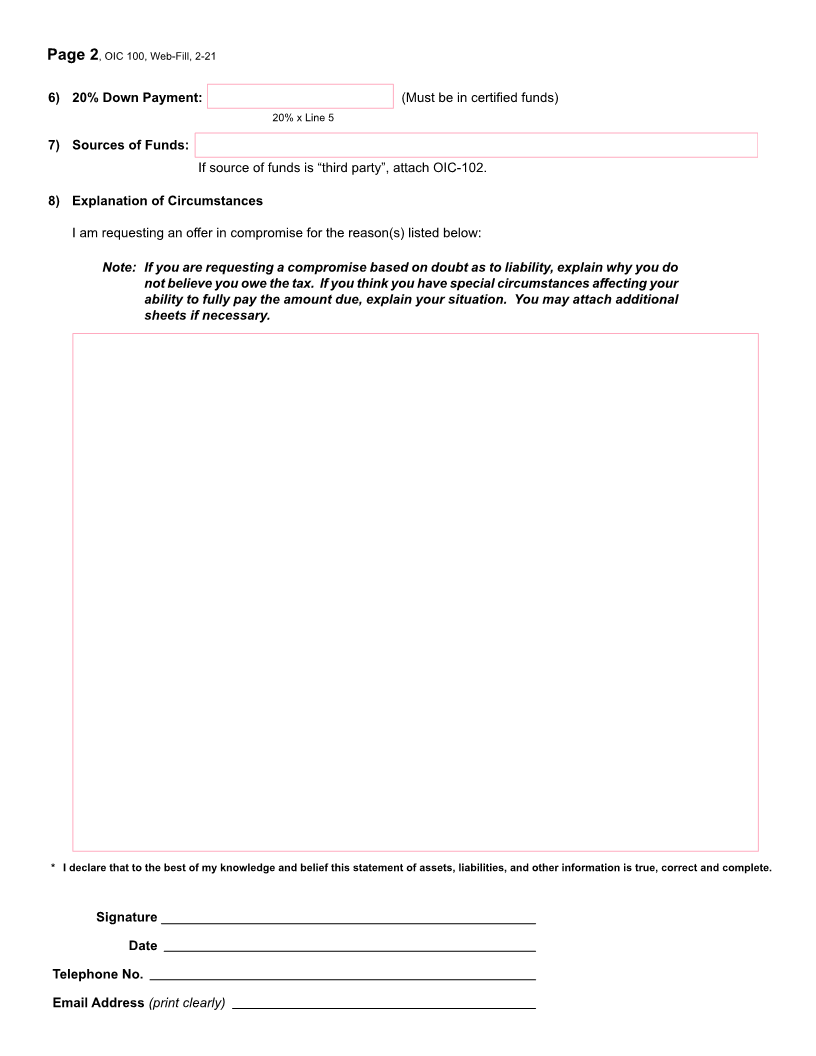

Enlarge image

4 6

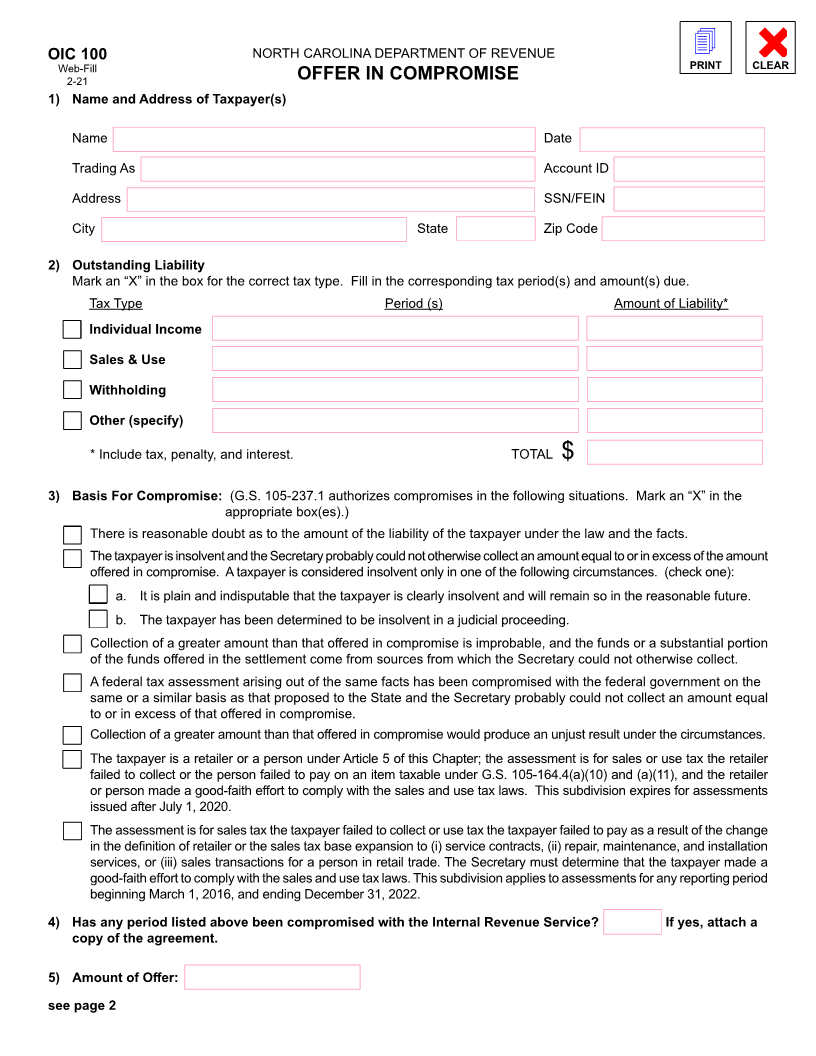

OIC 100 NORTH CAROLINA DEPARTMENT OF REVENUE PRINT CLEAR

Web-Fill

2-21 OFFER IN COMPROMISE

1) Name and Address of Taxpayer(s)

Name Date

Trading As Account ID

Address SSN/FEIN

City State Zip Code

2) Outstanding Liability

Mark an “X” in the box for the correct tax type. Fill in the corresponding tax period(s) and amount(s) due.

Tax Type Period (s) Amount of Liability*

Individual Income

Sales & Use

Withholding

Other (specify)

* Include tax, penalty, and interest. TOTAL $

3) Basis For Compromise: (G.S. 105-237.1 authorizes compromises in the following situations. Mark an “X” in the

appropriate box(es).)

There is reasonable doubt as to the amount of the liability of the taxpayer under the law and the facts.

The taxpayer is insolvent and the Secretary probably could not otherwise collect an amount equal to or in excess of the amount

offered in compromise. A taxpayer is considered insolvent only in one of the following circumstances. (check one):

a. It is plain and indisputable that the taxpayer is clearly insolvent and will remain so in the reasonable future.

b. The taxpayer has been determined to be insolvent in a judicial proceeding.

Collection of a greater amount than that offered in compromise is improbable, and the funds or a substantial portion

of the funds offered in the settlement come from sources from which the Secretary could not otherwise collect.

A federal tax assessment arising out of the same facts has been compromised with the federal government on the

same or a similar basis as that proposed to the State and the Secretary probably could not collect an amount equal

to or in excess of that offered in compromise.

Collection of a greater amount than that offered in compromise would produce an unjust result under the circumstances.

The taxpayer is a retailer or a person under Article 5 of this Chapter; the assessment is for sales or use tax the retailer

failed to collect or the person failed to pay on an item taxable under G.S. 105-164.4(a)(10) and (a)(11), and the retailer

or person made a good-faith effort to comply with the sales and use tax laws. This subdivision expires for assessments

issued after July 1, 2020.

The assessment is for sales tax the taxpayer failed to collect or use tax the taxpayer failed to pay as a result of the change

in the definition of retailer or the sales tax base expansion to (i) service contracts, (ii) repair, maintenance, and installation

services, or (iii) sales transactions for a person in retail trade. The Secretary must determine that the taxpayer made a

good-faith effort to comply with the sales and use tax laws. This subdivision applies to assessments for any reporting period

beginning March 1, 2016, and ending December 31, 2022.

4) Has any period listed above been compromised with the Internal Revenue Service? _________ If yes, attach a

copy of the agreement.

5) Amount of Offer:

see page 2