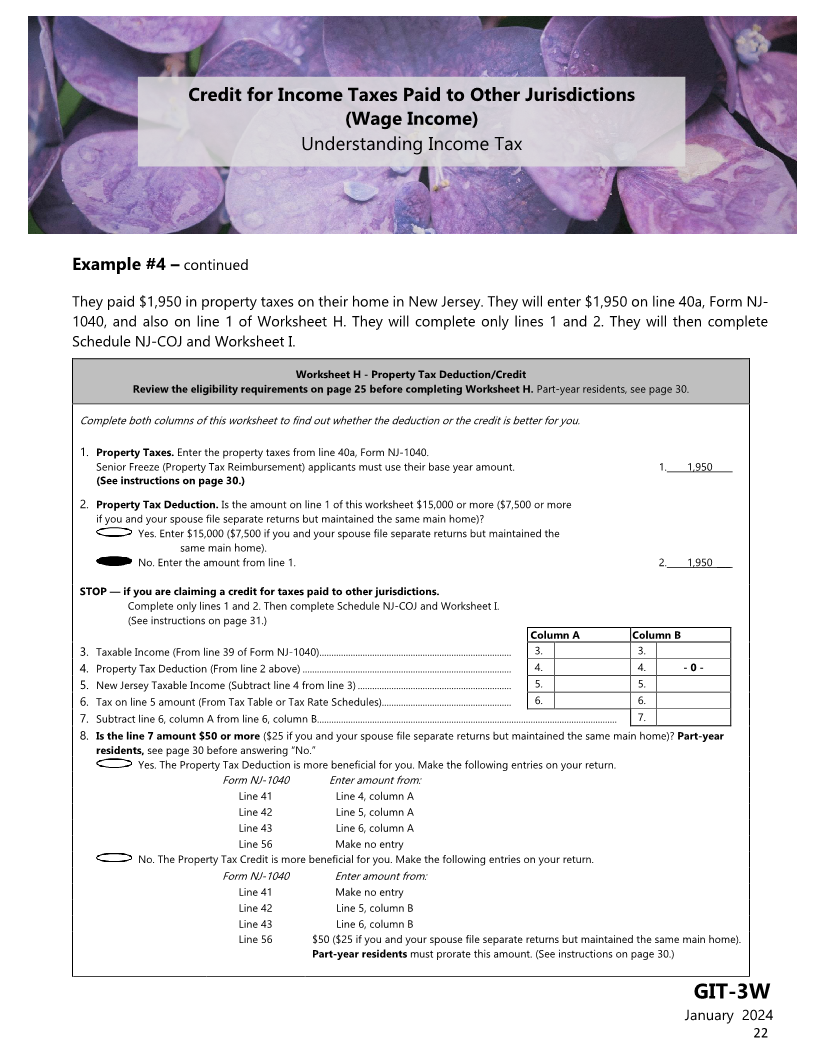

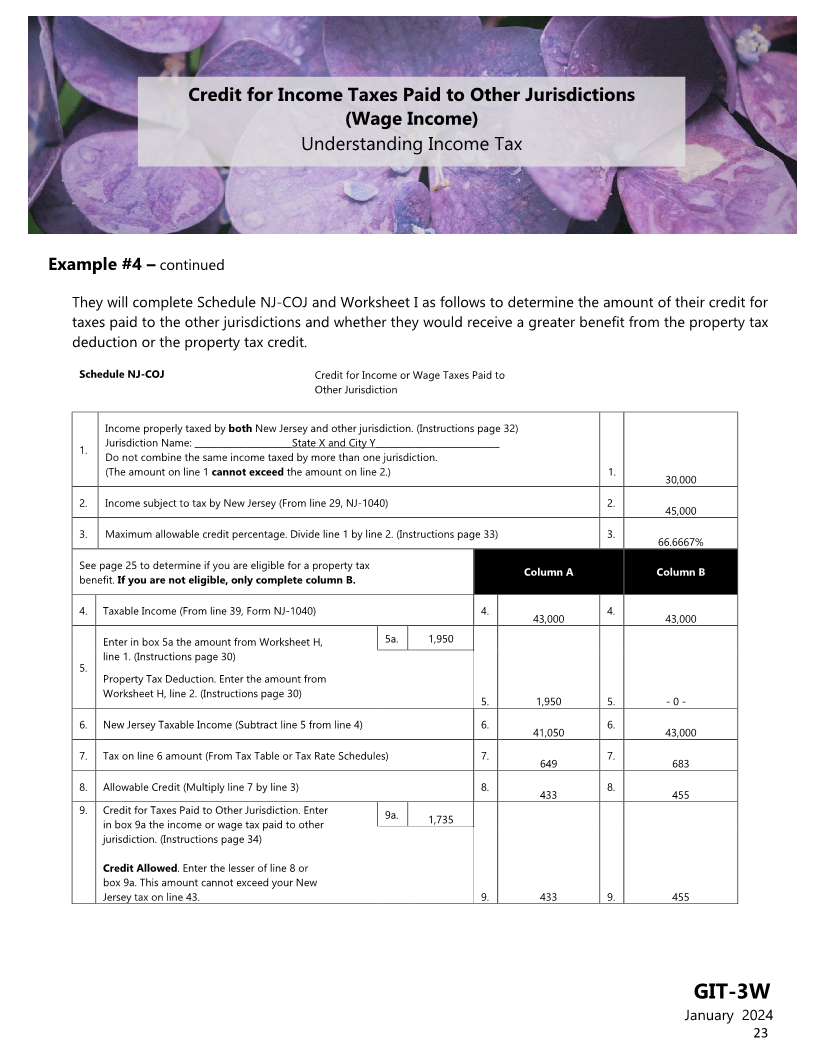

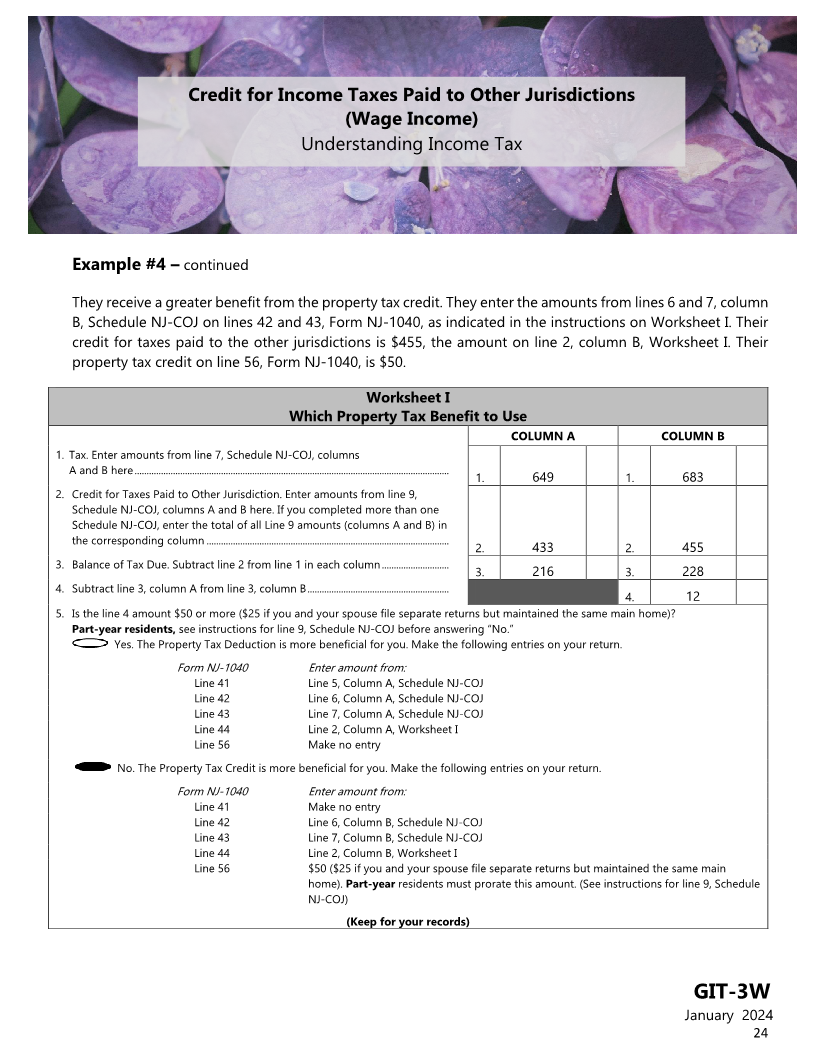

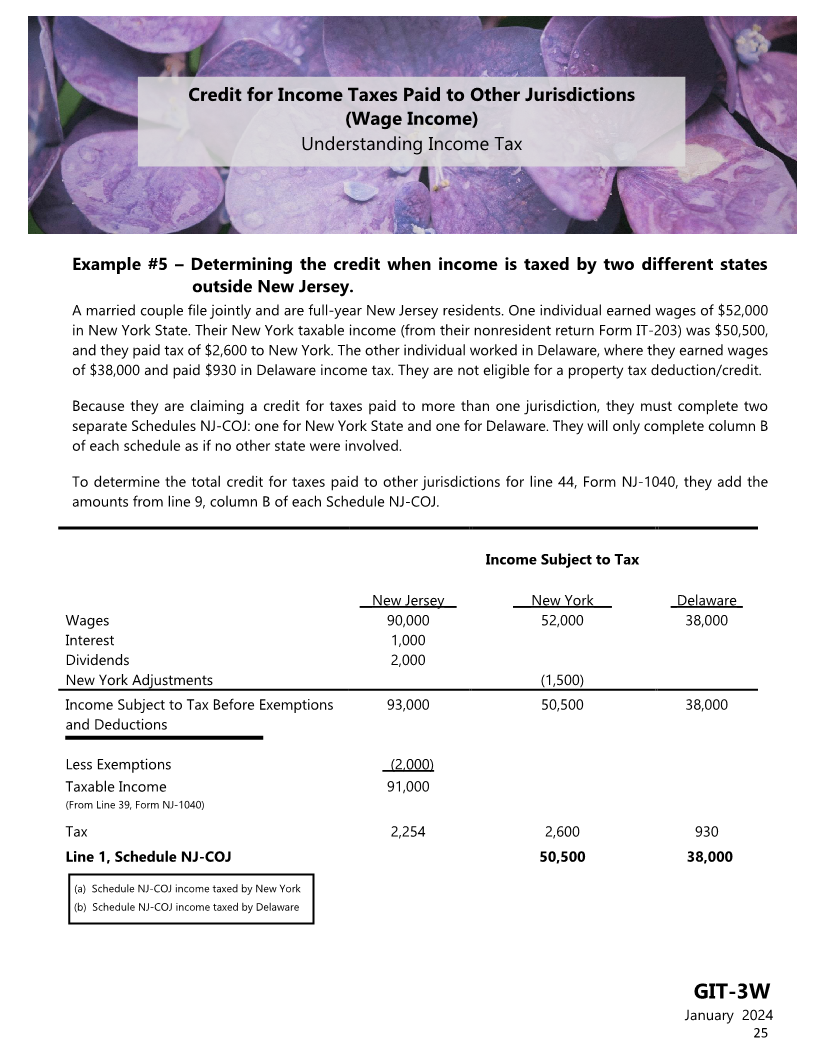

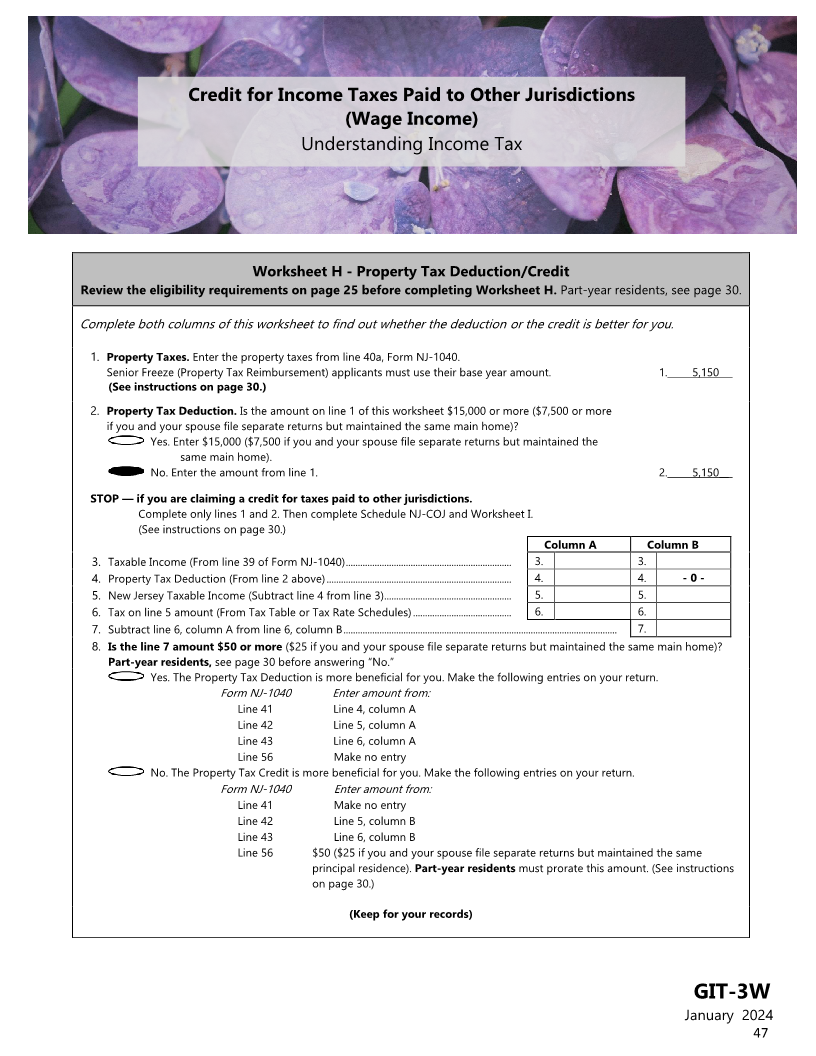

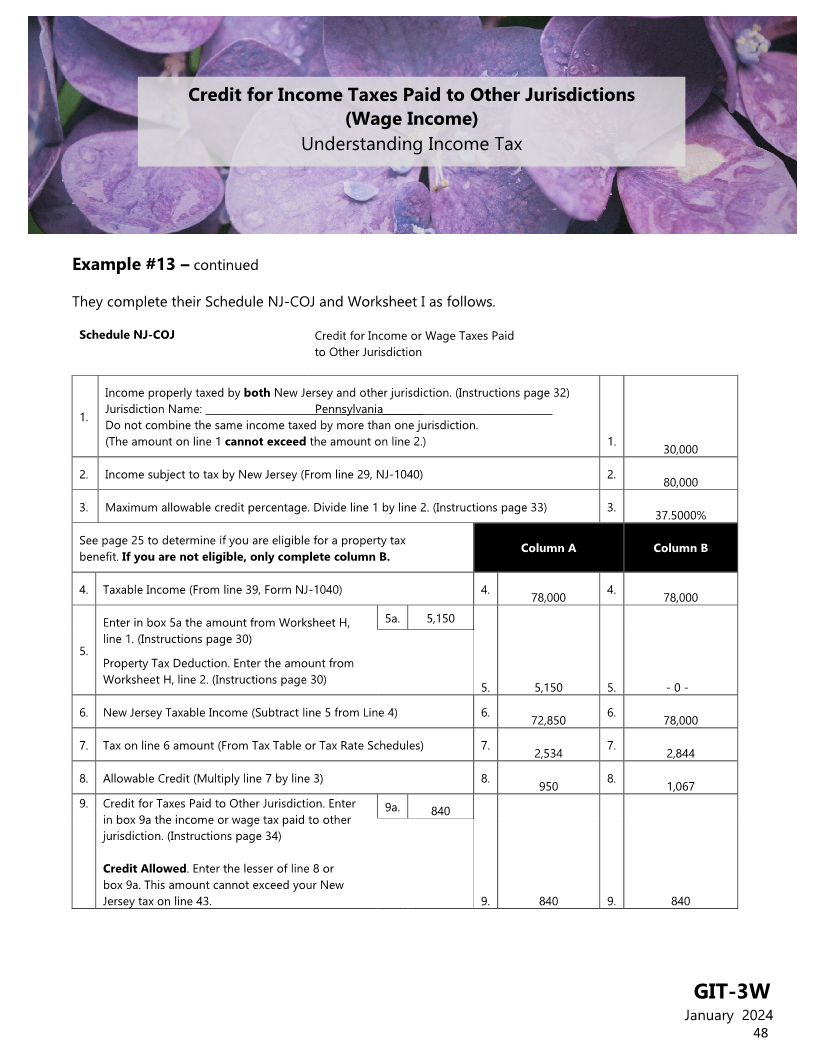

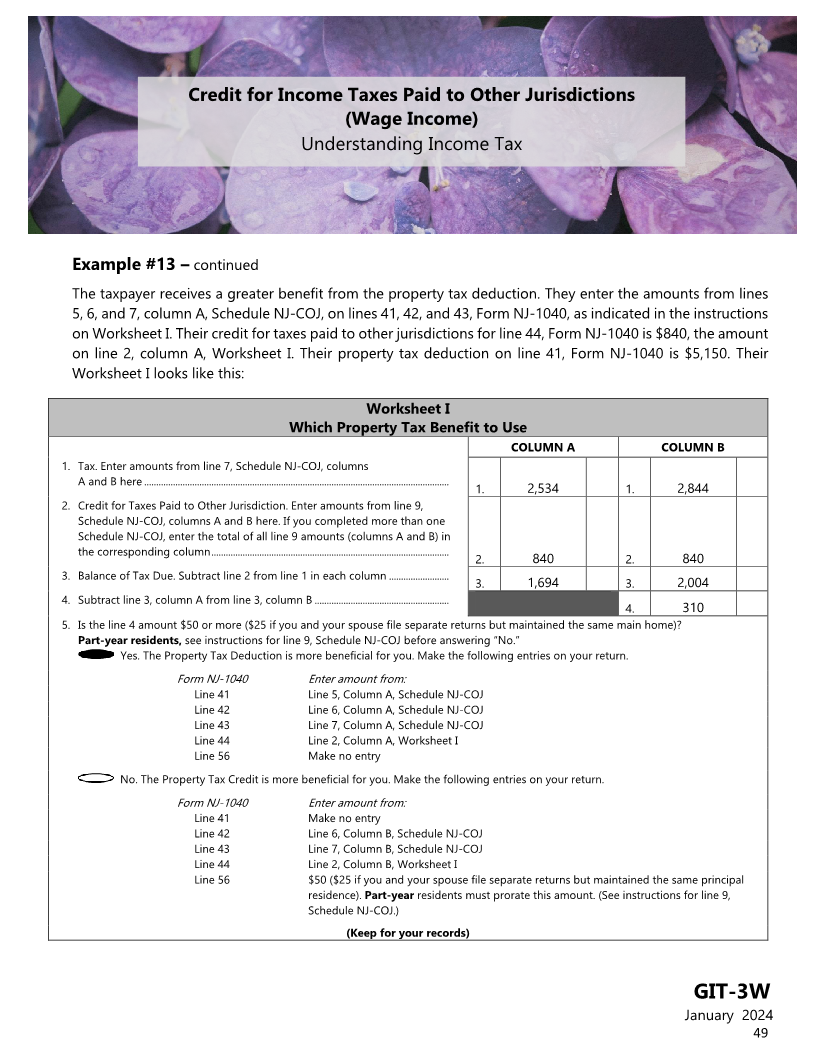

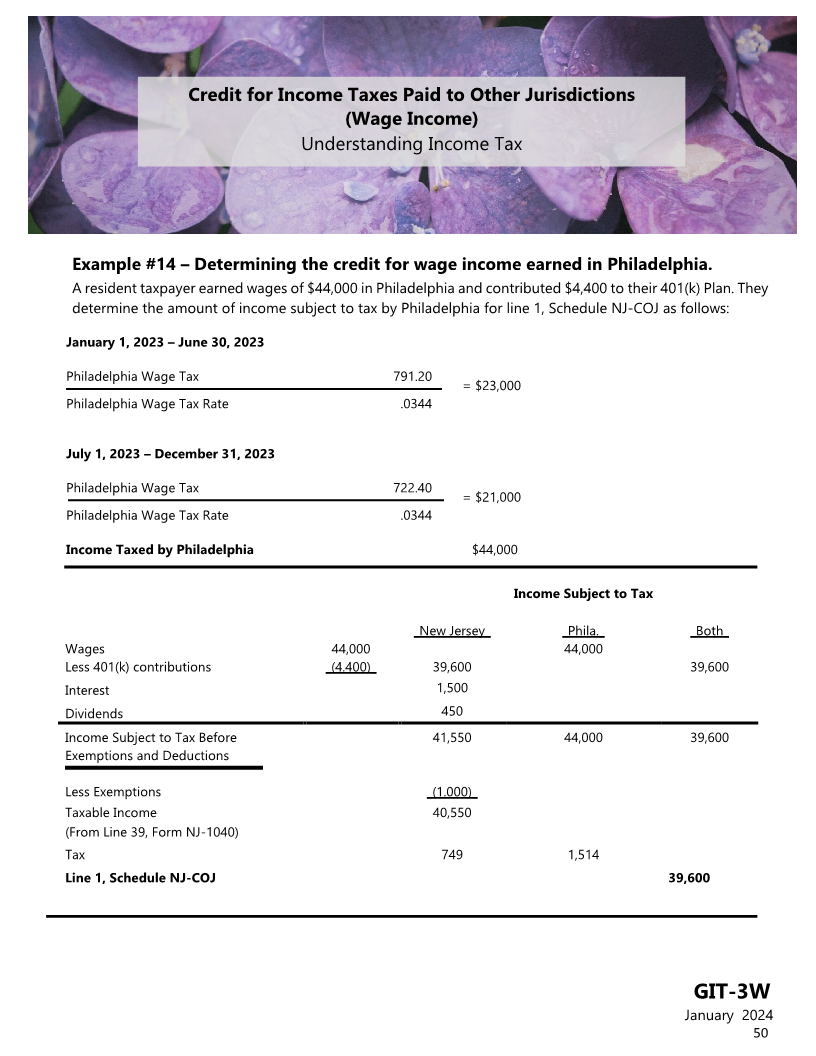

Enlarge image

Credit for Income Taxes Paid to Other

Jurisdictions (Wage Income)

Understanding Income Tax

New Jersey’s flower is the Meadow Violet.

Purpose of This Publication ................................................................................................................................. 3

