Enlarge image

INSTRUCTIONS FOR PRELIMINARY INVENTORY

ON SIDE TWO OF APPLICATION FOR LETTERS OF ADMINISTRATION,

FORM AOC-E-202, Rev. 8/21

THE CLERK IS THE JUDGE OF PROBATE AND CANNOT PRACTICE LAW OR GIVE LEGAL ADVICE.

ACCORDINGLY, THE CLERK’S STAFF CANNOT HELP YOU FILL OUT THIS FORM. PARTS OF THIS FORM ARE

SELF-EXPLANATORY. HOWEVER, FOR ANY NECESSARY ASSISTANCE, YOU SHOULD CONSULT AN ATTORNEY.

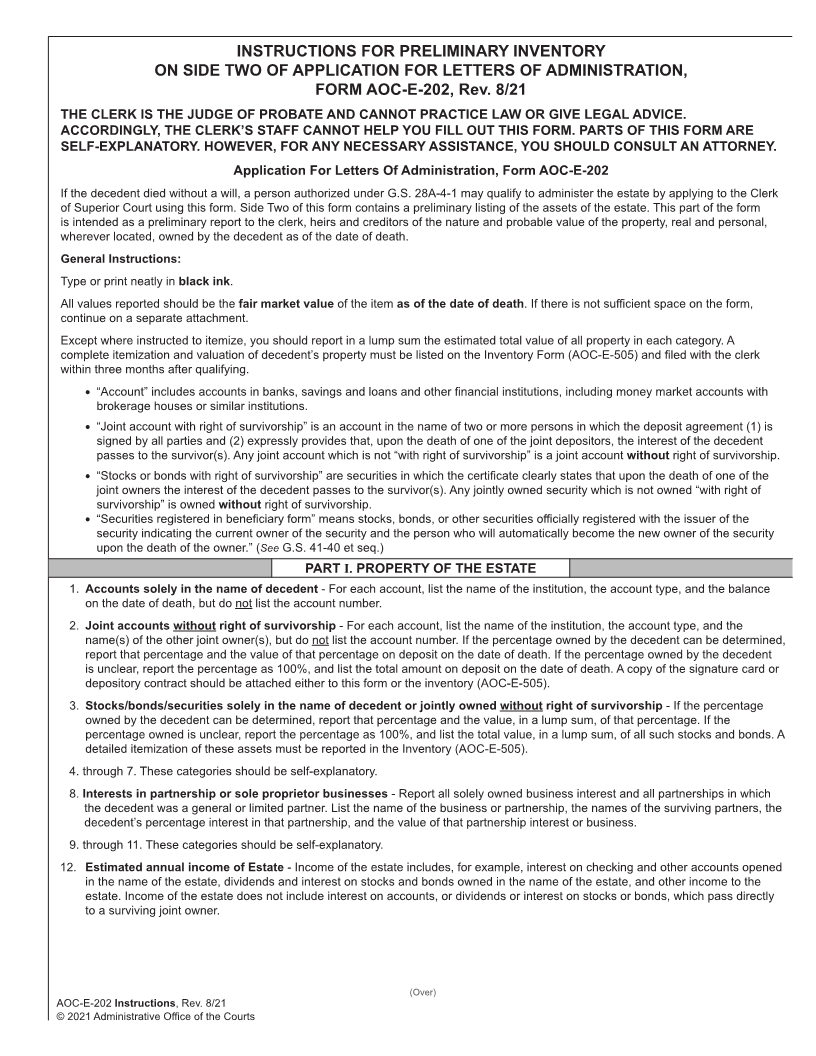

Application For Letters Of Administration, Form AOC-E-202

If the decedent died without a will, a person authorized under G.S. 28A-4-1 may qualify to administer the estate by applying to the Clerk

of Superior Court using this form. Side Two of this form contains a preliminary listing of the assets of the estate. This part of the form

is intended as a preliminary report to the clerk, heirs and creditors of the nature and probable value of the property, real and personal,

wherever located, owned by the decedent as of the date of death.

General Instructions:

Type or print neatly in black ink.

All values reported should be the fair market value of the item as of the date of death . If there is not sufficient space on the form,

continue on a separate attachment.

Except where instructed to itemize, you should report in a lump sum the estimated total value of all property in each category. A

complete itemization and valuation of decedent’s property must be listed on the Inventory Form (AOC-E-505) and filed with the clerk

within three months after qualifying.

• “Account” includes accounts in banks, savings and loans and other financial institutions, including money market accounts with

brokerage houses or similar institutions.

• “Joint account with right of survivorship” is an account in the name of two or more persons in which the deposit agreement (1) is

signed by all parties and (2) expressly provides that, upon the death of one of the joint depositors, the interest of the decedent

passes to the survivor(s). Any joint account which is not “with right of survivorship” is a joint account without right of survivorship.

• “Stocks or bonds with right of survivorship” are securities in which the certificate clearly states that upon the death of one of the

joint owners the interest of the decedent passes to the survivor(s). Any jointly owned security which is not owned “with right of

survivorship” is owned without right of survivorship.

