- 4 -

Enlarge image

|

R -10610i (1/20)

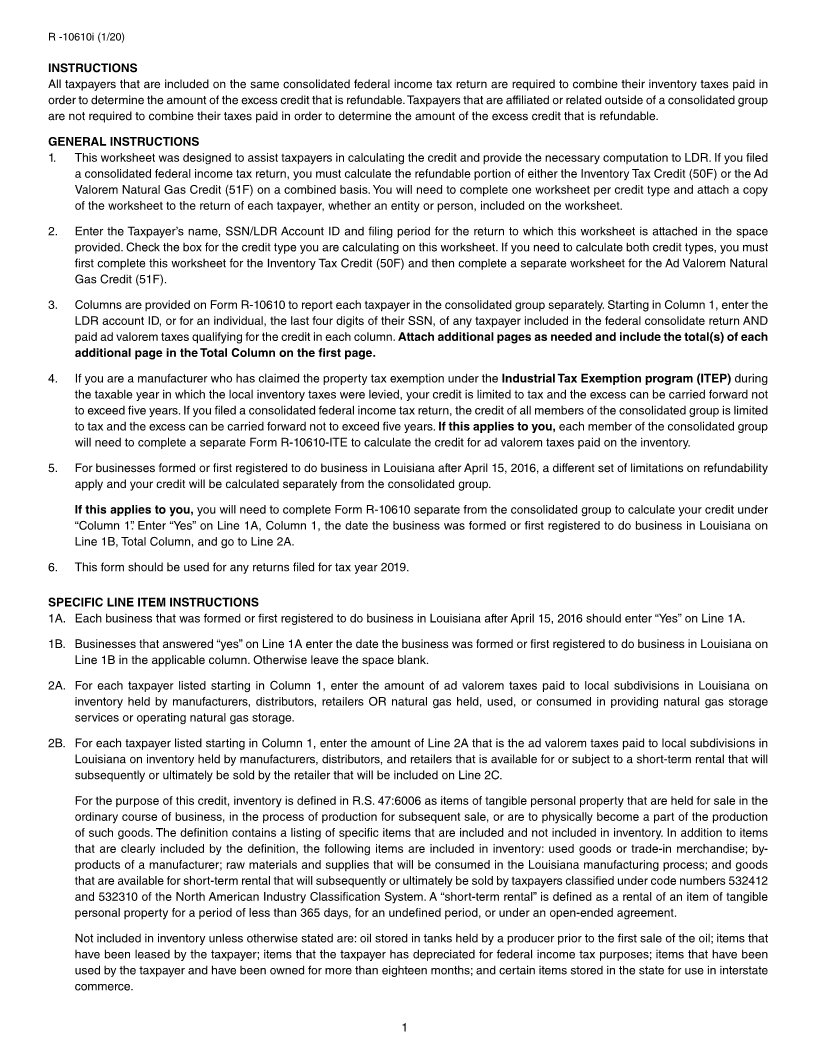

2C. For each taxpayer listed starting in Column 1, enter the amount of ad valorem taxes paid to local subdivisions in Louisiana on

inventory held by manufacturers, distributors, retailers OR natural gas held, used, or consumed in providing natural gas storage

services or operating natural gas storage reported on Line 2A that meets the definition of inventory under R.S. 47:6006. Enter the

total of all columns in the “Total Column”.

3. If the amount on Line 2C, Total Column, is greater than $500,000, go to Line 4.

If the amount on Line 2C, Total Column, is less than or equal to $500,000, your entire credit (Line 2C) will be used to offset tax and

any excess will be refunded. For each taxpayer listed, enter the amount from Line 2C of their column on Schedule I (Individual) or

Schedule RC-P4 (Business) with the identifying three-digit code.

Special instructions for any taxpayer listed with “Yes” on Line 1:

If Line 2C is less than $10,000, your credit (Line 2C) will be used to offset tax and any excess will be refunded. Enter the amount

from Line 2C on Schedule I or Schedule RC-P4 with the identifying three-digit code. However, the taxpayer must be included in the

remaining calculations to determine the refundability for the group.

If Line 2C is equal to or greater than $10,000 but less than $500,000, your credit (Line 2C) will be used to offset tax and 75 percent

of the excess will be refunded. Complete the rest of the worksheet using just the column for this taxpayer and the “Total Column”. The

other columns will be blank for Lines 4 through 7, 11 and 12.

Stop here; you are finished with the worksheet.

