Enlarge image

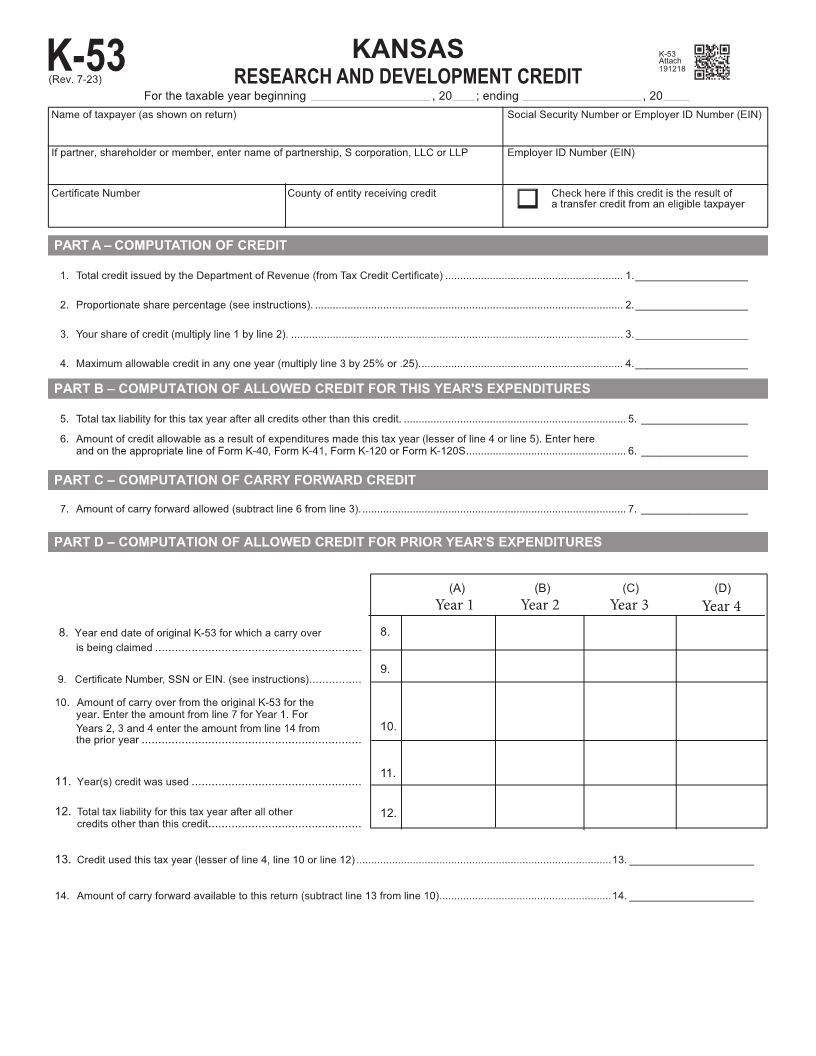

K-53

KANSAS Attach

191218

K-53(Rev. 7-23) RESEARCH AND DEVELOPMENT CREDIT

For the taxable year beginning ________________________________ , 20 ______ ; ending ________________________________ , 20 _______

Name of taxpayer (as shown on return) Social Security Number or Employer ID Number (EIN)

If partner, shareholder or member, enter name of partnership, S corporation, LLC or LLP Employer ID Number (EIN)

Certificate Number County of entity receiving credit Check here if this credit is the result of

o a transfer credit from an eligible taxpayer

PART A – COMPUTATION OF CREDIT

1. Total credit issued by the Department of Revenue (from Tax Credit Certificate) ............................................................ 1. ___________________

2. Proportionate share percentage (see instructions). ........................................................................................................ 2. ___________________

3. Your share of credit (multiply line 1 by line 2). ................................................................................................................ 3. ___________________

4. Maximum allowable credit in any one year (multiply line 3 by 25% or .25). .................................................................... 4. ___________________

PART B – COMPUTATION OF ALLOWED CREDIT FOR THIS YEAR'S EXPENDITURES

5. Total tax liability for this tax year after all credits other than this credit. ........................................................................... 5. __________________

6. Amount of credit allowable as a result of expenditures made this tax year (lesser of line 4 or line 5). Enter here

and on the appropriate line of Form K-40, Form K-41, Form K-120 or Form K-120S ...................................................... 6. __________________

PART C – COMPUTATION OF CARRY FORWARD CREDIT

7. Amount of carry forward allowed (subtract line 6 from line 3). ......................................................................................... 7. __________________

PART D – COMPUTATION OF ALLOWED CREDIT FOR PRIOR YEAR'S EXPENDITURES

(A) (B) (C) (D)

Year 1 Year 2 Year 3 Year 4

8. Year end date of original K-53 for which a carry over 8.

is being claimed ..............................................................

9.

9. Certificate Number, SSN or EIN. (see instructions)................

10. Amount of carry over from the original K-53 for the

year. Enter the amount from line 7 for Year 1. For

Years 2, 3 and 4 enter the amount from line 14 from 10.

the prior year ..................................................................

11.

11. Year(s) credit was used ...................................................

12. Total tax liability for this tax year after all other 12.

credits other than this credit ..............................................

13. Credit used this tax year (lesser of line 4, line 10 or line 12) ......................................................................................13. _____________________

14. Amount of carry forward available to this return (subtract line 13 from line 10) ..........................................................14. _____________________