Enlarge image

Reset Form Print Form

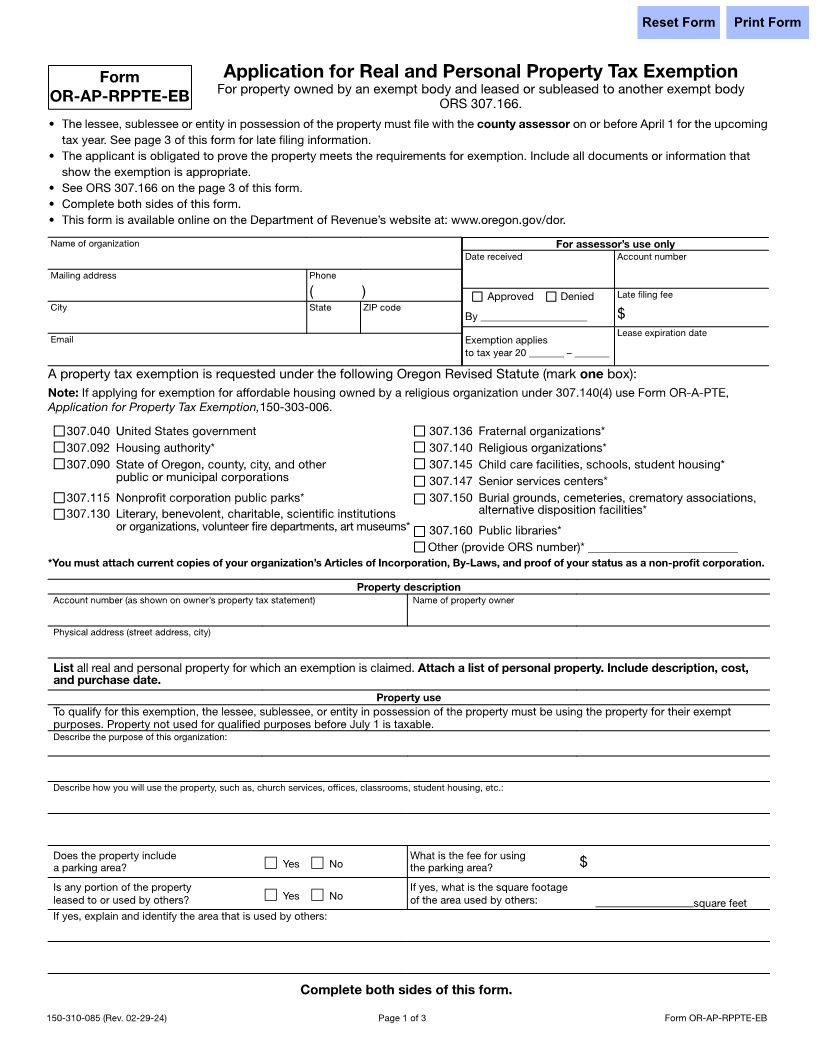

Form Application for Real and Personal Property Tax Exemption

For property owned by an exempt body and leased or subleased to another exempt body

OR-AP-RPPTE-EB ORS 307.166.

• The lessee, sublessee or entity in possession of the property must file with the county assessor on or before April 1 for the upcoming

tax year. See page 3 of this form for late filing information.

• The applicant is obligated to prove the property meets the requirements for exemption. Include all documents or information that

show the exemption is appropriate.

• See ORS 307.166 on the page 3 of this form.

• Complete both sides of this form.

• This form is available online on the Department of Revenue’s website at: www.oregon.gov/dor.

Name of organization For assessor’s use only

Date received Account number

Mailing address Phone

( ) Approved Denied Late filing fee

City State ZIP code

By ____________________ $

Lease expiration date

E mail Exemption applies

to tax year 20 _______ – _______

A property tax exemption is requested under the following Oregon Revised Statute (mark one box):

Note: If applying for exemption for affordable housing owned by a religious organization under 307.140(4) use Form OR-A-PTE,

Application for Property Tax Exemption,150-303-006.

307.040 United States government 307.136 Fraternal organizations*

307.092 Housing authority* 307.140 Religious organizations*

307.090 State of Oregon, county, city, and other 307.145 Child care facilities, schools, student housing*

public or municipal corporations 307.147 Senior services centers*

307.115 Nonprofit corporation public parks* 307.150 Burial grounds, cemeteries, crematory associations,

307.130 Literary, benevolent, charitable, scientific institutions alternative disposition facilities*

or organizations, volunteer fire departments, art museums* 307.160 Public libraries*

Other (provide ORS number)* _________________________

*You must attach current copies of your organization’s Articles of Incorporation, By-Laws, and proof of your status as a non-profit corporation.

Property description

Account number (as shown on owner’s property tax statement) Name of property owner

Physical address (street address, city)

List all real and personal property for which an exemption is claimed. Attach a list of personal property. Include description, cost,

and purchase date.

Property use

To qualify for this exemption, the lessee, sublessee, or entity in possession of the property must be using the property for their exempt

purposes. Property not used for qualified purposes before July 1 is taxable.

Describe the purpose of this organization:

Describe how you will use the property, such as, church services, offices, classrooms, student housing, etc.:

Does the property include What is the fee for using

a parking area? c Yes c No the parking area? $

Is any portion of the property If yes, what is the square footage

leased to or used by others? c Yes c No of the area used by others: ______________square feet

If yes, explain and identify the area that is used by others:

Complete both sides of this form.

150-310-085 (Rev. 02-29-24) Page 1 of 3 Form OR-AP-RPPTE-EB