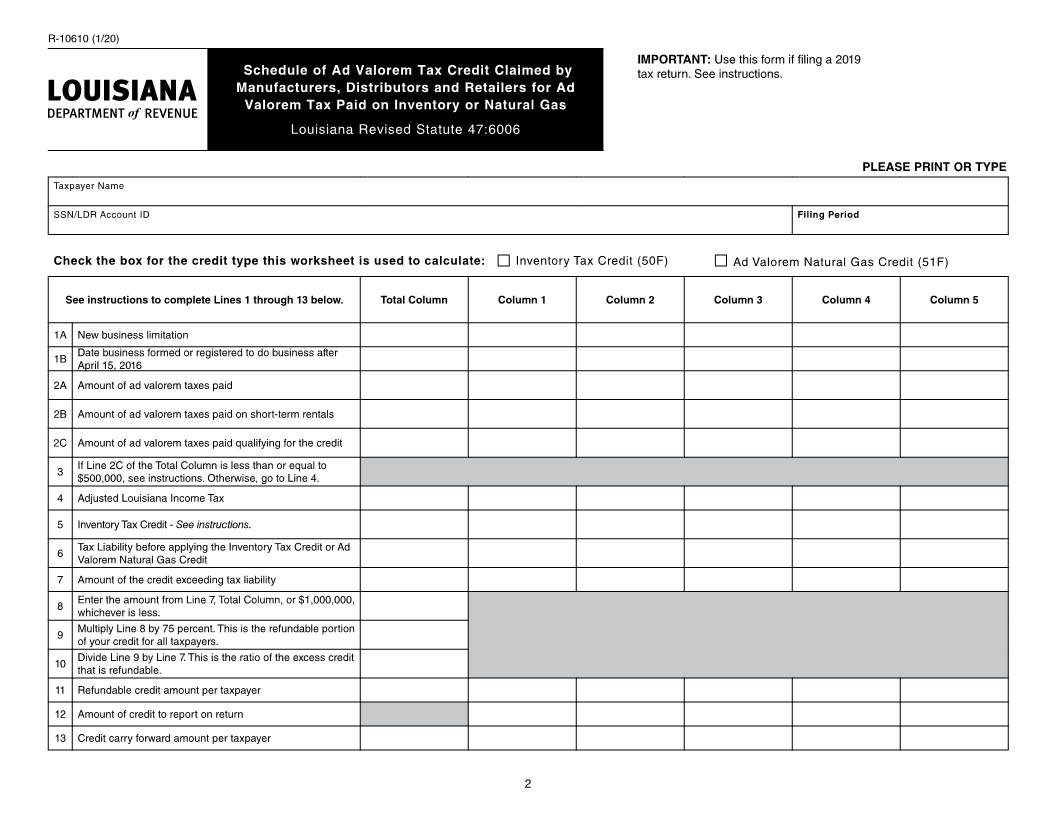

4. For each taxpayer listed starting in Column 1, enter the amount of your adjusted tax liability from your tax return. See chart below for

line numbers. Enter the total of all columns in the “Total Column”.

Tax Year IT-540 IT-540B IT-540BNRA IT-541 R-6922 CIFT-620

2019 Line 23 Line 22 Line 21 Line 19 Line 11 Line 16

5. Complete this line only if both credits are claimed and after calculating the Inventory Tax Credit. For each taxpayer listed starting in

Column 1, enter the Inventory Tax Credit amount claimed on Schedule I or Schedule RC-P4. Enter the total of all columns in the “Total

Column”.

6. Tax Liability before applying the Inventory Tax Credit or Ad Valorem Natural Gas Credit. For each taxpayer listed starting in Column

1, subtract Line 5 from Line 4. If less than zero, enter zero. Enter the total of all columns in the “Total Column”.

7. Amount of the credit exceeding tax liability. For each taxpayer listed starting in Column 1, subtract Line 6 from Line 2C. If less than

zero, enter zero. Enter the total of all columns in the “Total Column”.

If Line 7, Total Column, is equal to zero, your entire credit on Line 2C will be used to offset tax. For each taxpayer listed starting in

Column 1, enter the amount from Line 2C on Schedule I or Schedule RC-P4 with the identifying three-digit code. Stop here; you are

finished with the worksheet.

8. In the Total Column, enter the amount from Line 7, Total Column, or $1,000,000, whichever is less.

9. Multiply Line 8, Total Column, by 75 percent, round to the nearest dollar, and enter the result in the Total Column. This is the

refundable portion of your credit for all taxpayers.

10. Divide Line 9, Total Column, by Line 7, Total Column, round to six places after the decimal, and enter the ratio in the Total Column.

This is the ratio of the excess credit that is refundable.

11. For each taxpayer listed starting in Column 1, multiply Line 7 by the ratio on Line 10, Total Column, and round to the nearest dollar.

Enter the total of all columns in the “Total Column”. This amount should equal the amount on Line 9, Total Column, except for minor

rounding differences.

12. For each taxpayer listed starting in Column 1, if Line 7 is greater than zero, add Lines 6 and 11. Otherwise, enter the amount from

Line 2C. For each taxpayer, enter the amount from Line 12 on Schedule I or Schedule RC-P4 with the identifying three-digit code.

13. For each taxpayer listed starting in Column 1, subtract Line 11 from Line 7. Enter the total of all columns in the “Total Column”. This

amount is your credit carry forward. This amount should be reported on next year’s return, on Schedule J (Individual) or Schedule

NRC-P3 (Business) with the identifying three-digit code listed below.

Inventory Tax Credit Carried Forward 218

Ad Valorem Natural Gas Credit Carried Forward 219

2

|