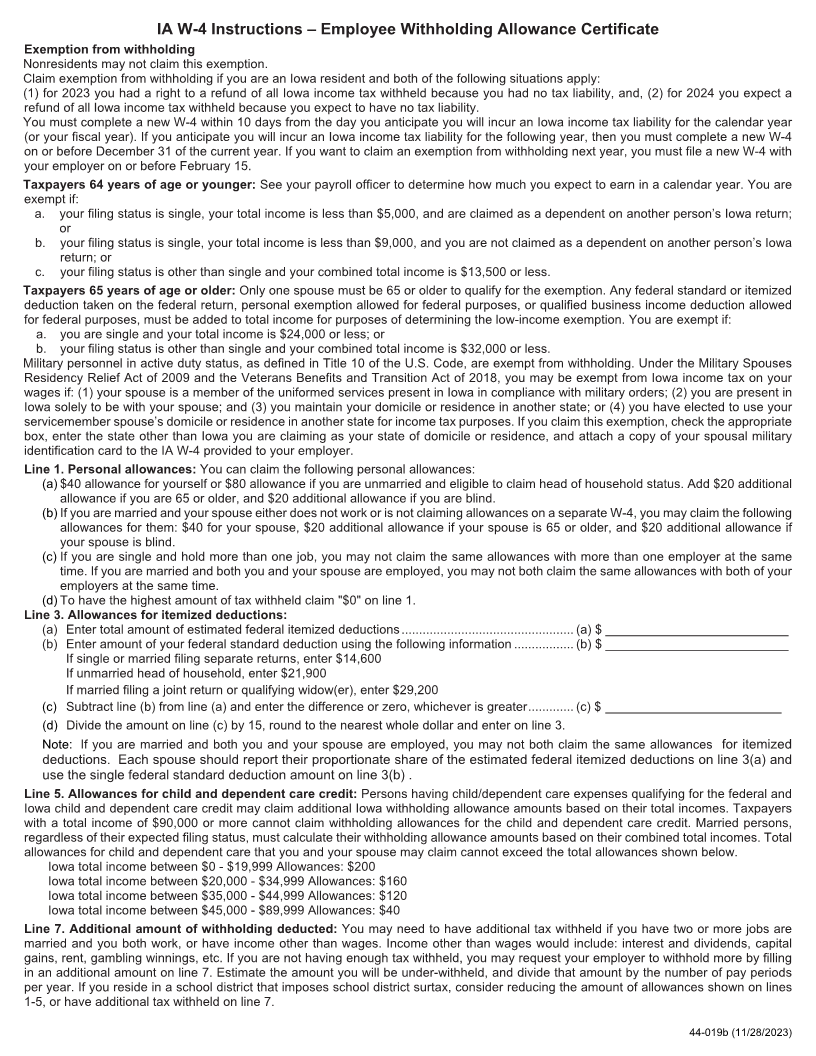

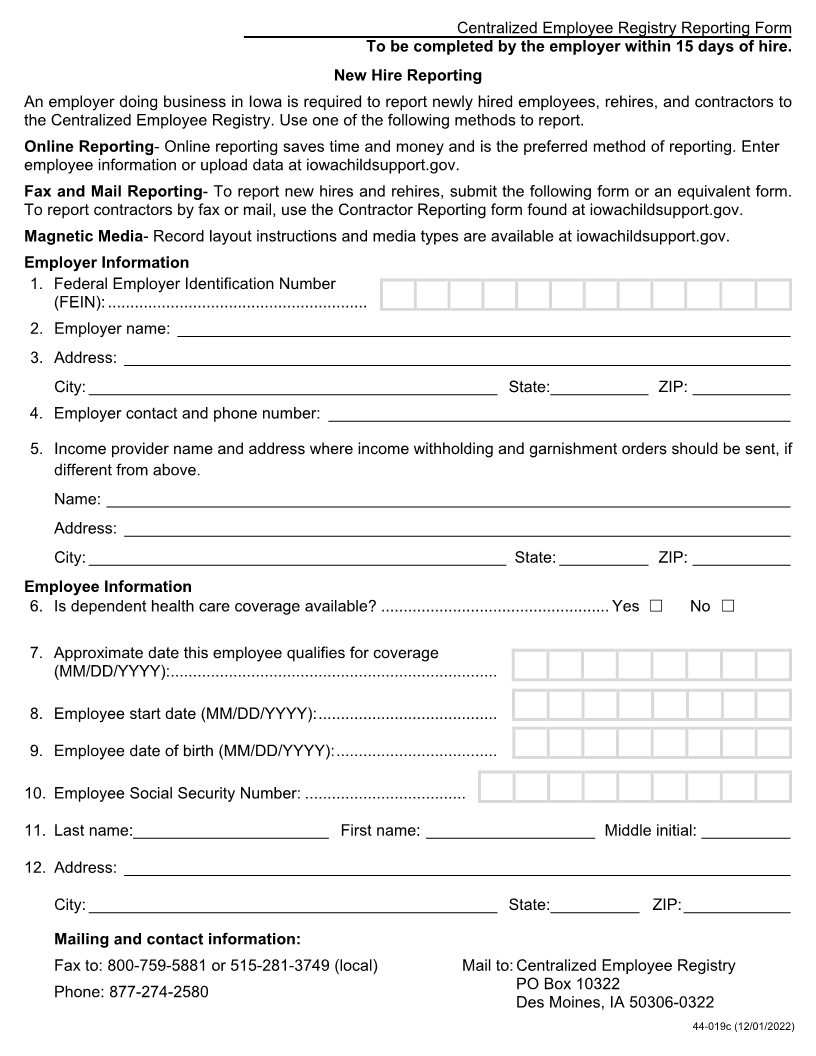

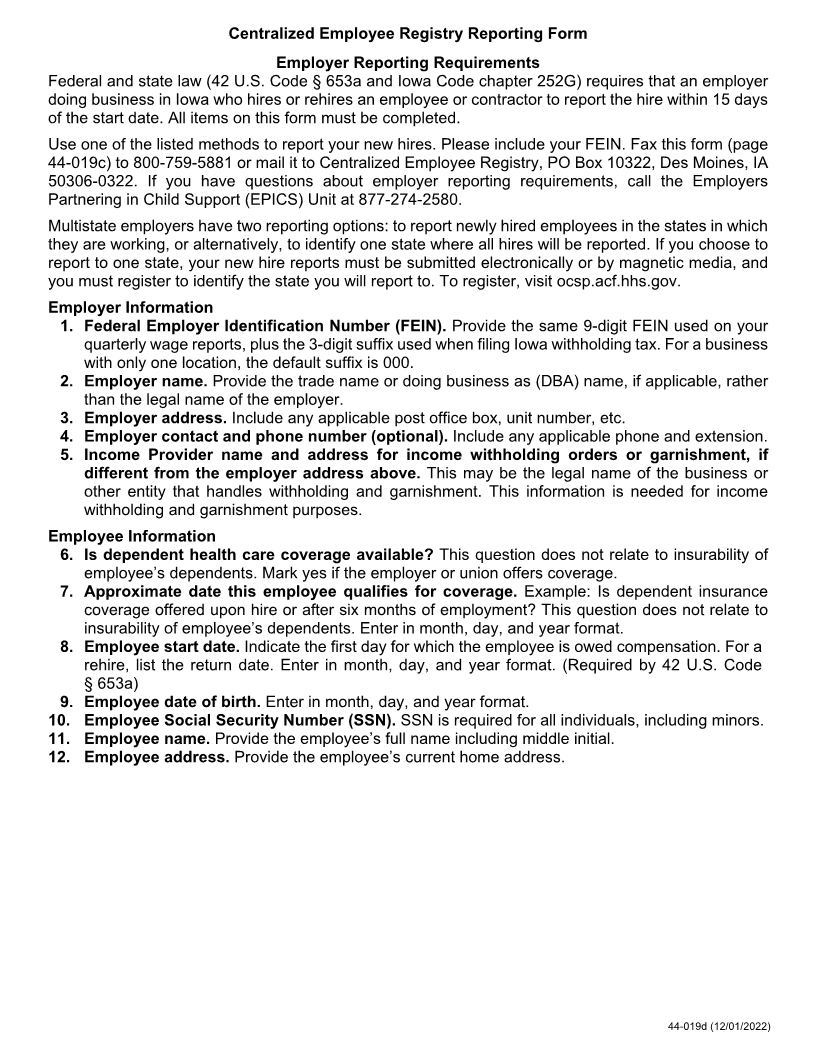

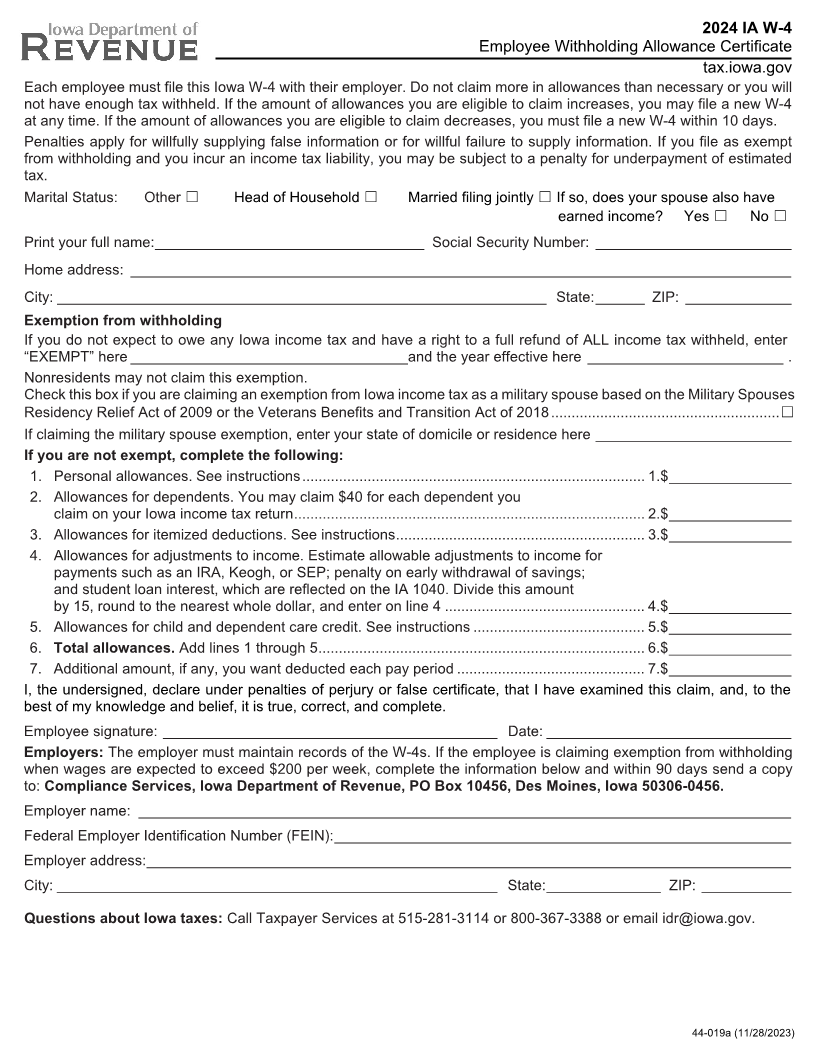

Enlarge image

2024 IA W-4

Employee Withholding Allowance Certificate

tax.iowa.gov

Each employee must file this Iowa W-4 with their employer. Do not claim more in allowances than necessary or you will

not have enough tax withheld. If the amount of allowances you are eligible to claim increases, you may file a new W-4

at any time. If the amount of allowances you are eligible to claim decreases, you must file a new W-4 within 10 days.

Penalties apply for willfully supplying false information or for willful failure to supply information. If you file as exempt

from withholding and you incur an income tax liability, you may be subject to a penalty for underpayment of estimated

tax.

Marital Status: Other ☐ Head of Household ☐ Married filing jointly ☐ If so, does your spouse also have

earned income? Yes ☐ No ☐

Print your full name: _________________________________ Social Security Number: ________________________

Home address: _________________________________________________________________________________

City: ____________________________________________________________ State: ______ ZIP: _____________

Exemption from withholding

If you do not expect to owe any Iowa income tax and have a right to a full refund of ALL income tax withheld, enter

