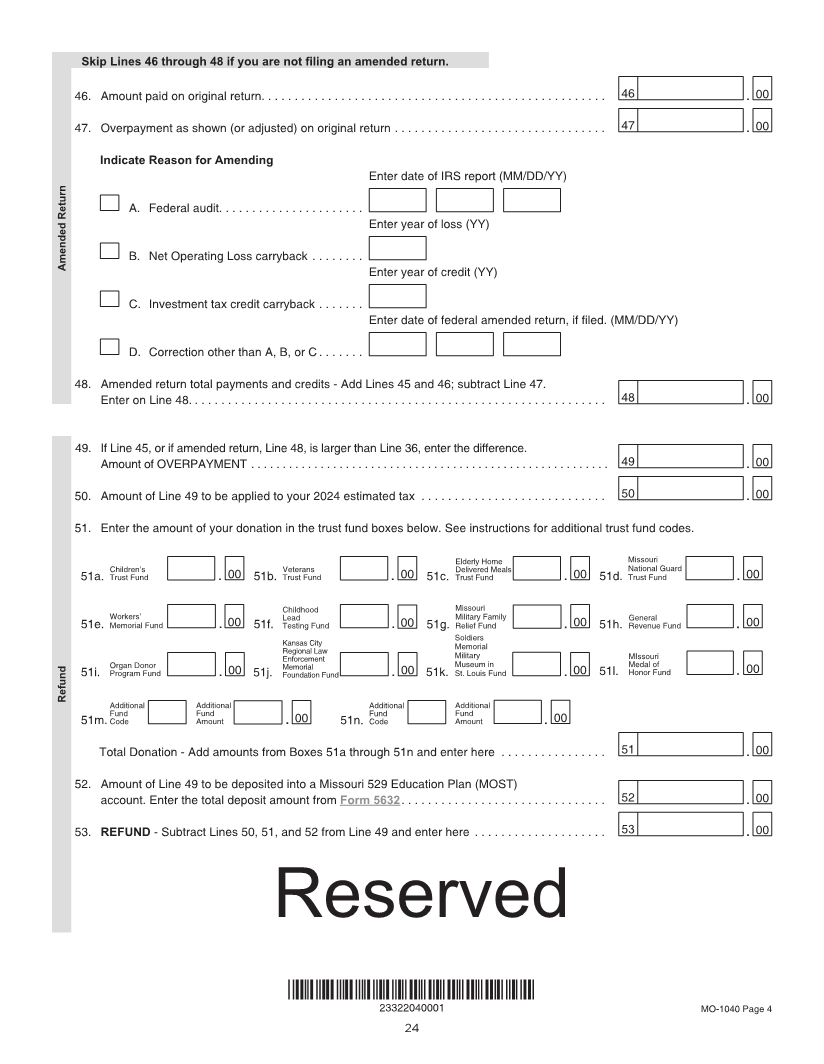

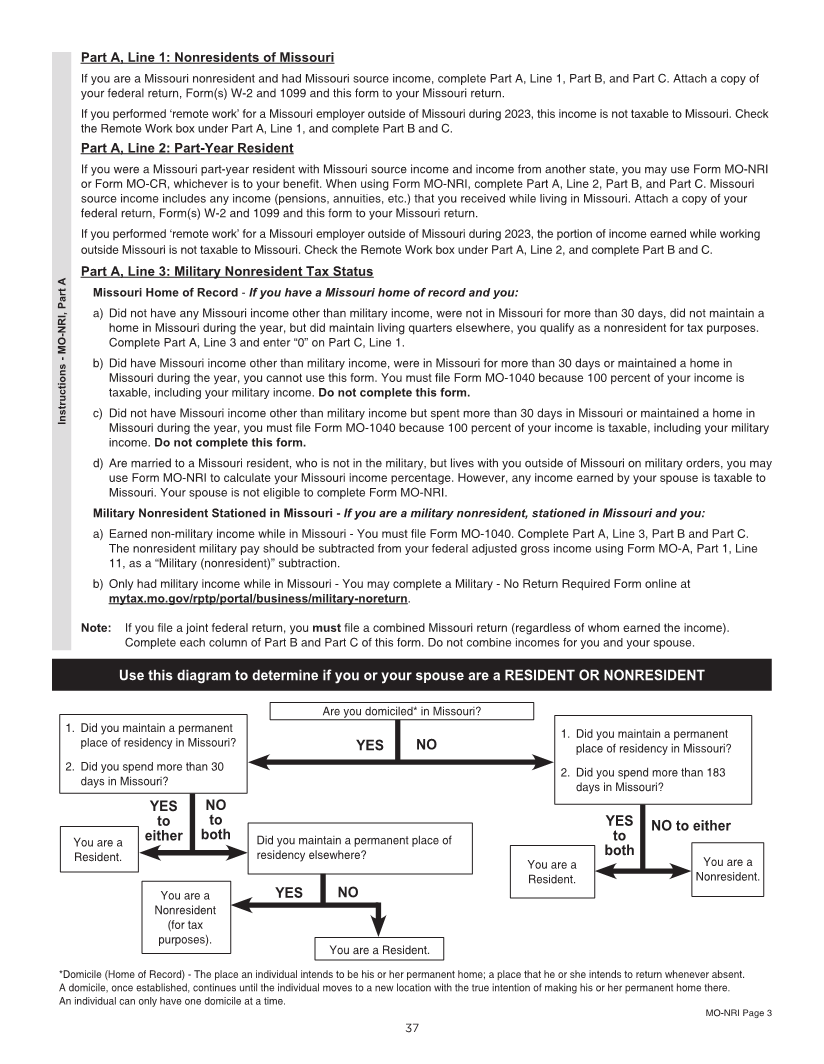

Enlarge image

|

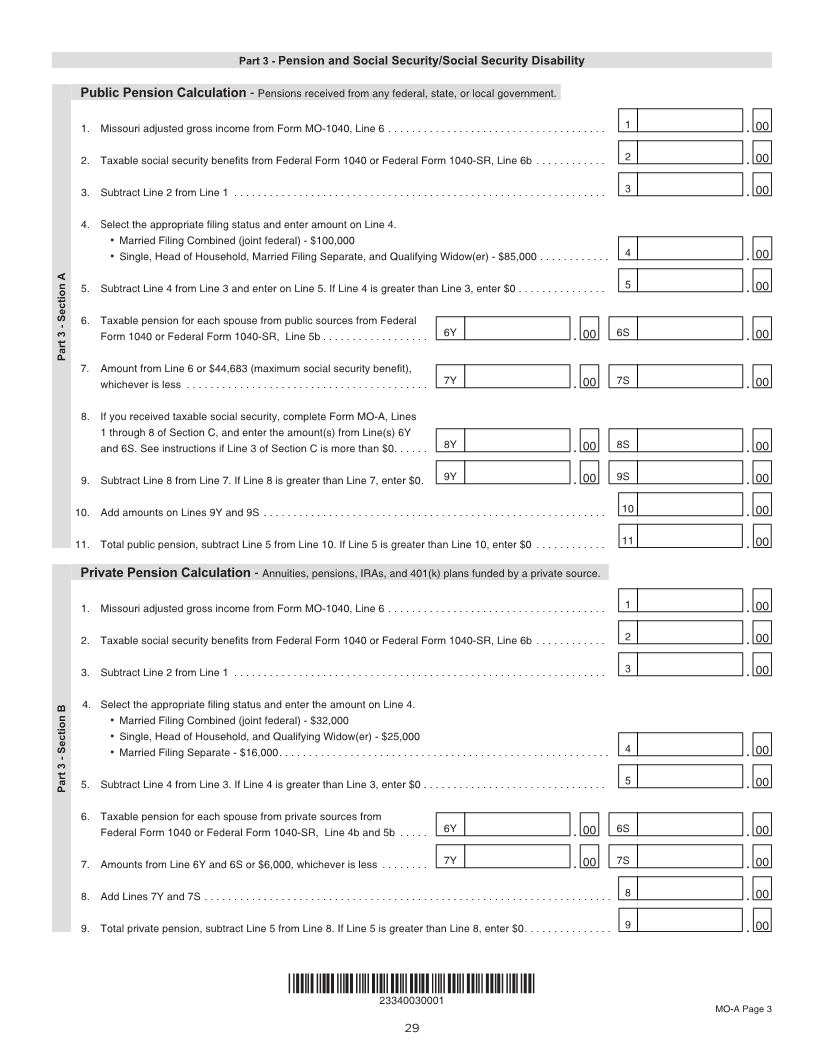

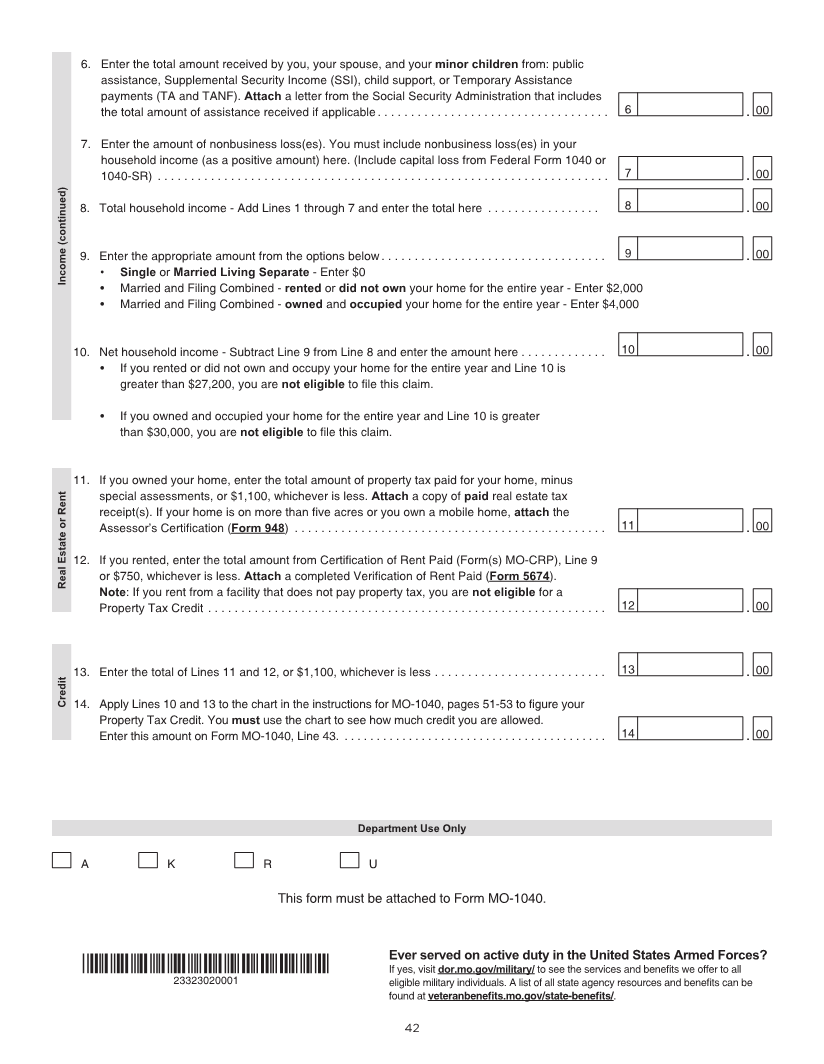

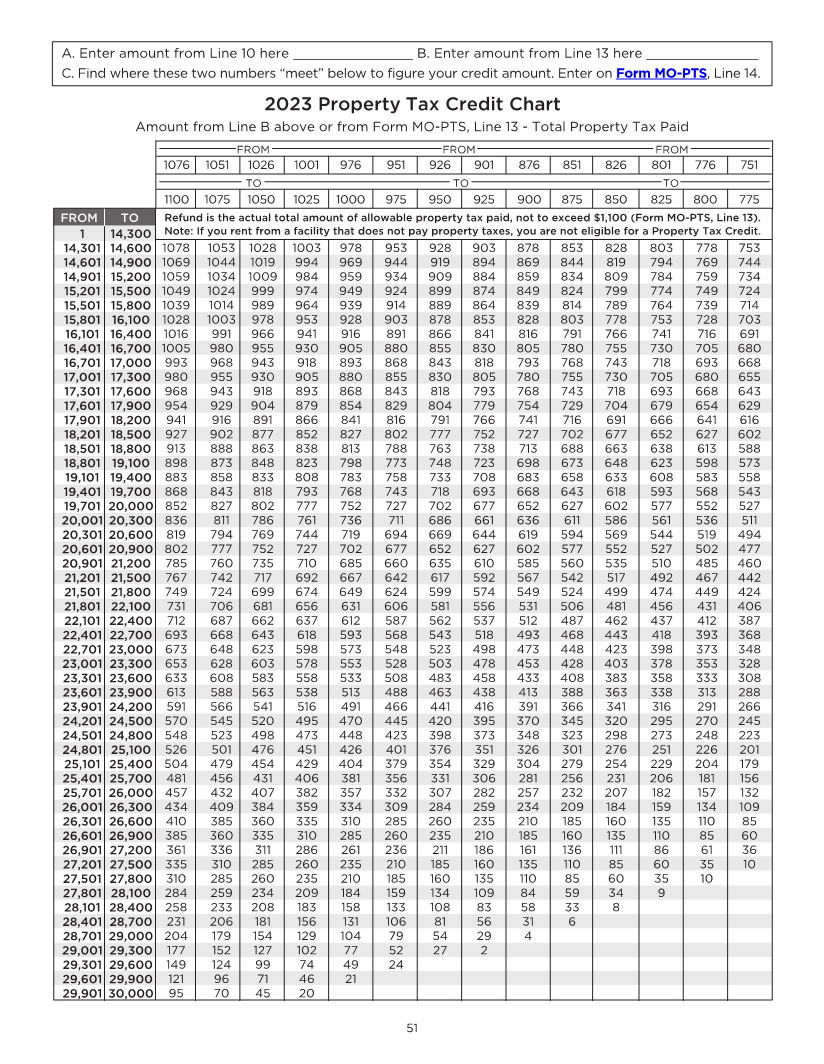

