- 2 -

Enlarge image

|

Instructions for Corporation Franchise Tax Initial Return

Act 12 of 2016 First Extraordinary Session extended the imposition of the franchise tax to additional types of entities, effective January 1, 2017. Those newly

taxable entities that were in existence and actually conducting business in Louisiana before January 1, 2017 should file their initial franchise tax return using

the Form CIFT-620, instead of this form. The franchise tax is imposed on corporations, and other entities that are tax as “C corporations” for federal income

tax purposes, subject to certain exceptions. Any limited liability company that is eligible to be treated as an “S corporation” for federal income tax purposes

on the first day of the franchise tax period, is not subject to franchise tax. Any other entity that was acquired during the period January 1, 2012 to Decem-

ber 31, 2013, by an entity that was taxed as an “S corporation,” is not subject to franchise tax. R.S. 47:608 provides certain exemptions from franchise tax.

Every new entity subject to franchise tax must file an initial return and pay the initial tax of $110.00. This return is due on or before the fifteenth day of the

third month following the month in which the tax accrues. For a domestic entity, the tax accrues on the date shown on the charter issued by the Secretary of

State. For a foreign entity, the tax accrues on the date the entity exercises its charter in Louisiana, is authorized to do, actually does business in Louisiana, or

uses any part of its capital or plant in Louisiana whether owned directly or indirectly by or through a partnership, joint venture, or any business organization

of which the domestic or foreign entity is a related party as defined in R. S. 47:605.1. Example due dates are as follows: The tax of ABC accrued on March

21, 2017; its initial return and payment of $110.00 tax would be due on or before June 15, 2017. If ABC adopted a calendar year accounting period, this initial

payment would cover the period March 21, 2013 through December 31, 2017. The next franchise return would be due on or before May 15, 2017, and must

be filed on Form CIFT-620. If the fiscal year ending June 30, 2017 was adopted, the initial return would cover the period from March 21, 2017 through June

30, 2017. The next franchise return would be due on or before November 15, 2017, and must be filed on Form CIFT-620. Delinquent returns and payments

must include applicable penalty and interest. If the due date falls on a holiday or weekend, the return must be transmitted on or before the next business

day in order to avoid penalty and interest.

Corporation franchise tax for domestic entities continues to accrue and must be filed on Form CIFT-620, regardless of whether any assets are owned or any

business operations are conducted, until a “Certificate of Dissolution” is issued by the Louisiana Secretary of State.

Corporation franchise tax for foreign entities continues to accrue and must be filed on Form CIFT-620, as long as the entities exercises its charter, does

business, or owns or uses any part of its capital or plant in Louisiana and, in the case of a qualified entities, until a “Certificate of Withdrawal” is issued by

the Louisiana Secretary of State.