• “Securities registered in beneficiary form” means stocks, bonds, or other securities officially registered with the issuer of the

security indicating the current owner of the security and the person who will automatically become the new owner of the security

upon the death of the owner.” (See G.S. 41-40 et seq.)

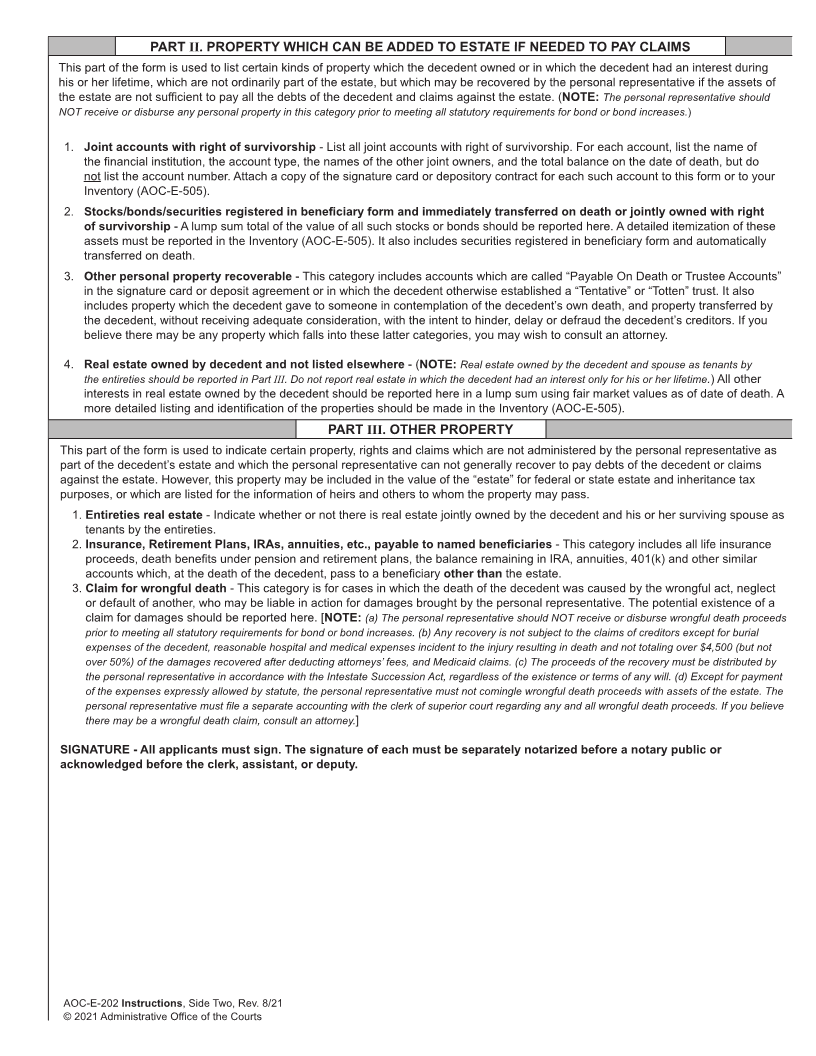

PART I.PROPERTY OF THE ESTATE

1. Accounts solely in the name of decedent - For each account, list the name of the institution, the account type, and the balance

on the date of death, but do not list the account number.

2. Joint accounts without right of survivorship - For each account, list the name of the institution, the account type, and the

name(s) of the other joint owner(s), but do not list the account number. If the percentage owned by the decedent can be determined,

report that percentage and the value of that percentage on deposit on the date of death. If the percentage owned by the decedent

is unclear, report the percentage as 100%, and list the total amount on deposit on the date of death. A copy of the signature card or

depository contract should be attached either to this form or the inventory (AOC-E-505).

3. Stocks/bonds/securities solely in the name of decedent or jointly owned without right of survivorship - If the percentage

owned by the decedent can be determined, report that percentage and the value, in a lump sum, of that percentage. If the

percentage owned is unclear, report the percentage as 100%, and list the total value, in a lump sum, of all such stocks and bonds. A

detailed itemization of these assets must be reported in the Inventory (AOC-E-505).

4. through 7. These categories should be self-explanatory.

8. Interests in partnership or sole proprietor businesses - Report all solely owned business interest and all partnerships in which

the decedent was a general or limited partner. List the name of the business or partnership, the names of the surviving partners, the

decedent’s percentage interest in that partnership, and the value of that partnership interest or business.

9. through 11. These categories should be self-explanatory.

12. Estimated annual income of Estate - Income of the estate includes, for example, interest on checking and other accounts opened

in the name of the estate, dividends and interest on stocks and bonds owned in the name of the estate, and other income to the

estate. Income of the estate does not include interest on accounts, or dividends or interest on stocks or bonds, which pass directly

to a surviving joint owner.

(Over)

AOC-E-202 Instructions, Rev. 8/21

© 2021 Administrative Office of the Courts