Enlarge image

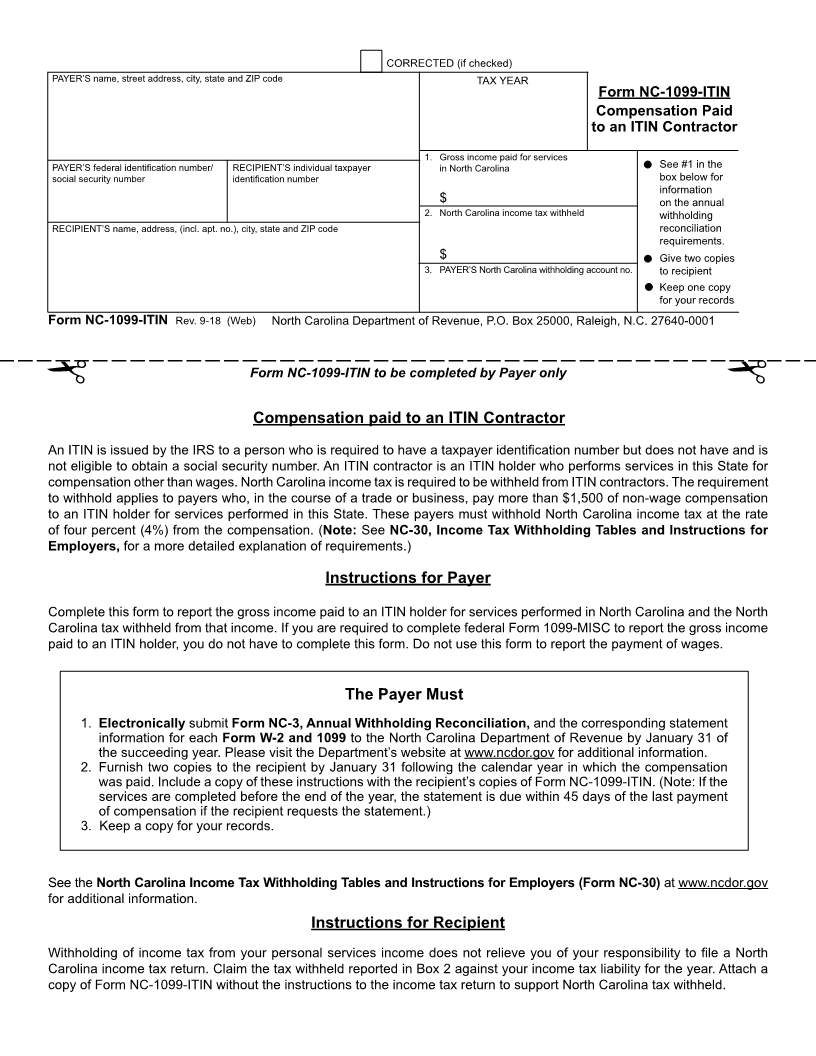

CORRECTED (if checked)

PAYER’S name, street address, city, state and ZIP code TAX YEAR

Form NC-1099-ITIN

Compensation Paid

to an ITIN Contractor

1. Gross income paid for services

PAYER’S federal identification number/ RECIPIENT’S individual taxpayer in North Carolina See #1 in the

social security number identification number box below for

information

$ on the annual

2. North Carolina income tax withheld withholding

RECIPIENT’S name, address, (incl. apt. no.), city, state and ZIP code reconciliation

requirements.

$ Give two copies

3. PAYER’S North Carolina withholding account no. to recipient

Keep one copy

for your records

Form NC-1099-ITIN Rev. 9-18 (Web) North Carolina Department of Revenue, P.O. Box 25000, Raleigh, N.C. 27640-0001

Form NC-1099-ITIN to be completed by Payer only

Compensation paid to an ITIN Contractor

An ITIN is issued by the IRS to a person who is required to have a taxpayer identification number but does not have and is

not eligible to obtain a social security number. An ITIN contractor is an ITIN holder who performs services in this State for

compensation other than wages. North Carolina income tax is required to be withheld from ITIN contractors. The requirement

to withhold applies to payers who, in the course of a trade or business, pay more than $1,500 of non-wage compensation

to an ITIN holder for services performed in this State. These payers must withhold North Carolina income tax at the rate

of four percent (4%) from the compensation. (Note: See NC-30, Income Tax Withholding Tables and Instructions for

Employers, for a more detailed explanation of requirements.)

Instructions for Payer

Complete this form to report the gross income paid to an ITIN holder for services performed in North Carolina and the North

Carolina tax withheld from that income. If you are required to complete federal Form 1099-MISC to report the gross income

paid to an ITIN holder, you do not have to complete this form. Do not use this form to report the payment of wages.

The Payer Must

1. Electronically submit Form NC-3, Annual Withholding Reconciliation, and the corresponding statement

information for each Form W-2 and 1099 to the North Carolina Department of Revenue by January 31 of

the succeeding year. Please visit the Department’s website at www.ncdor.gov for additional information.

2. Furnish two copies to the recipient by January 31 following the calendar year in which the compensation

was paid. Include a copy of these instructions with the recipient’s copies of Form NC-1099-ITIN. (Note: If the

services are completed before the end of the year, the statement is due within 45 days of the last payment

of compensation if the recipient requests the statement.)

3. Keep a copy for your records.

See the North Carolina Income Tax Withholding Tables and Instructions for Employers (Form NC-30) at www.ncdor.gov

for additional information.

Instructions for Recipient

Withholding of income tax from your personal services income does not relieve you of your responsibility to file a North

Carolina income tax return. Claim the tax withheld reported in Box 2 against your income tax liability for the year. Attach a

copy of Form NC-1099-ITIN without the instructions to the income tax return to support North Carolina tax withheld.