“EXEMPT” here __________________________________and the year effective here ________________________ .

Nonresidents may not claim this exemption.

Check this box if you are claiming an exemption from Iowa income tax as a military spouse based on the Military Spouses

Residency Relief Act of 2009 or the Veterans Benefits and Transition Act of 2018 ........................................................ ☐

If claiming the military spouse exemption, enter your state of domicile or residence here ________________________

If you are not exempt, complete the following:

1. Personal allowances. See instructions .................................................................................... 1.$ _______________

2. Allowances for dependents. You may claim $40 for each dependent you

claim on your Iowa income tax return ...................................................................................... 2.$ _______________

3. Allowances for itemized deductions. See instructions ............................................................. 3.$ _______________

4. Allowances for adjustments to income. Estimate allowable adjustments to income for

payments such as an IRA, Keogh, or SEP; penalty on early withdrawal of savings;

and student loan interest, which are reflected on the IA 1040. Divide this amount

by 15, round to the nearest whole dollar, and enter on line 4 ................................................. 4.$ _______________

5. Allowances for child and dependent care credit. See instructions .......................................... 5.$ _______________

6. Total allowances. Add lines 1 through 5 ................................................................................ 6.$ _______________

7. Additional amount, if any, you want deducted each pay period .............................................. 7.$ _______________

I, the undersigned, declare under penalties of perjury or false certificate, that I have examined this claim, and, to the

best of my knowledge and belief, it is true, correct, and complete.

Employee signature: _________________________________________ Date: ______________________________

Employers: The employer must maintain records of the W-4s. If the employee is claiming exemption from withholding

when wages are expected to exceed $200 per week, complete the information below and within 90 days send a copy

to: Compliance Services, Iowa Department of Revenue, PO Box 10456, Des Moines, Iowa 50306-0456.

Employer name: ________________________________________________________________________________

Federal Employer Identification Number (FEIN): ________________________________________________________

Employer address: _______________________________________________________________________________

City: ______________________________________________________ State: ______________ ZIP: ___________

Questions about Iowa taxes: Call Taxpayer Services at 515-281-3114 or 800-367-3388 or email idr@iowa.gov.

44-019a (11/28/2023)