Enlarge image

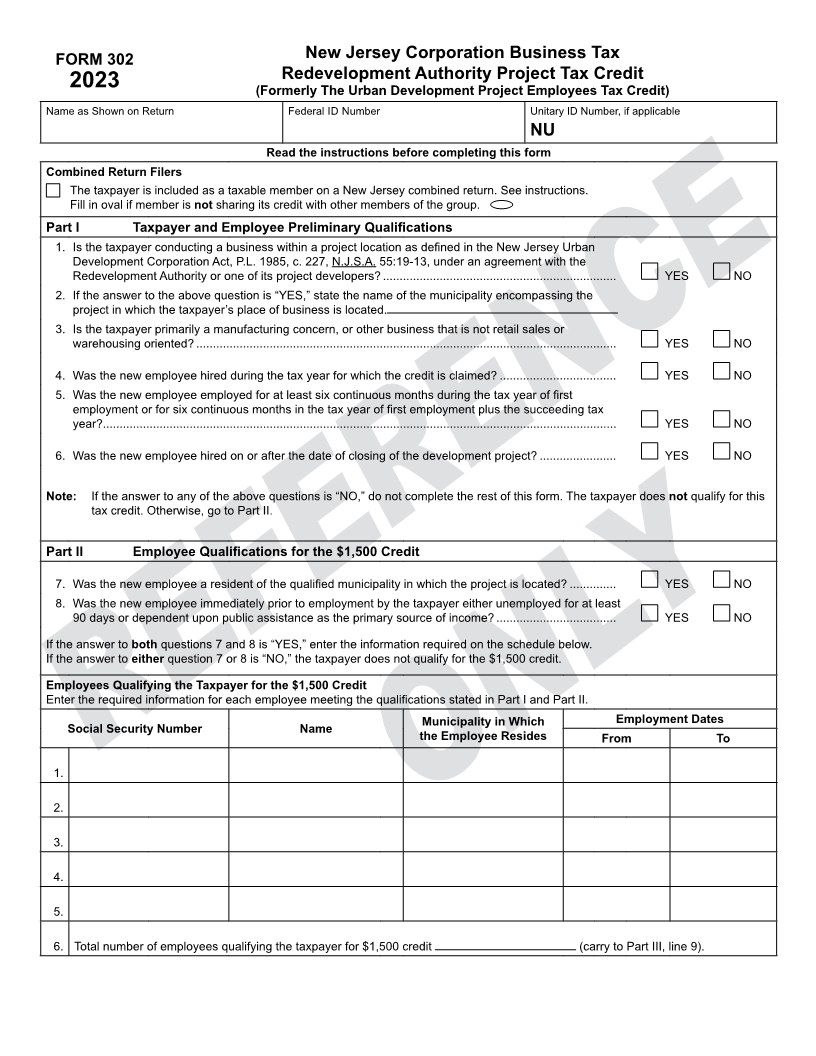

FORM 302 New Jersey Corporation Business Tax

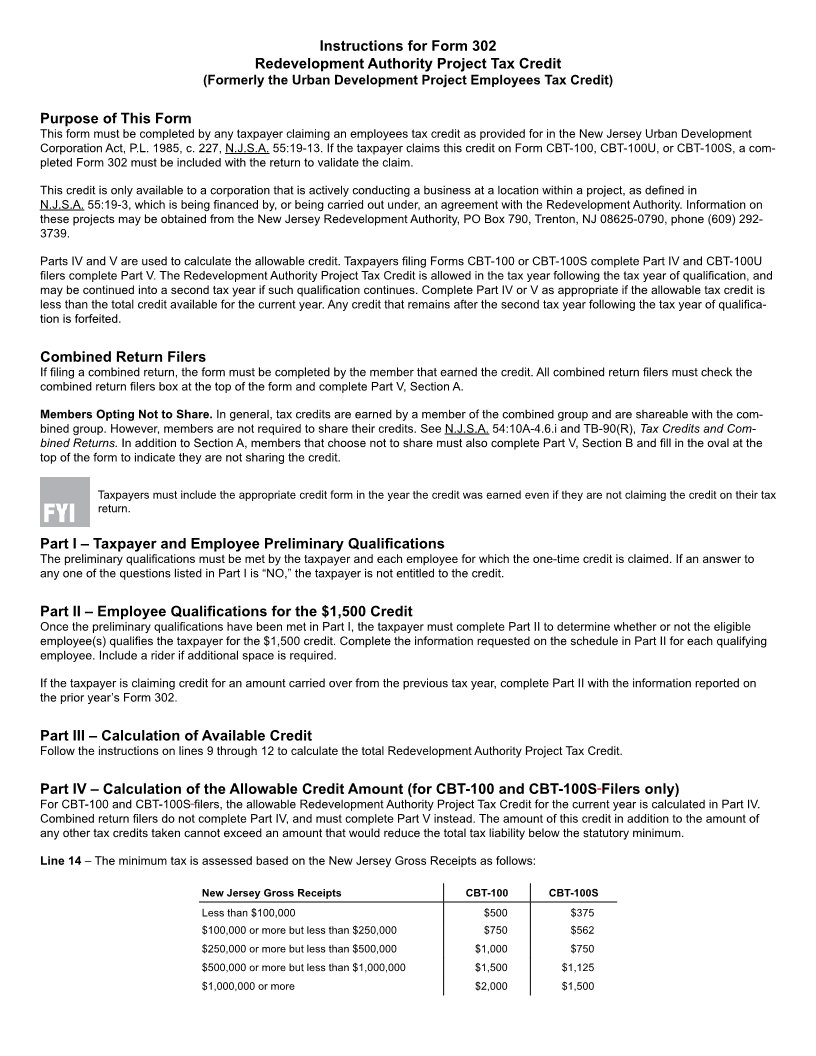

Redevelopment Authority Project Tax Credit

2023 (Formerly The Urban Development Project Employees Tax Credit)

