Enlarge image

R-1029i (7/19)

Sales Tax Return - General Instructions

1. Who Should File: All persons and dealers who are 3. FEIN Numbers : LDR is now requiring a federal paid preparer represents a firm, the firm’s FEIN must be

subject to the tax levied under Chapter 2 of Subtitle II employer identification number for all sales tax accounts. entered in the “Paid Preparer Use Only” box. The failure

of Title 47 of the Louisiana Revised Statutes of 1950, Please enter this information at the bottom of the return. of a paid preparer to sign or provide an identification

as amended, are required to file a tax return monthly or 4.Amended/Final Return: If this is an amended return, number will result in the assessment of the unidentified

quarterly. Returns are due on or before the 20th day of place an “X” in the box labeled “Amended Return” at the preparer penalty on the preparer. The penalty is $50 for

each month for the preceding calendar month or quarter. bottom of the return. If this is a final return, place an “X” each occurrence of failing to sign or failing to provide an

If the due date falls on a weekend or holiday, the return in the box labeled “Final Return” at the bottom of the identification number.

is due the next business day and becomes delinquent the return and enter the date the business was sold or closed 7. Before Mailing: Care should be exercised to ensure

next day thereafter. in the space provided. that: (a) the correct period is entered or shown in the

2.U.S. NAICS Code : Louisiana Department of Revenue 5. Dollar Amounts: All amounts on the return should appropriate area near the upper left-hand corner of the

(LDR) is assigning business codes to sales tax accounts based be rounded to the nearest dollar and handprinted in the return; (b) the handprinted numerals in the boxes are

upon the North American Industry Classification System appropriate boxes. clear and legible; (c) the return is signed and dated by

(NAICS). If your Louisiana Revenue tax account currently the appropriate company official; (d) a payment for the

does not have a NAICS code assigned to it, please include 6. Paid Preparer: If your return was prepared by a paid exact amount of tax, penalty, and interest accompanies the

this information on your sales tax return. NAICS codes may preparer, that person must also sign in the appropriate return and that this payment amount is properly entered

be found on your federal corporate income tax return or on space, complete the information in the “Paid Preparer on Line 16 of the form; (e) if payment is made electroni-

your Louisiana Workforce Commission account. NAICS Use Only” box and enter his or her identification number cally, mark the box on Line 16; and (f) the return and pay-

codes may also be found on the U.S. Census Bureau’s web- in the space provided under the box. If the paid preparer ment are placed in the provided pre-addressed envelope,

page at www.census.gov. has a PTIN, the PTIN must be provided; otherwise, the stamped, and mailed.