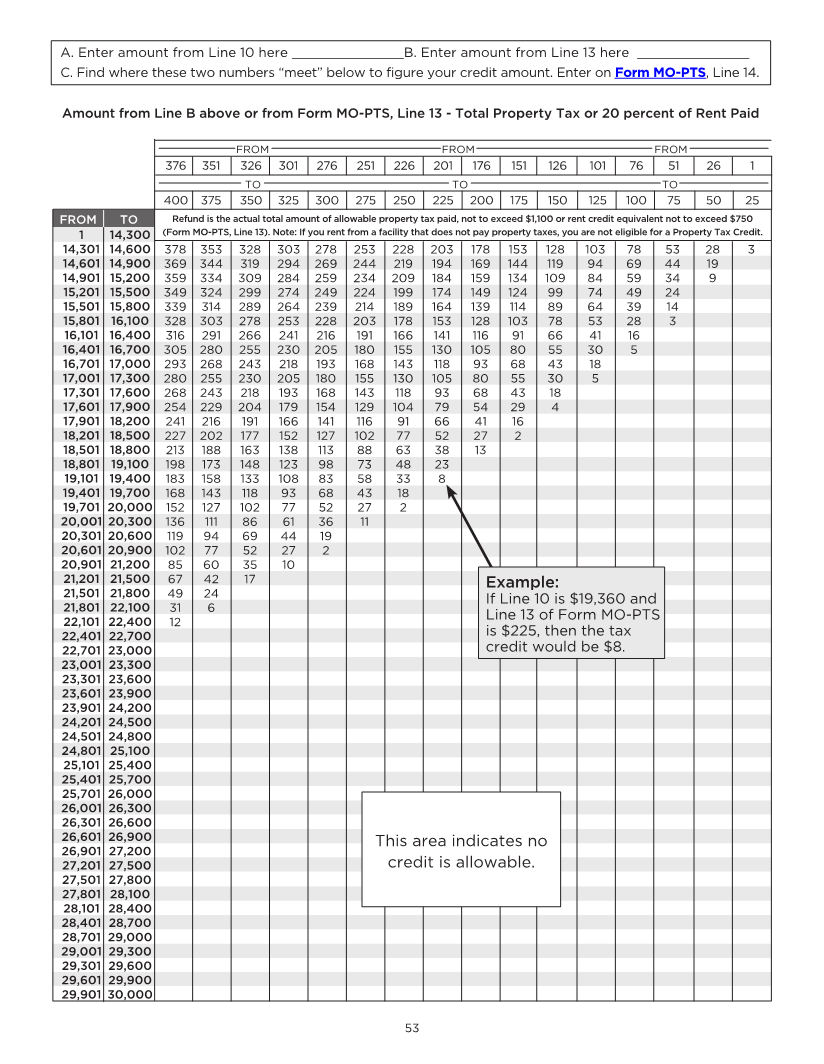

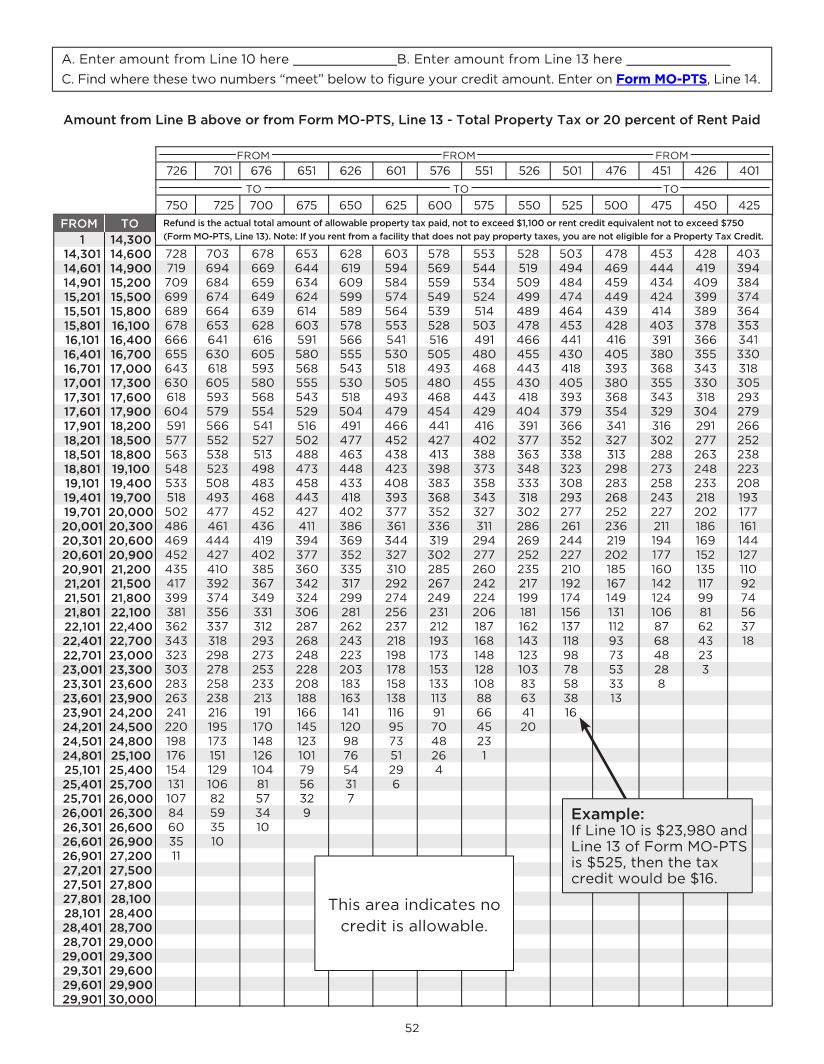

A. Enter amount from Line 10 here _____________B. Enter amount from Line 13 here _____________

C. Find where these two numbers “meet” below to figure your credit amount. Enter on Form MO-PTS, Line 14.

Amount from Line B above or from Form MO-PTS, Line 13 - Total Property Tax or 20 percent of Rent Paid

FROM FROM FROM

726 701 676 651 626 601 576 551 526 501 476 451 426 401

TO TO TO

750 725 700 675 650 625 600 575 550 525 500 475 450 425

FROM TO Refund is the actual total amount of allowable property tax paid, not to exceed $1,100 or rent credit equivalent not to exceed $750

1 14,300 (Form MO-PTS, Line 13). Note: If you rent from a facility that does not pay property taxes, you are not eligible for a Property Tax Credit.