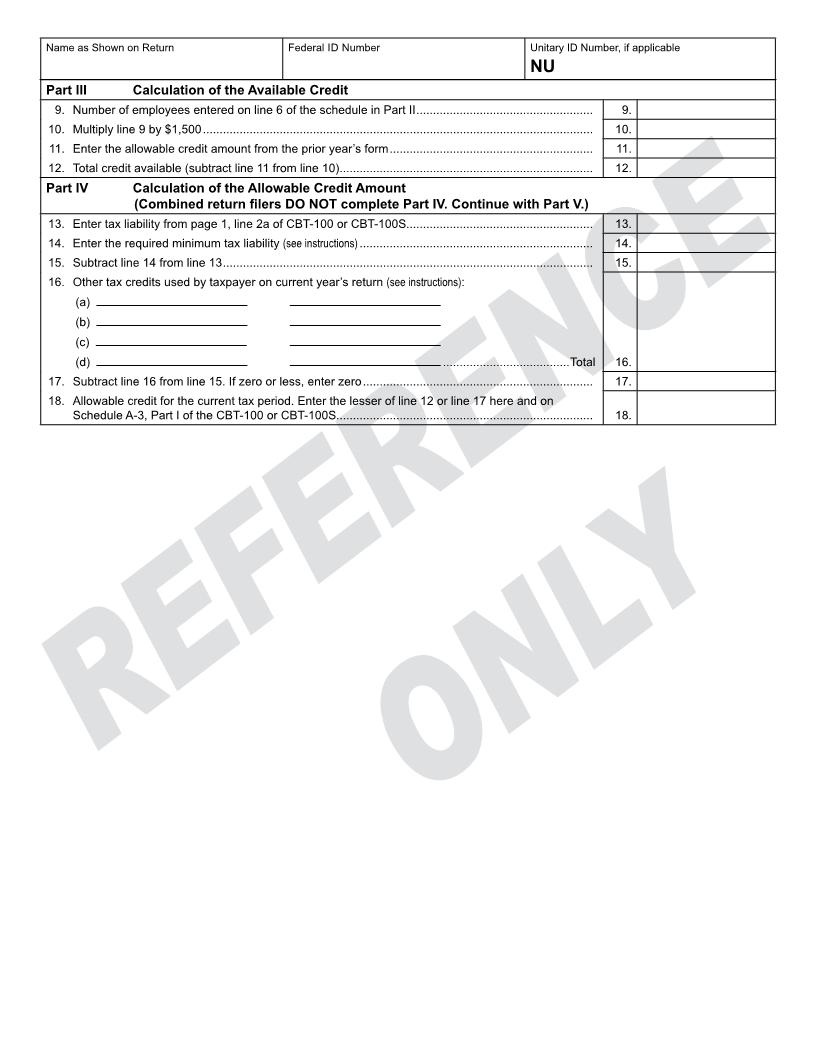

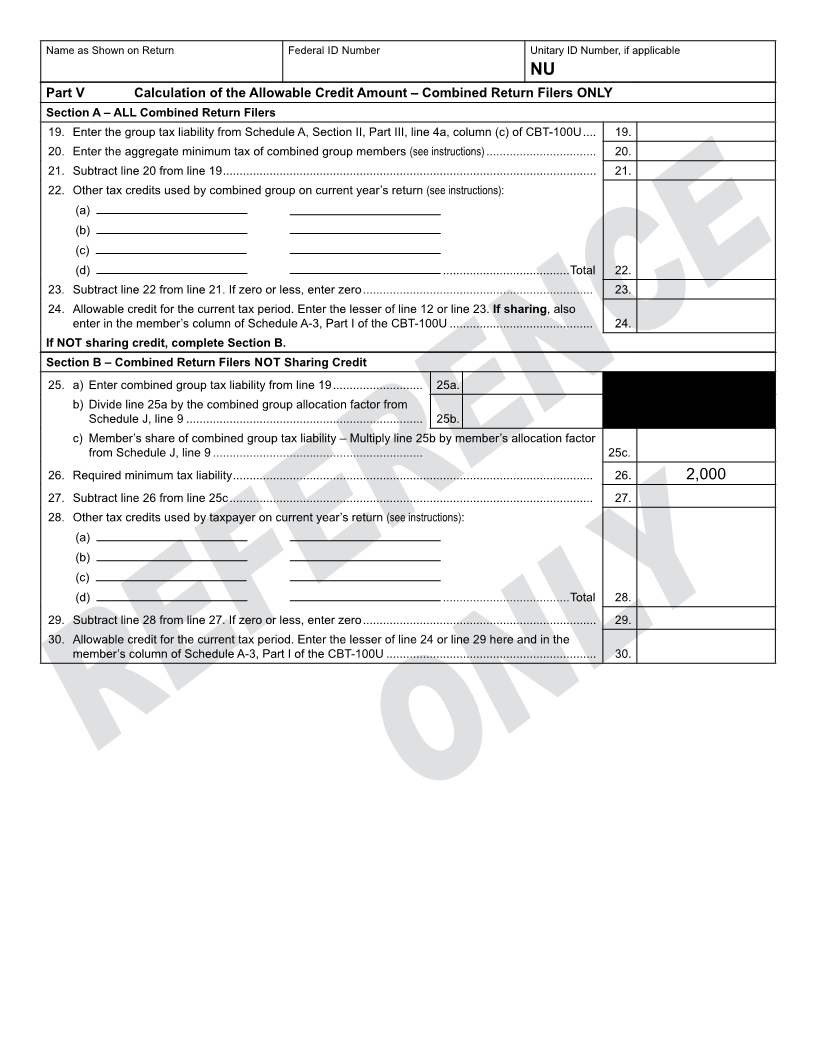

Name as Shown on Return Federal ID Number Unitary ID Number, if applicable

NU

Read the instructions before completing this form

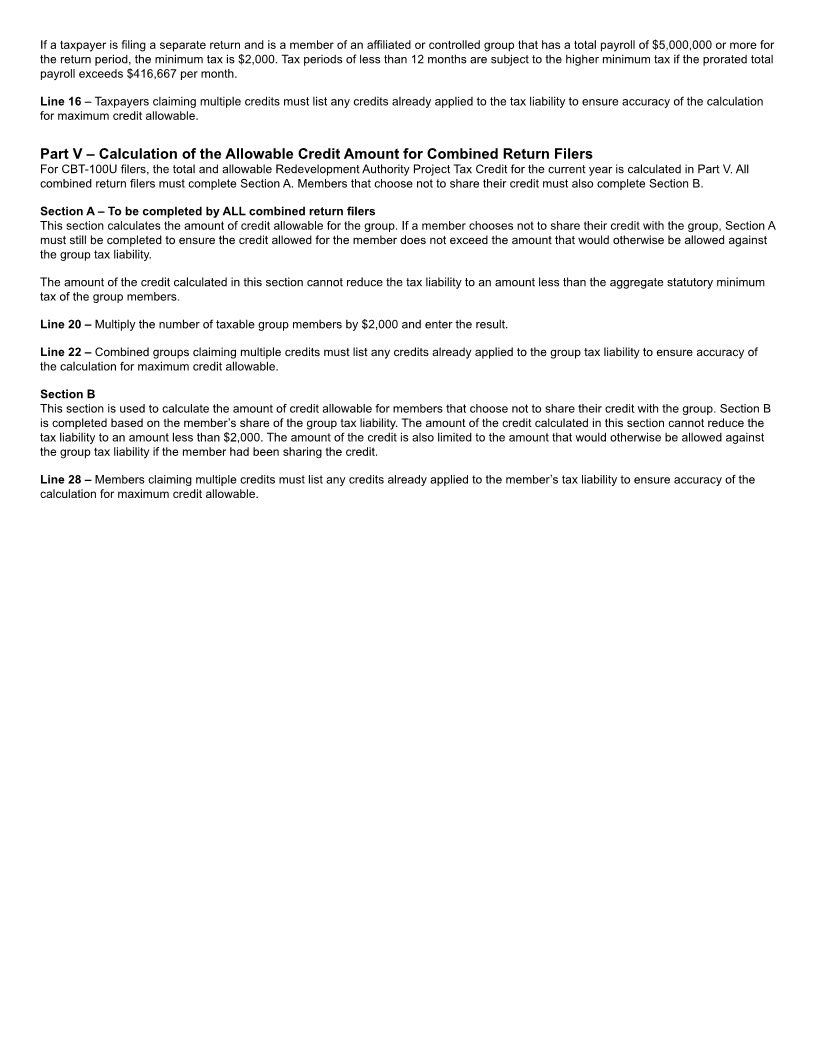

Combined Return Filers

The taxpayer is included as a taxable member on a New Jersey combined return. See instructions.

Fill in oval if member is not sharing its credit with other members of the group.

Part I Taxpayer and Employee Preliminary Qualifications

1. Is the taxpayer conducting a business within a project location as defined in the New Jersey Urban

Development Corporation Act, P.L. 1985, c. 227, N.J.S.A. 55:19-13, under an agreement with the

Redevelopment Authority or one of its project developers? ...................................................................... YES NO

2. If the answer to the above question is “YES,” state the name of the municipality encompassing the

project in which the taxpayer’s place of business is located.