Purpose of the Credit ............................................................................................................................................ 3

Components of the Credit Calculation ................................................................................................................ 3

Jurisdiction .................................................................................................................................................................................................. 4

Income Actually Taxed by Another Jurisdiction ............................................................................................................................ 4

Income Sourced to Another Jurisdiction v. “Worldwide Income” ..................................................................................... 4

Income Allocations Allowed by the Other Jurisdiction .......................................................................................................... 5

Adjustments (Deductions) Allowed by the Other Jurisdiction ............................................................................................ 5

Income Subject to Tax by More Than One Jurisdiction Within One State ..................................................................... 5

Income Properly Taxed by Another Jurisdiction ........................................................................................................................... 5

Income Properly Taxed ...................................................................................................................................................................... 5

Income Not Properly Taxed ............................................................................................................................................................. 6

Dual State Residents ........................................................................................................................................................................... 6

Income Actually Taxed by Both NJ and Another Jurisdiction .................................................................................................. 7

Income Taxable in Another Jurisdiction Exempt From Tax in NJ ....................................................................................... 7

Other Jurisdiction’s Additions to Income ................................................................................................................................... 7

Income Taxed by New Jersey ............................................................................................................................................................... 7

Actual Tax Paid to the Other Jurisdiction ........................................................................................................................................ 7

Actual Tax Paid on Income Taxed by More Than One Jurisdiction in a State Outside NJ ....................................... 7

How to Claim the Credit ....................................................................................................................................... 8

Proportional Credit Limitation Formula ............................................................................................................. 8

Completing More Than One Schedule NJ-COJ .................................................................................................. 8

GIT-3W

January 2024

1