Enlarge image

IT-541i (1/24)

General Information and Instructions for

Completing Form IT-541 Fiduciary Income Tax Return

Who Must File a Return even if the decedent was domiciled in another state at the time

Louisiana Revised Statute (R.S.) 47:162 provides that every of death. Any trust instrument that does not specify as to which

resident estate or trust and every nonresident estate or trust state’s governing law prevails and that is administered in this state

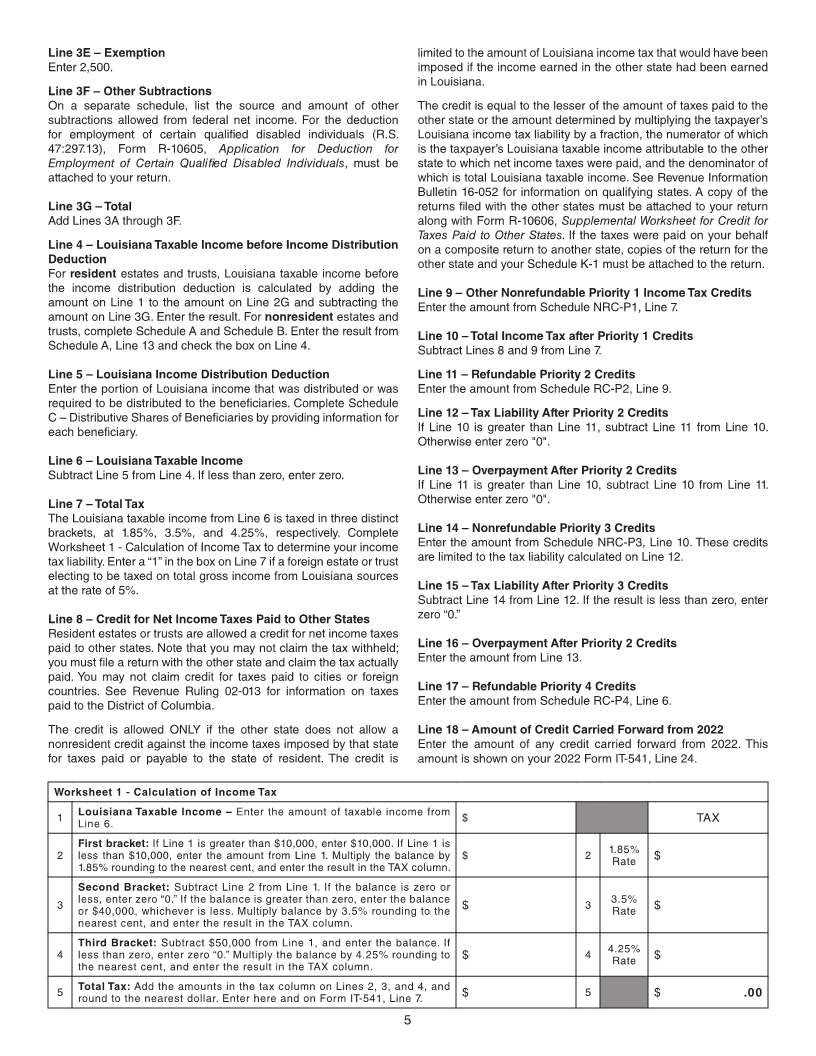

deriving income from Louisiana sources is liable for an income tax is considered a resident trust.

under the following guidelines:

Nonresident Bankruptcy Estate – A bankruptcy estate formed for

1. The net income of an estate or trust for the taxable year is a debtor for which a petition for relief has been filed and granted

$2,500 or more; under the Bankruptcy Code with any bankruptcy court not located

2. The gross income of an estate or trust for the taxable year is in Louisiana.

$6,000 or more, regardless of the amount of net income; Nonresident Estate – The estate of a decedent who was not

3. The beneficiary of an estate or trust is a nonresident of domiciled in Louisiana at the time of death.

Louisiana.

