Enlarge image

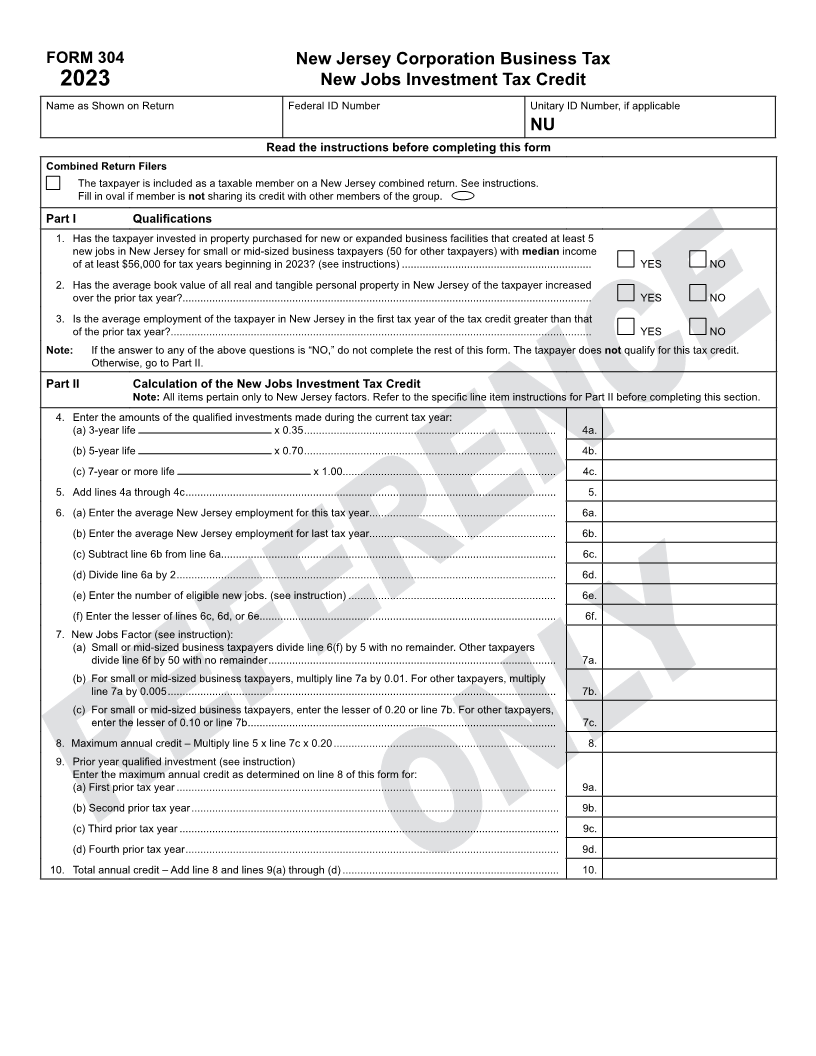

FORM 304 New Jersey Corporation Business Tax

2023 New Jobs Investment Tax Credit

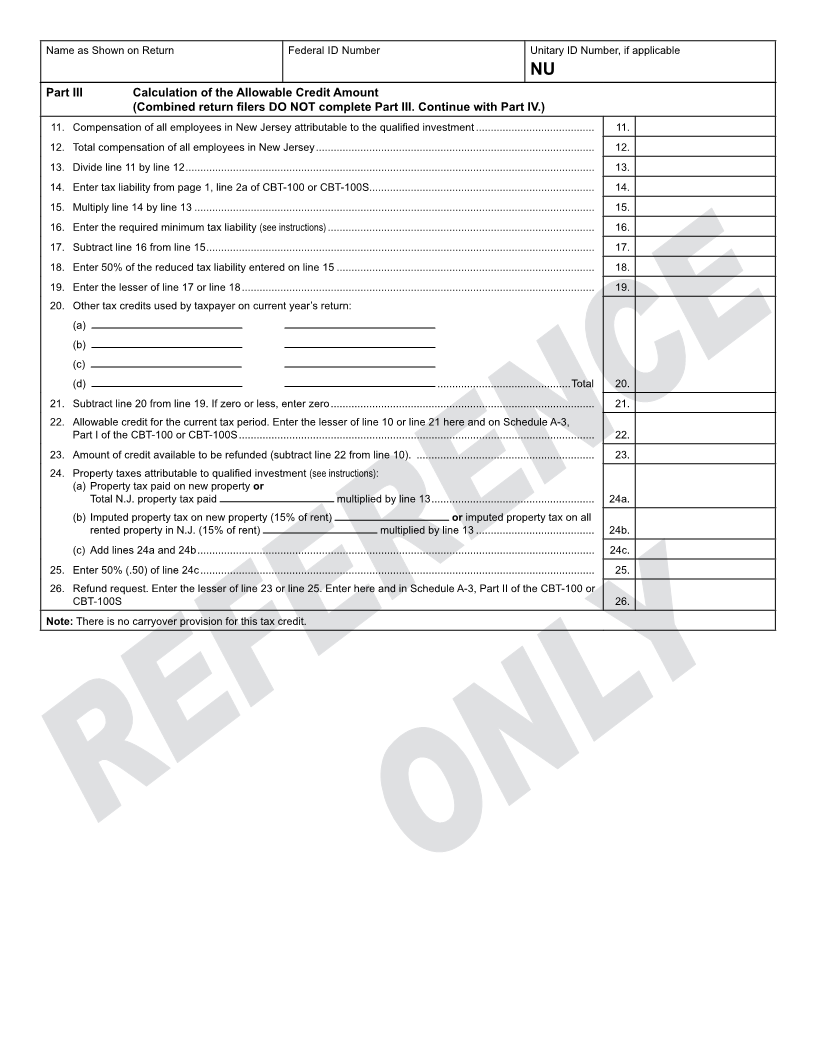

