Enlarge image

1 1

1 2 2 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 Form With grid With grid & data2 84 85

3 4 82 83

3 3

4 4

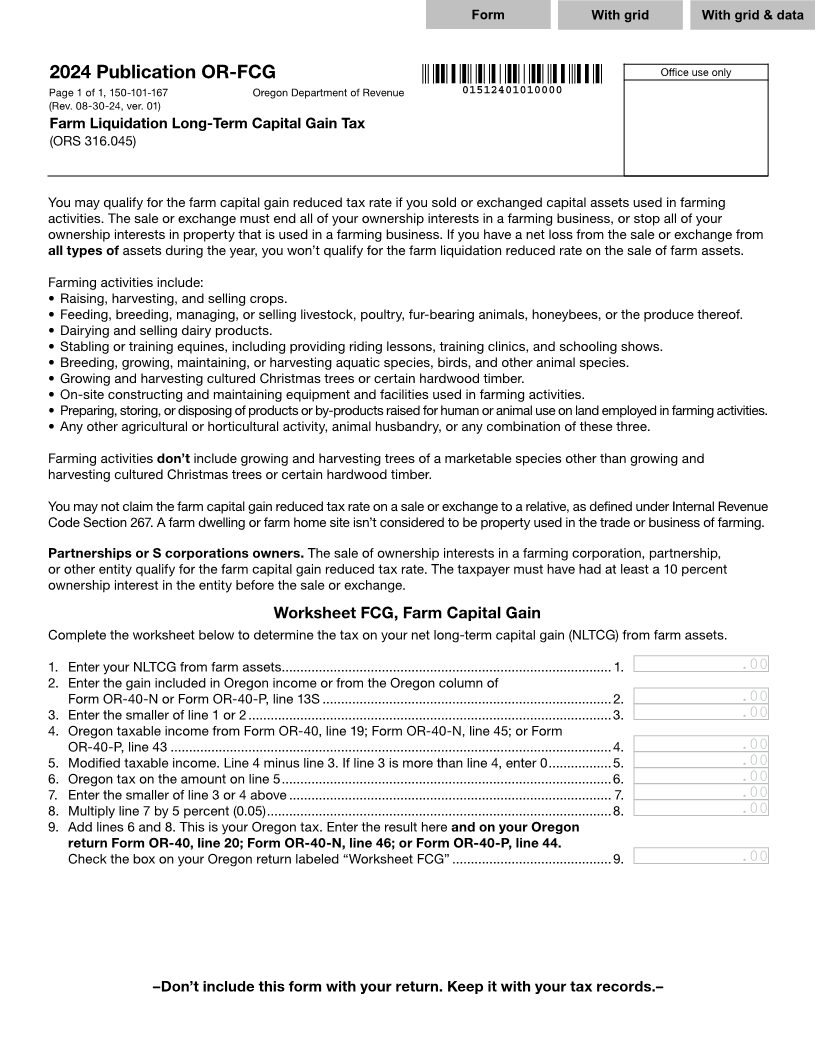

5 2024 Publication OR-FCG Office use only 5

6 Page 1 of 1, 150-101-167 Oregon Department of Revenue 01512401010000 6

7 (Rev. 08-30-24, ver. 01) 7

8 Farm Liquidation Long-Term Capital Gain Tax 8

9 9

(ORS 316.045)

10 10

11 11

12 12

13 You may qualify for the farm capital gain reduced tax rate if you sold or exchanged capital assets used in farming 13

14 activities. The sale or exchange must end all of your ownership interests in a farming business, or stop all of your 14

15 ownership interests in property that is used in a farming business. If you have a net loss from the sale or exchange from 15

16 all types of assets during the year, you won’t qualify for the farm liquidation reduced rate on the sale of farm assets. 16

17 17

18 Farming activities include: 18

19 • Raising, harvesting, and selling crops. 19

20 • Feeding, breeding, managing, or selling livestock, poultry, fur-bearing animals, honeybees, or the produce thereof. 20

21 • Dairying and selling dairy products. 21

22 • Stabling or training equines, including providing riding lessons, training clinics, and schooling shows. 22

23 • Breeding, growing, maintaining, or harvesting aquatic species, birds, and other animal species. 23

24 • Growing and harvesting cultured Christmas trees or certain hardwood timber. 24

25 • On-site constructing and maintaining equipment and facilities used in farming activities. 25

26 • Preparing, storing, or disposing of products or by-products raised for human or animal use on land employed in farming activities. 26

27 • Any other agricultural or horticultural activity, animal husbandry, or any combination of these three. 27

28 28

29 Farming activities don’t include growing and harvesting trees of a marketable species other than growing and 29

30 harvesting cultured Christmas trees or certain hardwood timber. 30

31 31

32 You may not claim the farm capital gain reduced tax rate on a sale or exchange to a relative, as defined under Internal Revenue 32

33 Code Section 267. A farm dwelling or farm home site isn’t considered to be property used in the trade or business of farming. 33

34 34

35 Partnerships or S corporations owners. The sale of ownership interests in a farming corporation, partnership, 35

36 or other entity qualify for the farm capital gain reduced tax rate. The taxpayer must have had at least a 10 percent 36

37 ownership interest in the entity before the sale or exchange. 37

38 38

39 Worksheet FCG, Farm Capital Gain 39

40 Complete the worksheet below to determine the tax on your net long-term capital gain (NLTCG) from farm assets. 40

41 41

42 1. Enter your NLTCG from farm assets ......................................................................................... 1. 999,999,999.00.00 42

43 2. Enter the gain included in Oregon income or from the Oregon column of 43

44 Form OR-40-N or Form OR-40-P, line 13S ..............................................................................2. 999,999,999.00.00 44

45 3. Enter the smaller of line 1 or 2 ..................................................................................................3. 999,999,999.00.00 45

46 4. Oregon taxable income from Form OR-40, line 19; Form OR-40-N, line 45; or Form 46

47 OR-40-P, line 43 .......................................................................................................................4. 999,999,999.00.00 47

48 5. Modified taxable income. Line 4 minus line 3. If line 3 is more than line 4, enter 0 .................5. 999,999,999.00.00 48

49 6. Oregon tax on the amount on line 5 .........................................................................................6. 999,999,999.00.00 49

50 7. Enter the smaller of line 3 or 4 above ....................................................................................... 7. 999,999,999.00.00 50

51 8. Multiply line 7 by 5 percent (0.05) .............................................................................................8. 999,999,999.00.00 51

52 9. Add lines 6 and 8. This is your Oregon tax. Enter the result here and on your Oregon 52

53 return Form OR-40, line 20; Form OR-40-N, line 46; or Form OR-40-P, line 44. 53

54 Check the box on your Oregon return labeled “Worksheet FCG” ...........................................9. 999,999,999.00.00 54

55 55

56 56

57 57

58 58

59 59

60 60

61 61

62 –Don’t include this form with your return. Keep it with your tax records.– 62

63 63

64 64

1 2 65 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 65 84 85

3 4 82 83

66 66