3. Is the taxpayer primarily a manufacturing concern, or other business that is not retail sales or

warehousing oriented? .............................................................................................................................. YES NO

4. Was the new employee hired during the tax year for which the credit is claimed? ................................... YES NO

5. Was the new employee employed for at least six continuous months during the tax year of first

employment or for six continuous months in the tax year of first employment plus the succeeding tax

year?.......................................................................................................................................................... YES NO

6. Was the new employee hired on or after the date of closing of the development project? ....................... YES NO

Note: If the answer to any of the above questions is “NO,” do not complete the rest of this form. The taxpayer does not qualify for this

tax credit. Otherwise, go to Part II.

Part II Employee Qualifications for the $1,500 Credit

7. Was the new employee a resident of the qualified municipality in which the project is located? .............. YES NO

8. Was the new employee immediately prior to employment by the taxpayer either unemployed for at least

90 days or dependent upon public assistance as the primary source of income? .................................... YES NO

If the answer to both questions 7 and 8 is “YES,” enter the information required on the schedule below.

If the answer to either question 7 or 8 is “NO,” the taxpayer does not qualify for the $1,500 credit.

Employees Qualifying the Taxpayer for the $1,500 Credit

Enter the required information for each employee meeting the qualifications stated in Part I and Part II.

Municipality in Which Employment Dates

Social Security Number Name

the Employee Resides From To

1.

2.

3.

4.

5.

6. Total number of employees qualifying the taxpayer for $1,500 credit (carry to Part III, line 9).