FEIN or LDR account number must be provided. If the

Sales Tax Return - Specific Instructions for Filing Periods Beginning July 2019

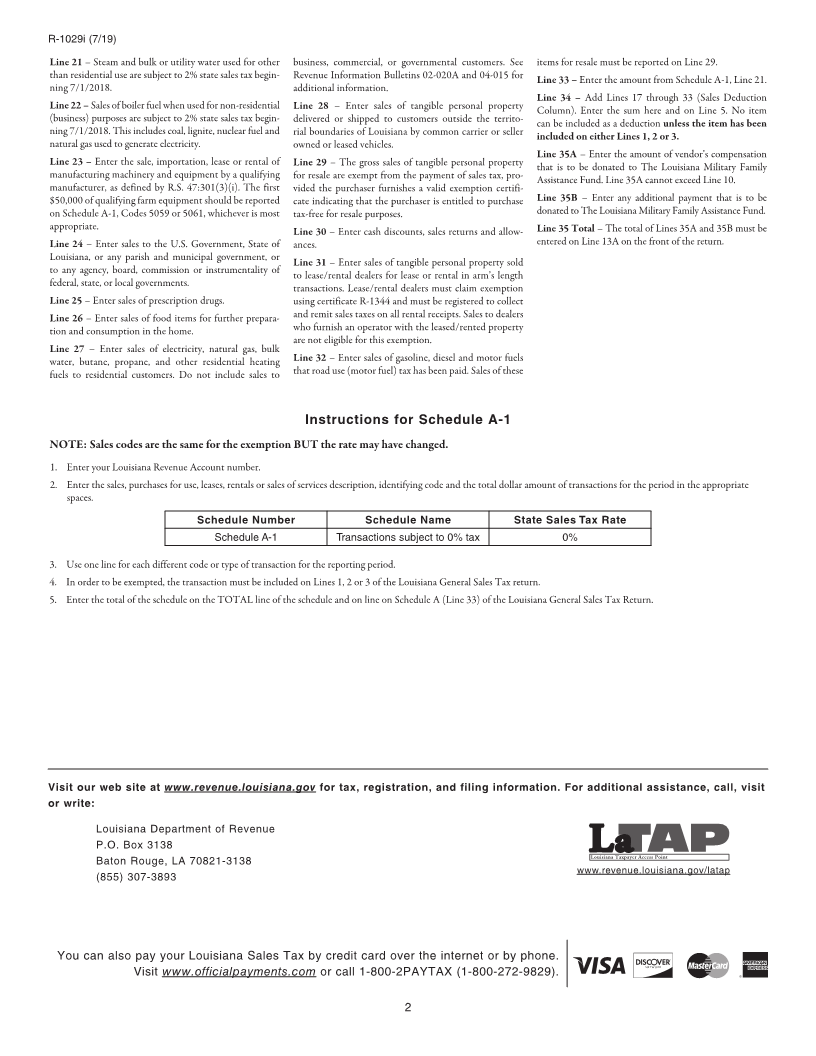

Line 1 – “Gross sales” is the total sales price for each indi- either Line 1, 2, or 3. NOTE – In addition to the delinquent penalties reported

vidual item or article of tangible personal property with Line 6 – Subtract Line 5 from Line 4. above, a taxpayer may also incur a negligence penalty

no reduction for any purpose. All taxable and exempt sales under R.S. 47:1604.1 if circumstances indicate willful neg-

must be entered on this line. Line 7 – Multiply Line 6 by 4.45%. ligence or intentional disregard of rules and regulations.

Line 2 – A use tax is due on the purchaser’s acquisition Line 8 – In cases where the total amount of Louisiana Also, an examination fee may be imposed in the event the

price of the tangible personal property used, consumed, sales or use taxes collected by use of tax-bracket tables Department is required to issue a billing notice necessitated

distributed, stored for use or consumption in Louisiana, exceeds the amount shown on Line 7, any excess must be by the filing or lack of filing of this return.

or purchased or imported into the state for resale in coin- remitted to LDR.

operated vending machines. The total cost or value of the Line 9 – Add Lines 7 and 8. Line 15 – Refer to the Interest Rate Schedule (R-1111) for

monthly interest rates that apply. Form R-1111 is available on

property on which the tax has not been paid to vendors Line 10 – To compute vendor’s compensation, multiply the Department’s website at www.revenue.louisiana.gov.

must be entered on this line. the amount shown on Line 9 by 0.84%. Act 1 of the Third

Line 3 – The gross receipts billed for the lease or rental Extraordinary Session of the 2018 Louisiana Legislature Line 16 – Add Lines 13, 13A, 14, and 15. Make payment

of tangible personal property, as well as the gross receipts imposed a 0.45% sales tax on all taxable transactions in to: Louisiana Department of Revenue. You can file and

from taxable services defined in R.S. 47:301(14) should be Louisiana. Act 15 of the First Extraordinary Session of the pay your Louisiana Sales Tax at www.revenue.louisiana.

included. The eight services subject to state sales tax include 2016 Louisiana Legislature states that the sales tax imposed gov/latap. You can also pay by credit card over the inter-

(1) the furnishing of sleeping rooms, cottages or cabins; (2) pursuant to R.S. 47:321.1 is not eligible for vendor’s com- net or by phone. Visit www.officialpayments.com or call

admissions to places of amusement, athletic, entertainment pensation. The 0.84% rate is the mathematical equivalent 1-800-2PAYTAX (1-800-272-9829).

and recreational events and dues, fees or other consider- of 4 cents out of 4.45 cents (4/4.45) of the .935% vendor’s NOTE – Do not claim credit on Line 16 for any previous

ation for the privilege of accessing clubs or amusement, compensation. Act 15 of the First Extraordinary Session

overpayment. A refund will be issued.

