Enlarge image

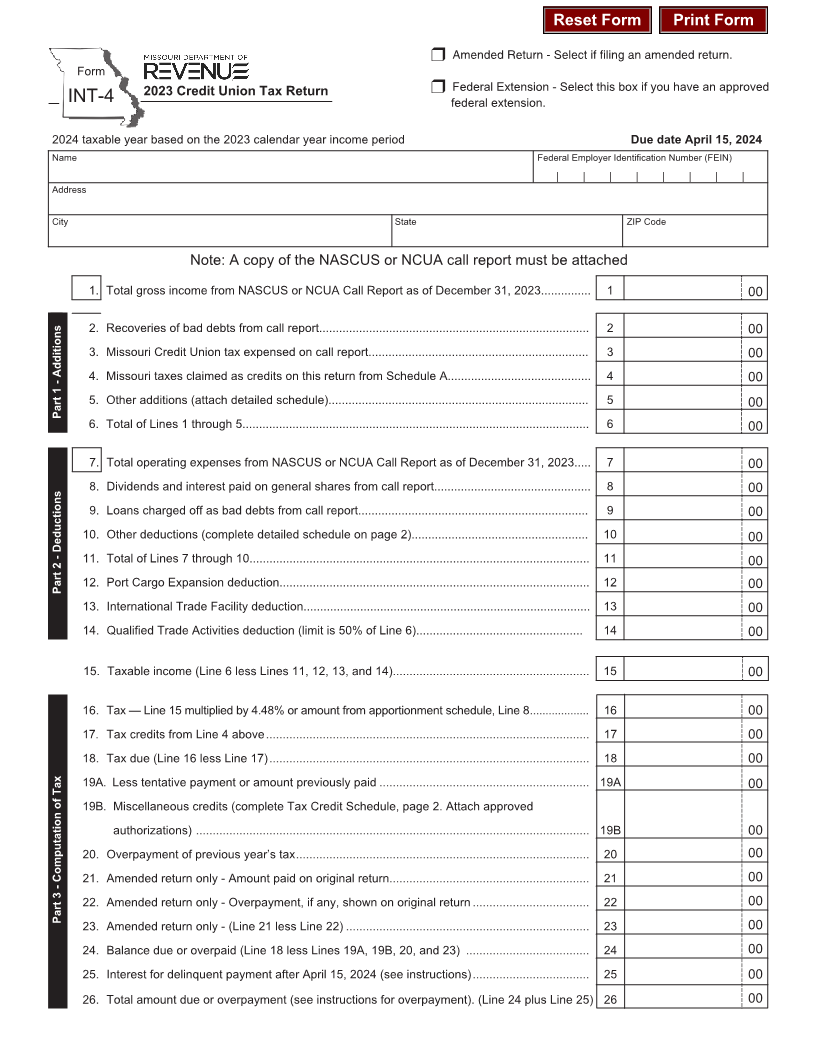

Reset Form Print Form

r Amended Return - Select if filing an amended return.

Form

2023 Credit Union Tax Return r Federal Extension - Select this box if you have an approved

INT-4 federal extension.

2024 taxable year based on the 2023 calendar year income period Due date April 15, 2024

Name Federal Employer Identification Number (FEIN)

| | | | | | | |

Address

City State ZIP Code

Note: A copy of the NASCUS or NCUA call report must be attached

1. Total gross income from NASCUS or NCUA Call Report as of December 31, 2023............... 1 00

2. Recoveries of bad debts from call report................................................................................. 2 00

3. Missouri Credit Union tax expensed on call report.................................................................. 3 00