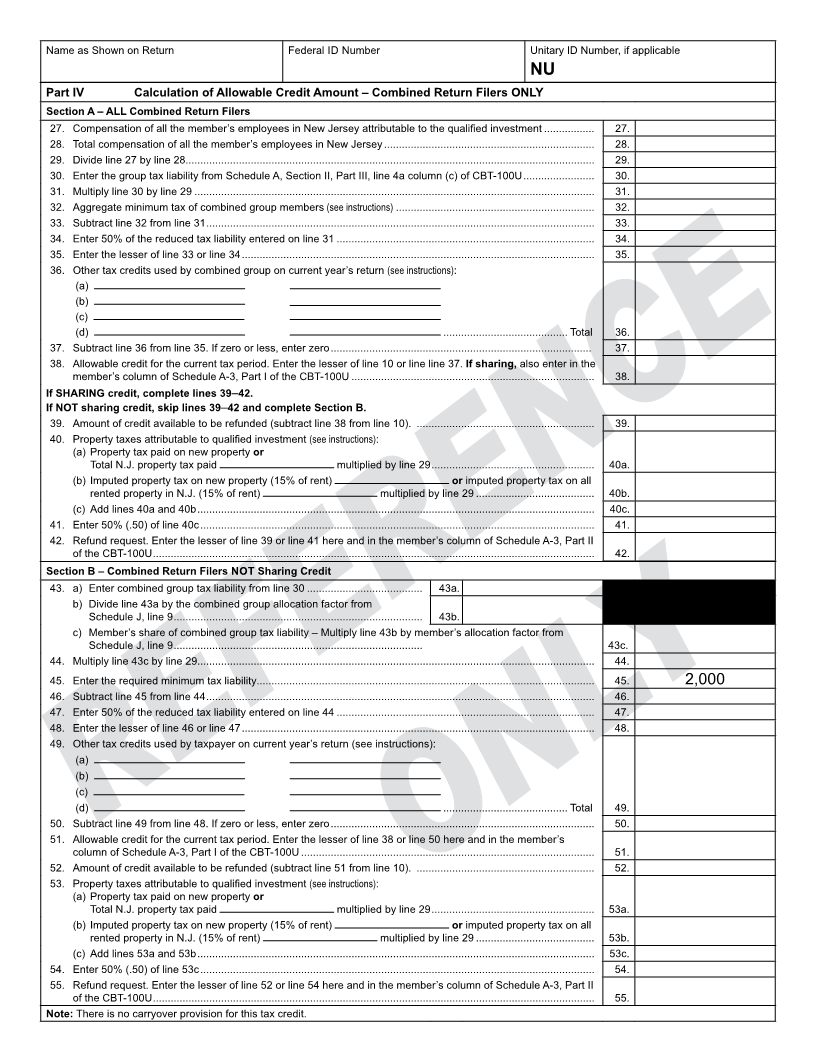

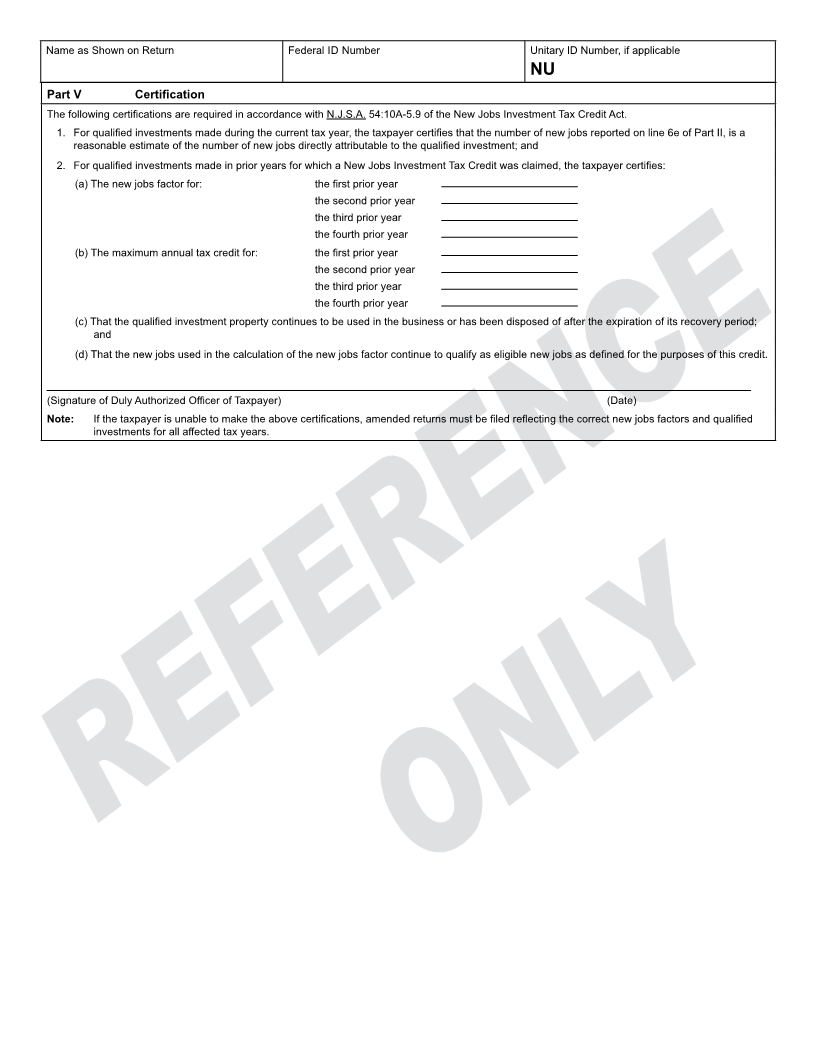

Name as Shown on Return Federal ID Number Unitary ID Number, if applicable

NU

Read the instructions before completing this form

Combined Return Filers

The taxpayer is included as a taxable member on a New Jersey combined return. See instructions.

Fill in oval if member is not sharing its credit with other members of the group.