entertainment, athletic or recreational facilities; (3) storage of the 2016 Louisiana Legislature also limited vendor’s

or parking privileges; (4) printing and related services; (5) compensation to $1500 per Louisiana dealer. This com-

laundry, cleaning, pressing and dyeing services of textiles pensation is allowed only if the return is timely filed and Schedule A Instructions for Lines 17 through 34

(includes storage space for clothing, furs and rugs); (6) paid. See Revenue Information Bulletin No. 16-015. Enter the sales amounts for this reporting period in

furnishing of cold storage space; (7) repairs to tangible the boxes provided in the total sales column. Multiply

personal property and (8) taxable telecommunication ser- Vendor’s compensation as provided by LA R.S. 47:306(A) these sales amounts by the percent factor appearing

vices, such as charges for intrastate and interstate telephone (3)(a) is allowed only when the dealer remits all sales tax as in the middle col umn and enter the result in the Sales

calls, cellular telephone calls, and pager services. Additional shown due on the return. Partial vendor’s compensation Deduction boxes appearing in the right-hand column.

information regarding the taxation of these transactions for a partial payment of sales tax due is not allowed. The sales amount must also be included on Line 1, 2, or 3

can be found at www.revenue.louisiana.gov. for allowable deductions claimed on Schedule A.

Line 11 – Subtract Line 10 from Line 9.

NOTE – Dealers who collect sales tax on motor vehicle leases Line 17 – Report intrastate telecommunication services,

and rentals are required to complete a special electronic reg- Line 12 – This line is intentionally left blank. such as local telephone calls, cellular telephone charges,

istration and file their sales tax returns electronically using Line 13 – Same as Line 11. and pager service charges on this line. Do not include

a different tax return that allows for separately reporting Line 13A – Taxpayers may donate to The Louisiana prepaid telephone calling cards on this line.

the sales tax collected on the motor vehicle leases and rentals. Military Family Assistance Fund by entering the amount of Line 18 – Report interstate telecommunication services on

In addition, dealers who collect sales tax on hotel/motel the donation on Lines 35A and 35B and entering the total this line. These include any taxable telecommunication servic-

room rentals are also required to complete a special electronic of those donations on Lines 35 and 13A. Donations can be es that originate in Louisiana and terminate outside Louisiana,

registration and file their sales tax returns electronically made by: 1) contributing all or any portion of the vendor’s or that originate outside Louisiana and terminate in Louisiana,

using a different tax return that allows for separate sales compensation listed on Line 10; or 2) paying an amount in and that are charged to a Louisiana address regardless of where

tax reporting. addition to the net tax due on Line 13 of this return. The the amount is billed or paid.

To register and file your sales tax return electronically using amount entered on Line 13A must equal Line 35. Line 19 – Enter sales of prepaid telephone calling cards.

the Louisiana Taxpayer Access Point (LaTAP), visit our Line 14 – A return becomes delinquent on the day after Prepaid telephone calling cards are paid in advance in

website at www.revenue.louisiana.gov. the due date as discussed in the General Instructions above. predetermined amounts that decline with use.

If the return is filed late, a delinquent penalty of 5 percent Line 20 – Sales of electricity and natural gas or energy for

Line 4 – Add Lines 1 through 3. for each 30 days or fraction thereof of delinquency, not to nonresidential use are subject to 2% state sales tax begin-