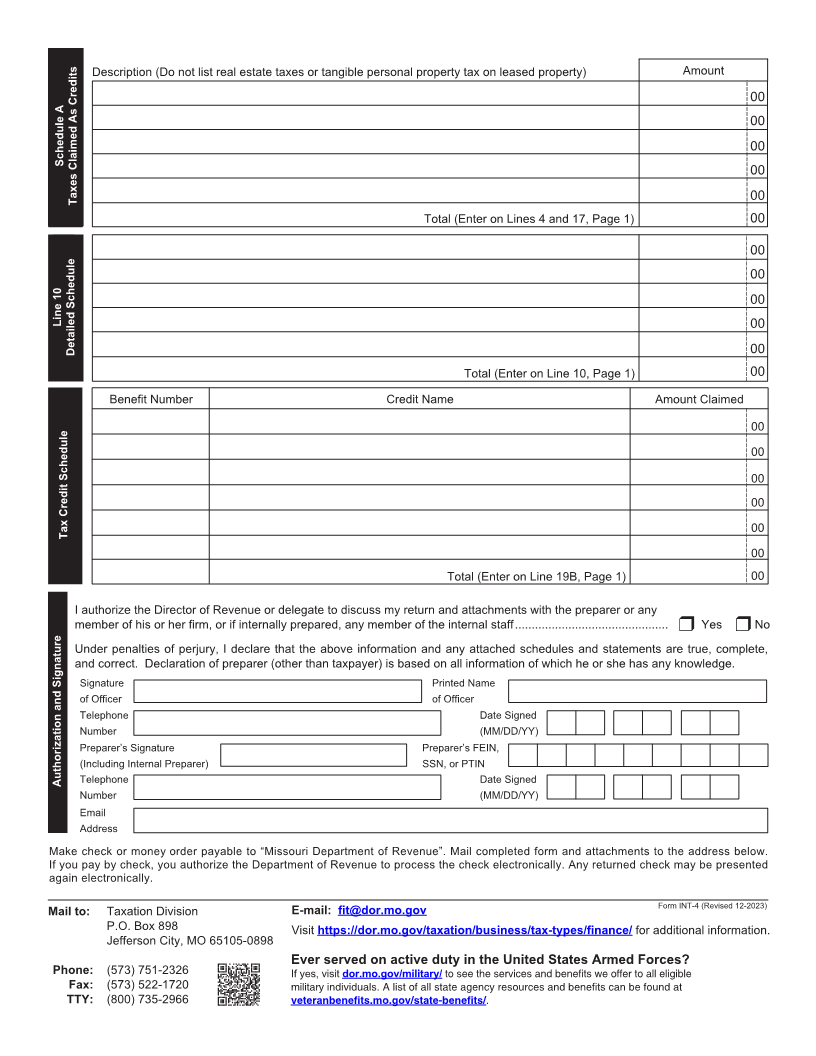

4. Missouri taxes claimed as credits on this return from Schedule A........................................... 4 00

5. Other additions (attach detailed schedule).............................................................................. 5 00

Part 1 - Additions

6. Total of Lines 1 through 5........................................................................................................ 6 00

7. Total operating expenses from NASCUS or NCUA Call Report as of December 31, 2023..... 7 00

8. Dividends and interest paid on general shares from call report............................................... 8 00

9. Loans charged off as bad debts from call report..................................................................... 9 00

10. Other deductions (complete detailed schedule on page 2)..................................................... 10 00

11. Total of Lines 7 through 10...................................................................................................... 11 00

Part 2 - Deductions 12. Port Cargo Expansion deduction............................................................................................. 12 00

13. International Trade Facility deduction...................................................................................... 13 00

14. Qualified Trade Activities deduction (limit is 50% of Line 6).................................................. 14 00

15. Taxable income (Line 6 less Lines 11, 12, 13, and 14)........................................................... 15 00

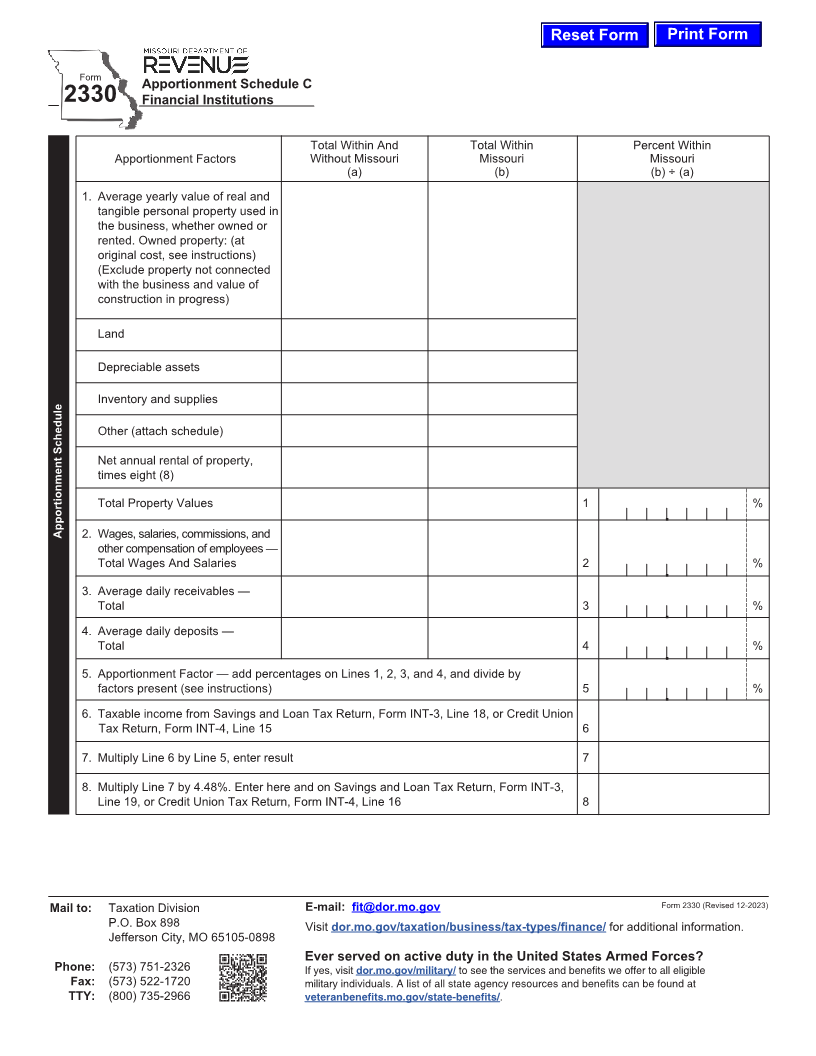

16. Tax — Line 15 multiplied by 4.48% or amount from apportionment schedule, Line 8 ................... 16 00

17. Tax credits from Line 4 above ................................................................................................. 17 00

18. Tax due (Line 16 less Line 17) ................................................................................................ 18 00

19A. Less tentative payment or amount previously paid ............................................................... 19A 00

19B. Miscellaneous credits (complete Tax Credit Schedule, page 2. Attach approved

authorizations) ...................................................................................................................... 19B 00

20. Overpayment of previous year’s tax ........................................................................................ 20 00

21. Amended return only - Amount paid on original return............................................................ 21 00

22. Amended return only - Overpayment, if any, shown on original return ................................... 22 00

Part 3 - Computation of Tax

23. Amended return only - (Line 21 less Line 22) ......................................................................... 23 00

24. Balance due or overpaid (Line 18 less Lines 19A, 19B, 20, and 23) ..................................... 24 00

25. Interest for delinquent payment after April 15, 2024 (see instructions) ................................... 25 00

26. Total amount due or overpayment (see instructions for overpayment). (Line 24 plus Line 25) 26 00