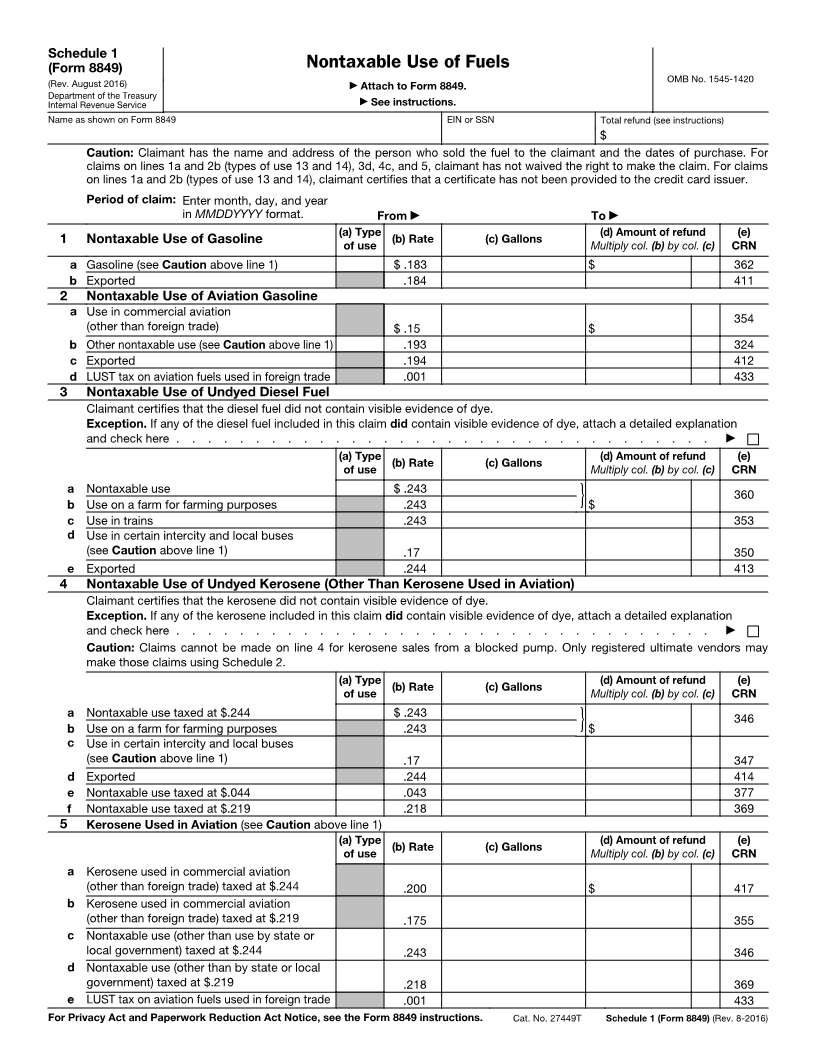

Enlarge image

Schedule 1

(Form 8849) Nontaxable Use of Fuels

(Rev. August 2016) ▶ Attach to Form 8849. OMB No. 1545-1420

Department of the Treasury ▶ See instructions.

Internal Revenue Service

Name as shown on Form 8849 EIN or SSN Total refund (see instructions)

$

Caution: Claimant has the name and address of the person who sold the fuel to the claimant and the dates of purchase. For

claims on lines 1a and 2b (types of use 13 and 14), 3d, 4c, and 5, claimant has not waived the right to make the claim. For claims

on lines 1a and 2b (types of use 13 and 14), claimant certifies that a certificate has not been provided to the credit card issuer.

Period of claim: Enter month, day, and year

in MMDDYYYY format. From ▶ To ▶

(a) Type (d) Amount of refund (e)

(b) Rate (c) Gallons

1 Nontaxable Use of Gasoline of use Multiply col. (b) by col. (c) CRN

a Gasoline (see Caution above line 1) $ .183 $ 362

b Exported .184 411

2 Nontaxable Use of Aviation Gasoline

a Use in commercial aviation

354

(other than foreign trade) $ .15 $

b Other nontaxable use (see Caution above line 1) .193 324

c Exported .194 412

d LUST tax on aviation fuels used in foreign trade .001 433

3 Nontaxable Use of Undyed Diesel Fuel

Claimant certifies that the diesel fuel did not contain visible evidence of dye.

Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach a detailed explanation

and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

(a) Type (d) Amount of refund (e)

(b) Rate (c) Gallons

of use Multiply col. (b) by col. (c) CRN

a Nontaxable use $ .243 360

b Use on a farm for farming purposes .243 } $

c Use in trains .243 353

d Use in certain intercity and local buses

(see Caution above line 1) .17 350

e Exported .244 413

4 Nontaxable Use of Undyed Kerosene (Other Than Kerosene Used in Aviation)

Claimant certifies that the kerosene did not contain visible evidence of dye.

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach a detailed explanation

and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

Caution: Claims cannot be made on line 4 for kerosene sales from a blocked pump. Only registered ultimate vendors may

make those claims using Schedule 2.

(a) Type (d) Amount of refund (e)

(b) Rate (c) Gallons

of use Multiply col. (b) by col. (c) CRN

a Nontaxable use taxed at $.244 $ .243 346

b Use on a farm for farming purposes .243 } $

c Use in certain intercity and local buses

(see Caution above line 1) .17 347

d Exported .244 414

e Nontaxable use taxed at $.044 .043 377

f Nontaxable use taxed at $.219 .218 369

5 Kerosene Used in Aviation (see Caution above line 1)

(a) Type (d) Amount of refund (e)

(b) Rate (c) Gallons

of use Multiply col. (b) by col. (c) CRN

a Kerosene used in commercial aviation

(other than foreign trade) taxed at $.244 .200 $ 417

b Kerosene used in commercial aviation

(other than foreign trade) taxed at $.219 .175 355

c Nontaxable use (other than use by state or

local government) taxed at $.244 .243 346

d Nontaxable use (other than by state or local

government) taxed at $.219 .218 369

e LUST tax on aviation fuels used in foreign trade .001 433

For Privacy Act and Paperwork Reduction Act Notice, see the Form 8849 instructions. Cat. No. 27449T Schedule 1 (Form 8849) (Rev. 8-2016)