Nonresident Trust – Any trust that is not considered to be a resident

Grantor trusts, defined in R.S. 47:187 are also required to file a trust. If the trust instrument provides that the trust is governed by

return if any part of the net Louisiana income is taxable to the trust another state’s law, the trust is considered to be a nonresident trust

or to the nonresident beneficiaries of the grantor trust. even if the decedent was domiciled in Louisiana at the time of death.

Definitions Foreign Estates and Trusts Located Outside the United States

Bankruptcy Estate – An estate formed for a debtor for which a Foreign estates and trusts located outside the United States are

petition for relief has been filed and granted under chapter 7 or generally not required to file a United States fiduciary income

chapter 11 of title 11 of the United States Code (“Bankruptcy Code”). tax return. However, if the estate or trust derived income from

• If the debtor is an individual, the bankruptcy estate is treated Louisiana sources, the filing of a Louisiana fiduciary income tax

under federal law, and thus Louisiana, as a separate taxable return is required. The tax is imposed in the same manner as any

entity. other nonresident estate or trust. An alternate method of imposing

the tax provided under R.S. 47:300.3(3) allows estates and trusts

• A separate taxable entity is not created if a partnership or located outside the United States to elect to be taxed on total gross

corporation files a petition under any chapter of title 11 of the income from Louisiana sources at the rate of 5%. If this election is

U.S. Bankruptcy Code. being made, enter a "1" in the box on Line 7.

Fiduciary – Any person, firm, partnership, or association in whom Fiduciary Responsibility

a legal or ethical relationship of trust is established between two or As an entity in whom a relationship of trust is established to manage

more parties to manage and protect property or money. A fiduciary and protect property and money, the fiduciary is responsible for the

will have sufficient knowledge of the affairs of the trust or estate to preparation and filing of a true and correct return. R.S. 47:300.5

enable the preparation and filing of a true and correct return. provides that the fiduciary of an estate or trust is personally liable

Foreign Estate – Estates located outside the United States that for the payment of all taxes, penalties, and interest due by the

derive income from Louisiana sources but are not required to file estate or trust. The tax liability imposed on any beneficiary of the

United States fiduciary income tax returns. estate and trust is not the responsibility of the fiduciary.

Foreign Trust – Trusts located outside the United States that derive Income Taxed To Fiduciary

income from Louisiana sources but are not required to file United Under the provisions of R.S. 47:181 and R.S. 47:300.2, the income

States fiduciary income tax returns. tax imposed on an estate or trust for which a fiduciary will file

applies to the Louisiana taxable income of estates or of any kind of

Louisiana Taxable Income – R.S. 47:300.6 defines Louisiana property held in trust, including:

taxable income of a resident estate or trust as the amount of income

taxed in accordance with federal law for the same taxable year. 1. Income accumulated in trust for the benefit of unborn or

R. S. 47:300.7 defines Louisiana taxable income of a nonresident unascertained persons or persons with contingent interests,

estate or trust as the amount of income taxed in accordance with and income accumulated or held for future distribution under

federal law earned within or derived from sources within Louisiana the terms of the will or trust;

for the same taxable year. 2. Income that is to be distributed currently by the fiduciary to the

Resident Bankruptcy Estate – A bankruptcy estate formed for a beneficiaries and income collected by a guardian of a minor

debtor for which a petition for relief has been filed and granted under that is to be held or distributed as the court may direct;

the Bankruptcy Code with any bankruptcy court located in Louisiana. 3. Income received by the estates of deceased persons during

the period of administration or settlement of the estate; and,

Resident Estate – The estate of a decedent who was domiciled in

Louisiana at the time of death. 4. Income that, in the discretion of the fiduciary, may be either

distributed to the beneficiaries or accumulated.

Resident Trust – A trust or a portion of a trust created by the last

will and testament of a decedent domiciled in Louisiana at the time NOTE: Include all income from Electing Small Business Trusts

of death. If the trust instrument provides that the trust is governed (ESBTs) on this return. Also, there is no special tax calculation for

by Louisiana law, the trust is considered to be a resident trust this income and no need to file a separate return.

1