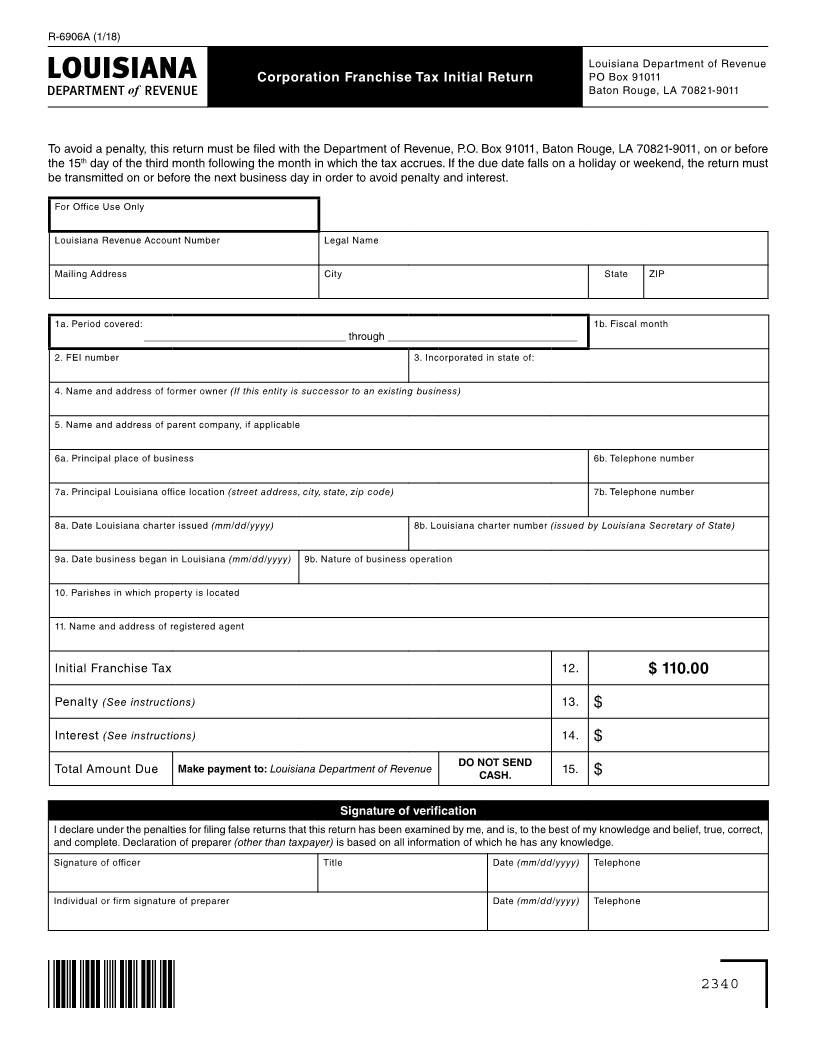

Line 1a. Enter the period covered by this initial franchise tax return. The period begins on the date the charter is filed with the Secretary of State, or

the date of Louisiana qualification, or other taxing incidence. The period ends on the date the first accounting period closes. If books are

kept on a calendar year basis, the period covered must end on the last day of December. If a fiscal year basis is used, the period must end

on the last day of any month and cannot exceed 12 months.

Line 1b. Enter the month your accounting period closes. The month should match the period ends date on Line 1a.

Line 2. Enter the Federal Employer’s Identification Number for the entity.

Line 3. Enter the state where the entity was originally incorporated.

Line 4. If the entity is the successor to an existing business (i.e., through a merger or the incorporation of an existing entity, such as a partnership),

enter the name and address of the former business or owner.

Line 5. If the entity is a subsidiary of another entity, enter the name and address of the parent entity.

Line 6a. Enter the city and state of the principal place of business. Enter the telephone number on line 6b.

Line 7a. Enter the primary Louisiana office location. Provide a physical address of the primary location: street address, city, state, and zip code.

Line 7b. Enter the telephone number.

Line 8a. Enter the date (month, day, year) the Louisiana charter was issued.

Line 8b. Enter the charter number assigned to this entity by the Louisiana Secretary of State.

Line 9a. Enter the date (month, day, year) this entity began business in Louisiana.

Line 9b. Describe the nature of the business operations in Louisiana.

Line 10. Enter the parishes in Louisiana where corporate property is located.

Line 11. Enter the name and address of the registered agent for this entity as recorded with the Louisiana Secretary of State.

Line 12. The initial franchise tax due is $110.00.

Line 13. Calculate Delinquent Filing Penalty for failure to file a return timely. The penalty for failure to file a return on time, except when failure is due

to a reasonable cause, is 5 percent of the tax for each 30 days or fraction thereof during which the failure to file continues.

Calculate Delinquent Payment Penalty for failure to pay the tax in full by the date the return is required by law to be filed. The penalty is 5

percent of the tax not paid for each 30 days, or fraction thereof, during which the failure to pay continues.

Add the amounts calculated for each penalty and print the total amount of penalties. The combined amount of delinquent filing and delin-

quent payment penalties cannot exceed 25 percent.

Line 14. Interest is due on all items of tax not paid by the due date of the return. Because the interest rate varies year to year, the Department is

unable to provide a specific rate. Refer to the Tax Rate Schedule (R-1111) for monthly interest rates that apply. Form R-1111 is available on

the LDR’s website at www.revenue.louisiana.gov. Calculate the interest amount and print the amount of interest here.

Line 15. Add the total penalty and interest due to the franchise tax amount of $110.00 and enter the total on Line 15. Make payment to the Louisiana

Department of Revenue. DO NOT SEND CASH.

The return must be signed by either the president, vice-president, treasurer, or another authorized officer, partner, or member. The telephone number of the

signer should be furnished. Any person, firm or corporation who prepares a taxpayer’s return other than the taxpayer, must sign the return as a representa-

tive of the firm or corporation preparing the return. This verification is not required if the return is prepared by a regular full-time employee of the taxpayer.

The telephone number of the preparer should also be furnished.

|