Part I Qualifications

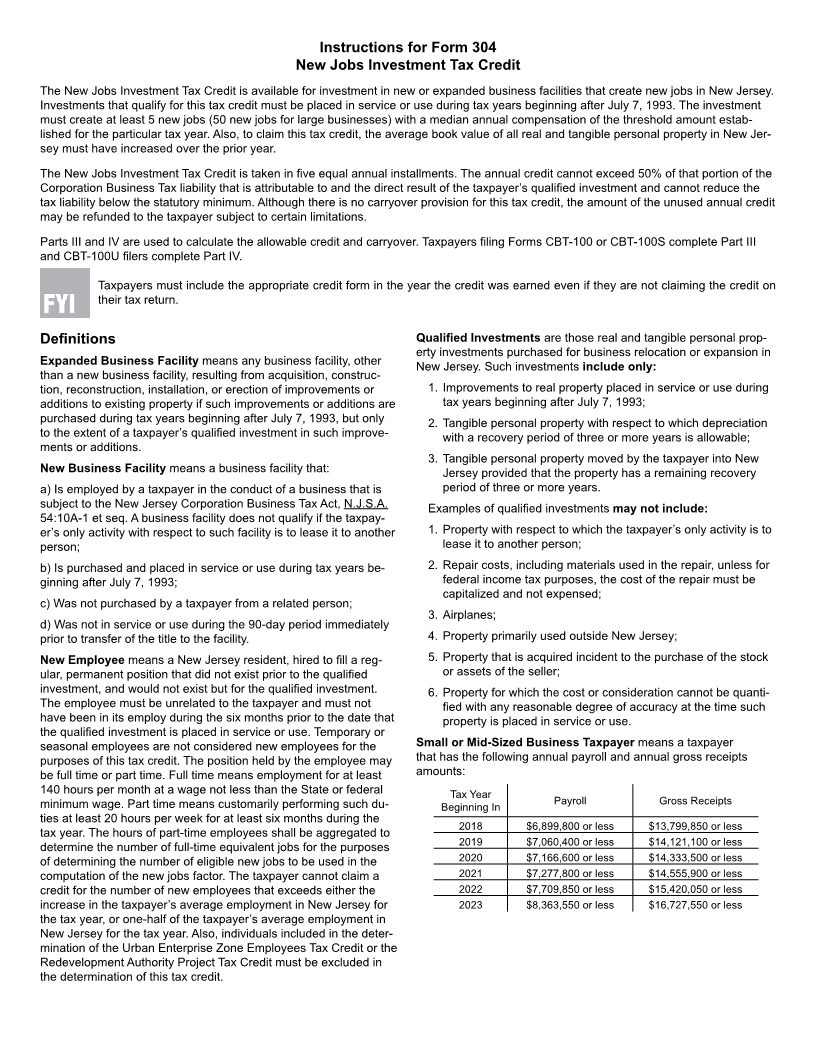

1. Has the taxpayer invested in property purchased for new or expanded business facilities that created at least 5

new jobs in New Jersey for small or mid-sized business taxpayers (50 for other taxpayers) with median income

of at least $56,000 for tax years beginning in 2023? (see instructions) ................................................................ YES NO

2. Has the average book value of all real and tangible personal property in New Jersey of the taxpayer increased

over the prior tax year?.......................................................................................................................................... YES NO

3. Is the average employment of the taxpayer in New Jersey in the first tax year of the tax credit greater than that

of the prior tax year?.............................................................................................................................................. YES NO

Note: If the answer to any of the above questions is “NO,” do not complete the rest of this form. The taxpayer does not qualify for this tax credit.

Otherwise, go to Part II.

Part II Calculation of the New Jobs Investment Tax Credit

Note: All items pertain only to New Jersey factors. Refer to the specific line item instructions for Part II before completing this section.

4. Enter the amounts of the qualified investments made during the current tax year:

(a) 3-year life x 0.35 ..................................................................................... 4a.

(b) 5-year life x 0.70 ..................................................................................... 4b.

(c) 7-year or more life x 1.00........................................................................ 4c.

5. Add lines 4a through 4c ............................................................................................................................. 5.

6. (a) Enter the average New Jersey employment for this tax year............................................................... 6a.

(b) Enter the average New Jersey employment for last tax year............................................................... 6b.

(c) Subtract line 6b from line 6a................................................................................................................. 6c.

(d) Divide line 6a by 2 ................................................................................................................................ 6d.

(e) Enter the number of eligible new jobs. (see instruction) ...................................................................... 6e.

(f) Enter the lesser of lines 6c, 6d, or 6e.................................................................................................... 6f.

7. New Jobs Factor (see instruction):

(a) Small or mid-sized business taxpayers divide line 6(f) by 5 with no remainder. Other taxpayers

divide line 6f by 50 with no remainder ................................................................................................. 7a.

(b) For small or mid-sized business taxpayers, multiply line 7a by 0.01. For other taxpayers, multiply

line 7a by 0.005 ................................................................................................................................... 7b.

(c) For small or mid-sized business taxpayers, enter the lesser of 0.20 or line 7b. For other taxpayers,

enter the lesser of 0.10 or line 7b ........................................................................................................ 7c.

8. Maximum annual credit – Multiply line 5 x line 7c x 0.20 ........................................................................... 8.

9. Prior year qualified investment (see instruction)

Enter the maximum annual credit as determined on line 8 of this form for:

(a) First prior tax year ................................................................................................................................ 9a.

(b) Second prior tax year ............................................................................................................................ 9b.

(c) Third prior tax year ................................................................................................................................ 9c.

(d) Fourth prior tax year .............................................................................................................................. 9d.

10. Total annual credit – Add line 8 and lines 9(a) through (d) ......................................................................... 10.