14,301 14,600 728 703 678 653 628 603 578 553 528 503 478 453 428 403

14,601 14,900 719 694 669 644 619 594 569 544 519 494 469 444 419 394

14,901 15,200 709 684 659 634 609 584 559 534 509 484 459 434 409 384

15,201 15,500 699 674 649 624 599 574 549 524 499 474 449 424 399 374

15,501 15,800 689 664 639 614 589 564 539 514 489 464 439 414 389 364

15,801 16,100 678 653 628 603 578 553 528 503 478 453 428 403 378 353

16,101 16,400 666 641 616 591 566 541 516 491 466 441 416 391 366 341

16,401 16,700 655 630 605 580 555 530 505 480 455 430 405 380 355 330

16,701 17,000 643 618 593 568 543 518 493 468 443 418 393 368 343 318

17,001 17,300 630 605 580 555 530 505 480 455 430 405 380 355 330 305

17,301 17,600 618 593 568 543 518 493 468 443 418 393 368 343 318 293

17,601 17,900 604 579 554 529 504 479 454 429 404 379 354 329 304 279

17,901 18,200 591 566 541 516 491 466 441 416 391 366 341 316 291 266

18,201 18,500 577 552 527 502 477 452 427 402 377 352 327 302 277 252

18,501 18,800 563 538 513 488 463 438 413 388 363 338 313 288 263 238

18,801 19,100 548 523 498 473 448 423 398 373 348 323 298 273 248 223

19,101 19,400 533 508 483 458 433 408 383 358 333 308 283 258 233 208

19,401 19,700 518 493 468 443 418 393 368 343 318 293 268 243 218 193

19,701 20,000 502 477 452 427 402 377 352 327 302 277 252 227 202 177

20,001 20,300 486 461 436 411 386 361 336 311 286 261 236 211 186 161

20,301 20,600 469 444 419 394 369 344 319 294 269 244 219 194 169 144

20,601 20,900 452 427 402 377 352 327 302 277 252 227 202 177 152 127

20,901 21,200 435 410 385 360 335 310 285 260 235 210 185 160 135 110

21,201 21,500 417 392 367 342 317 292 267 242 217 192 167 142 117 92

21,501 21,800 399 374 349 324 299 274 249 224 199 174 149 124 99 74

21,801 22,100 381 356 331 306 281 256 231 206 181 156 131 106 81 56

22,101 22,400 362 337 312 287 262 237 212 187 162 137 112 87 62 37

22,401 22,700 343 318 293 268 243 218 193 168 143 118 93 68 43 18

22,701 23,000 323 298 273 248 223 198 173 148 123 98 73 48 23

23,001 23,300 303 278 253 228 203 178 153 128 103 78 53 28 3

23,301 23,600 283 258 233 208 183 158 133 108 83 58 33 8

23,601 23,900 263 238 213 188 163 138 113 88 63 38 13

23,901 24,200 241 216 191 166 141 116 91 66 41 16

24,201 24,500 220 195 170 145 120 95 70 45 20

24,501 24,800 198 173 148 123 98 73 48 23

24,801 25,100 176 151 126 101 76 51 26 1

25,101 25,400 154 129 104 79 54 29 4

25,401 25,700 131 106 81 56 31 6

25,701 26,000 107 82 57 32 7

26,001 26,300 84 59 34 9 Example:

26,301 26,600 60 35 10 If Line 10 is $23,980 and

26,601 26,900 35 10 Line 13 of Form MO-PTS

26,901 27,200 11

is $525, then the tax

27,201 27,500

27,501 27,800 credit would be $16.

27,801 28,100

This area indicates no

28,101 28,400

28,401 28,700 credit is allowable.

28,701 29,000

29,001 29,300

29,301 29,600

29,601 29,900

29,901 30,000

52

|