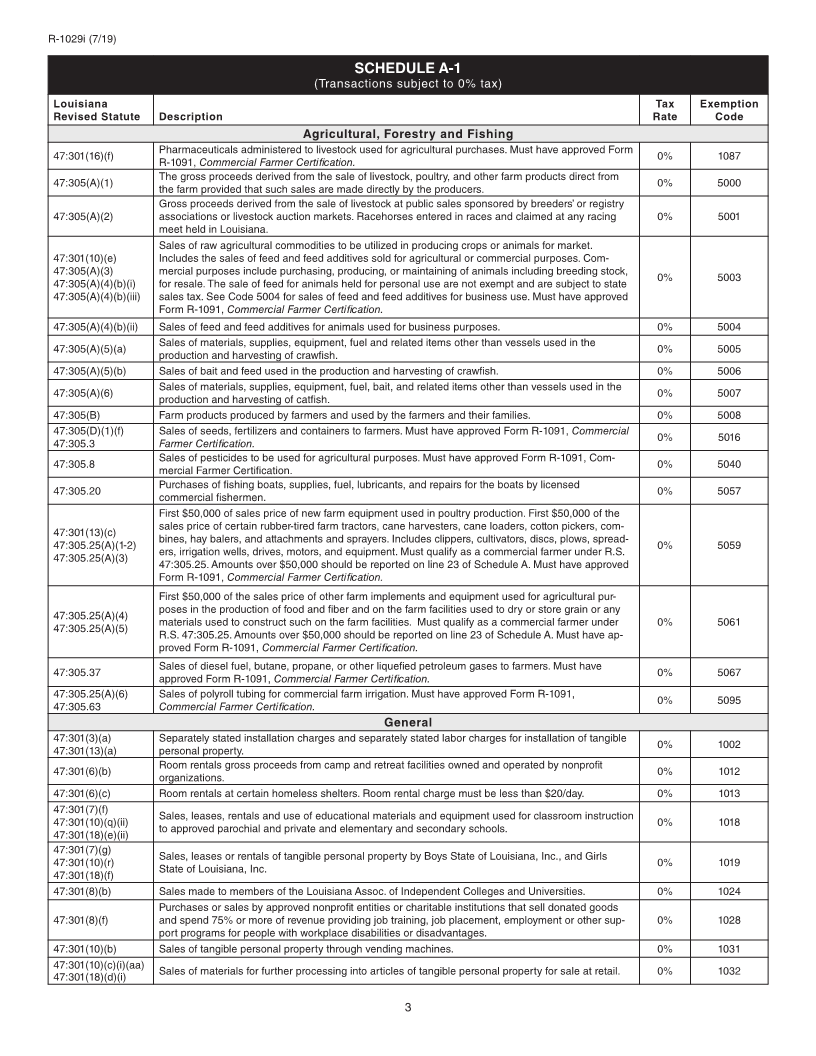

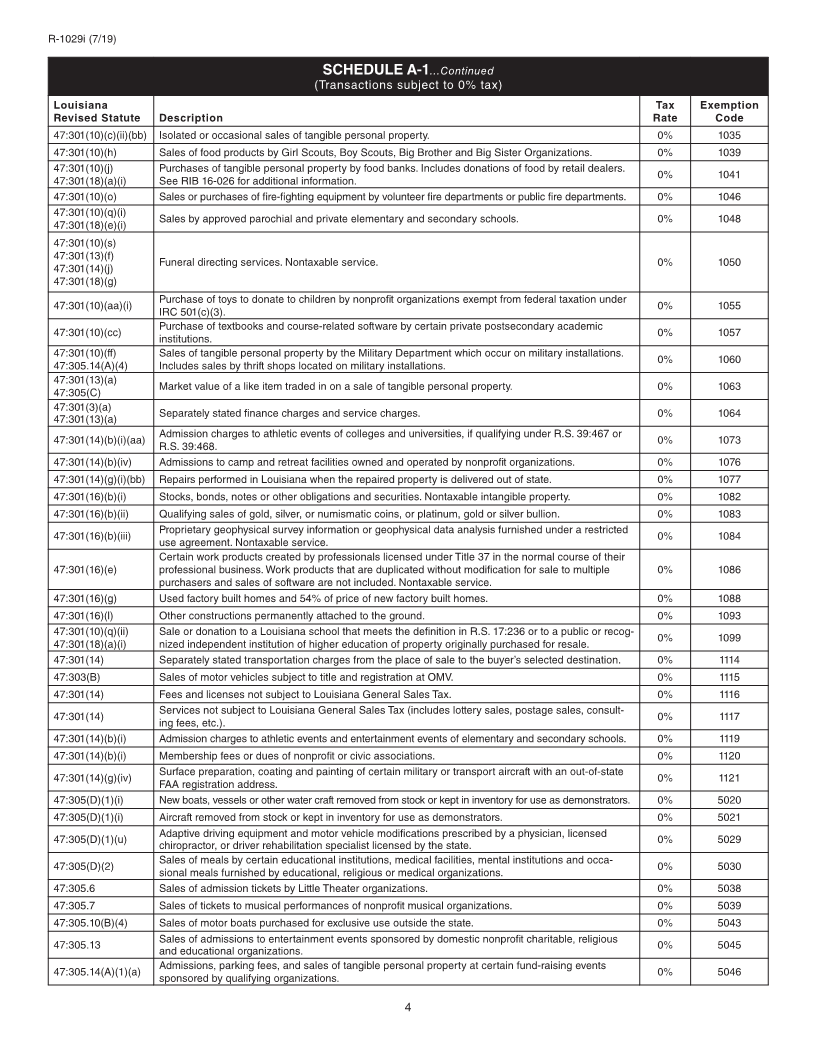

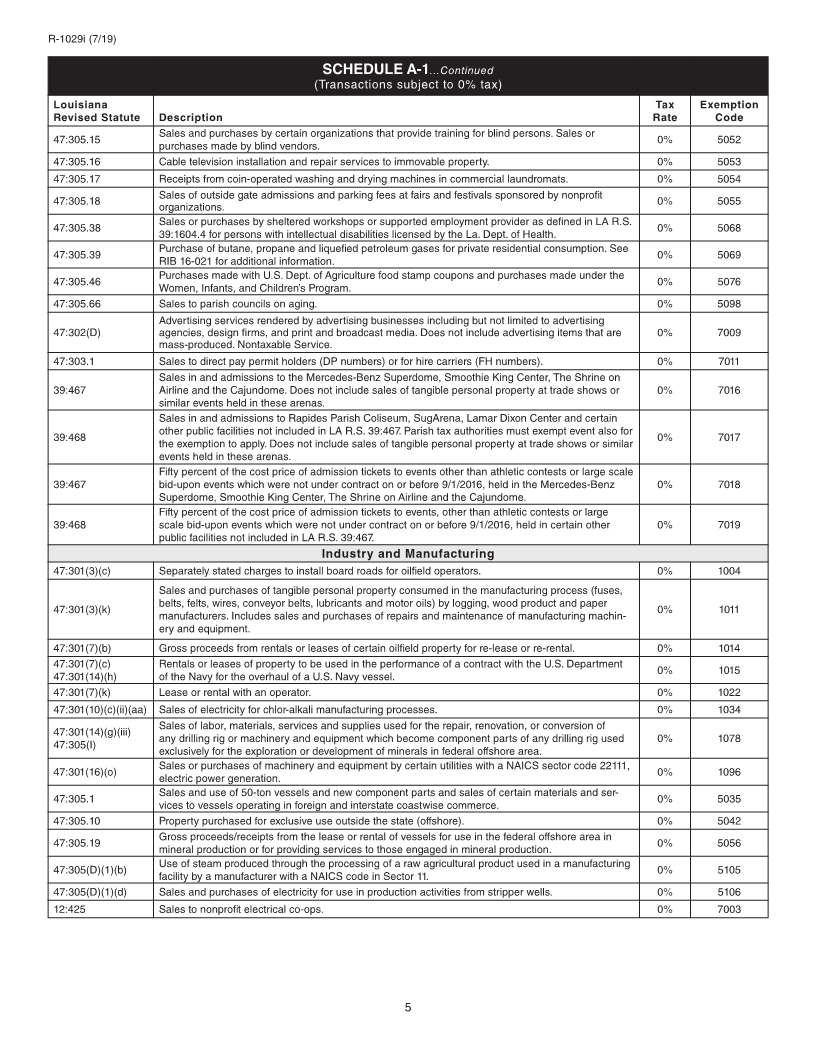

Line 5 – (From Line 34-Schedule A) No deduction can exceed 25 percent of the net tax due on Line 13, must be ning 7/1/2018.

be claimed unless the transaction has been included on entered on Line 14.

1