Enlarge image

Form OR-706 Instructions

Oregon Estate Transfer Tax 2024

This publication is a guide, not a complete statement, of Oregon Revised Statutes (ORS) and Oregon Administrative Rules (OAR).

For possible updates and more information, refer to the laws and rules on our website, www.oregon.gov/dor.

Contents

Purpose of Form OR-706 ......................................................2 Forest Conservation Tax Credit ...........................................5

Amount paid by the due date of the return ......................6

What’s new ...............................................................................2 Penalty due .............................................................................6

Interest due .............................................................................6

Important .................................................................................2 Total due .................................................................................6

Executor signature .................................................................6

Overview ...................................................................................2 Authorization .........................................................................6

Filing requirements ...............................................................2

Who must file the return ......................................................2 Part 3: Elections by the executor .......................................7

When to file return—due date ............................................2 Alternate valuation ................................................................7

Special use valuation of Section 2032A ..............................7

Return mailing addresses and payment instructions ...3 Reversionary or remainder interests ..................................7

Returns ....................................................................................3

Payment only..........................................................................3 Part 4: General information ................................................7

Private delivery services .......................................................3 Surviving spouse ...................................................................7

Amended returns ..................................................................3 Beneficiary information........................................................7

Forms and schedules ............................................................3 Section 2044 property ...........................................................7

Insurance not included in the gross estate ........................7

Part 1: Decedent and executor information ..................4 Partnership interests and stock in closely

Decedent name and SSN ......................................................4 held corporations ...................................................................7

Decedent domicile .................................................................4 Trusts .......................................................................................8

Extensions ...............................................................................4

Part 5: Recapitulation ...........................................................8

Separate election checkbox ..................................................4

Executor name and address ................................................4 Conservation easement exclusion .......................................8

Deductions ..............................................................................8

Part 2: Tax computation ...................................................... 4 Marital deduction—Schedule M .........................................8

Rounding off to whole dollars ............................................ 4

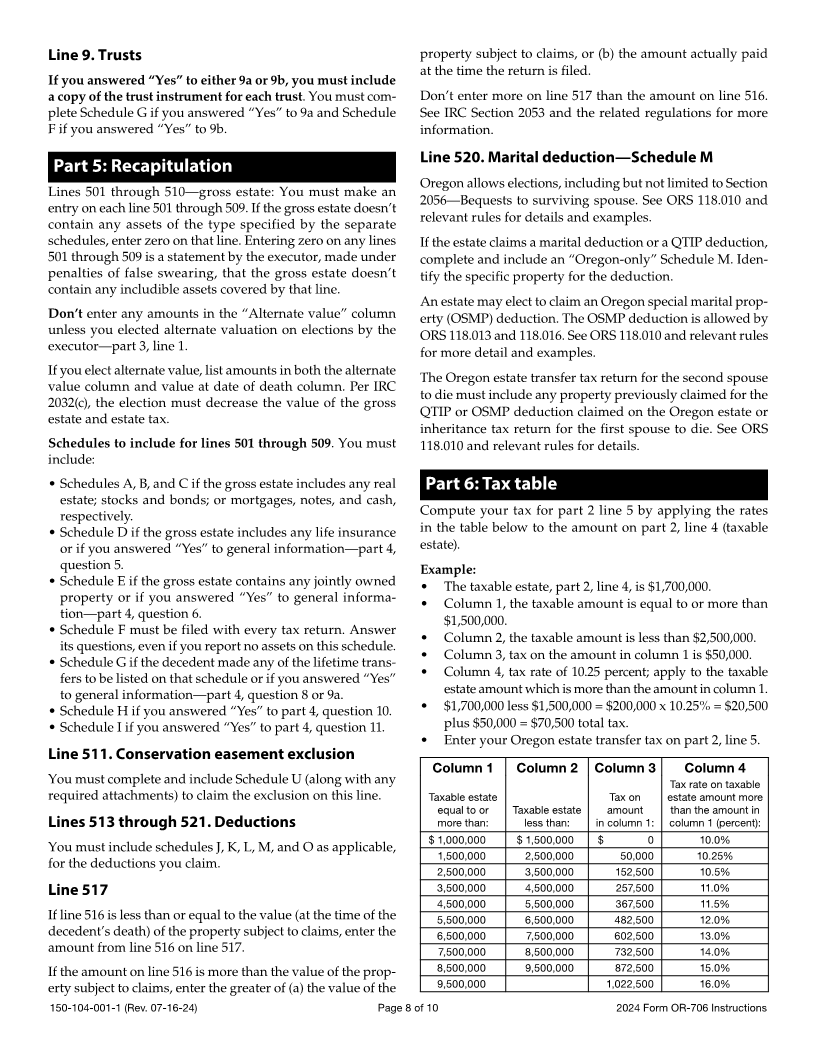

Part 6: Tax table ......................................................................8

Total gross estate ...................................................................4

Natural resource property exemption ................................4 Assembly and processing.....................................................9

Disposition of qualifying property and additional Filing checklist for Form OR-706 .........................................9

tax due .....................................................................................5 What happens after you file the tax return? .....................9

Oregon estate tax. ..................................................................5 Installment payments ...........................................................9

Gross value of property located in Oregon .......................5

Oregon percentage ................................................................5 Survivor information .......................................................... 10

Tax payable to Oregon ..........................................................5 Definitions ............................................................................ 10

Natural resource and commercial

fishing business credit ..........................................................5 Do you have questions or need help? ............................ 10

Visit www.oregon.gov/dor for potential updates.

150-104-001-1 (Rev. 07-16-24) Page 1 of 10 2024 Form OR-706 Instructions