Enlarge image

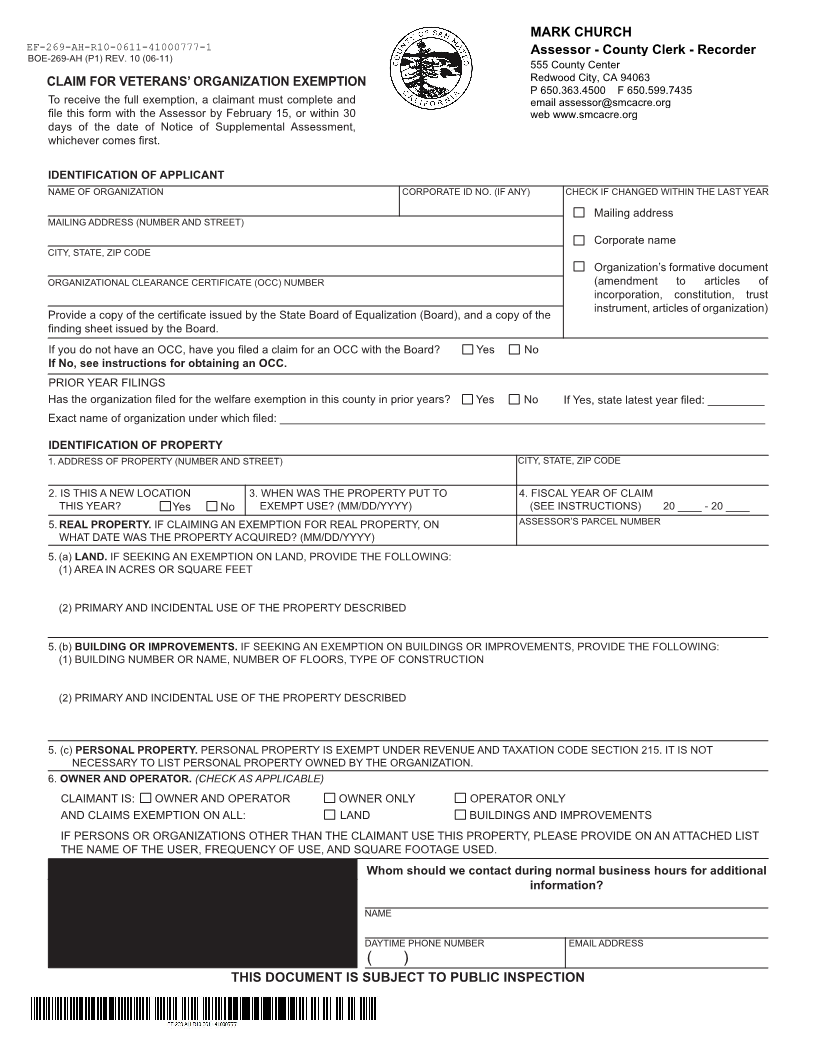

MARK CHURCH

EF-269-AH-R10-0611-41000777-1 Assessor - County Clerk - Recorder

BOE-269-AH (P1) REV. 10 (0 -6 11) 555 County Center

Redwood City, CA 94063

CLAIM FOR VETERANS’ ORGANIZATION EXEMPTION P 650.363.4500 F 650.599.7435

To receive the full exemption, a claimant must complete and email assessor@smcacre.org

file this form with the Assessor by February 15, or within 30 web www.smcacre.org

days of the date of Notice of Supplemental Assessment,

whichever comes first.

IDENTIFICATION OF APPLICANT

NAME OF ORGANIZATION CORPORATE ID NO. (IF ANY) CHECK IF CHANGED WITHIN THE LAST YEAR

Mailing address

MAILING ADDRESS (NUMBER AND STREET)

Corporate name

CITY, STATE, ZIP CODE

Organization’s formative document

ORGANIZATIONAL CLEARANCE CERTIFICATE (OCC) NUMBER (amendment to articles of

incorporation, constitution, trust

instrument, articles of organization)

Provide a copy of the certificate issued by the State Board of Equalization (Board), and a copy of the

finding sheet issued by the Board.

If you do not have an OCC, have you filed a claim for an OCC with the Board? Yes No

If No, see instructions for obtaining an OCC.

PRIOR YEAR FILINGS

Has the organization filed for the welfare exemption in this county in prior years? Yes No If Yes, state latest year filed: _________

Exact name of organization under which filed: _____________________________________________________________________________

IDENTIFICATION OF PROPERTY

1. ADDRESS OF PROPERTY (NUMBER AND STREET) CITY, STATE, ZIP CODE

2. IS THIS A NEW LOCATION 3. WHEN WAS THE PROPERTY PUT TO 4. FISCAL YEAR OF CLAIM

THIS YEAR? Yes No EXEMPT USE? (MM/DD/YYYY) (SEE INSTRUCTIONS) 20 ____ - 20 ____

5. REAL PROPERTY. IF CLAIMING AN EXEMPTION FOR REAL PROPERTY, ON ASSESSOR’S PARCEL NUMBER

WHAT DATE WAS THE PROPERTY ACQUIRED? (MM/DD/YYYY)

5. (a) LAND. IF SEEKING AN EXEMPTION ON LAND, PROVIDE THE FOLLOWING:

(1) AREA IN ACRES OR SQUARE FEET

(2) PRIMARY AND INCIDENTAL USE OF THE PROPERTY DESCRIBED

5. (b) BUILDING OR IMPROVEMENTS. IF SEEKING AN EXEMPTION ON BUILDINGS OR IMPROVEMENTS, PROVIDE THE FOLLOWING:

(1) BUILDING NUMBER OR NAME, NUMBER OF FLOORS, TYPE OF CONSTRUCTION

(2) PRIMARY AND INCIDENTAL USE OF THE PROPERTY DESCRIBED

5. (c) PERSONAL PROPERTY. PERSONAL PROPERTY IS EXEMPT UNDER REVENUE AND TAXATION CODE SECTION 215. IT IS NOT

NECESSARY TO LIST PERSONAL PROPERTY OWNED BY THE ORGANIZATION.

6. OWNER AND OPERATOR. (CHECK AS APPLICABLE)

CLAIMANT IS: OWNER AND OPERATOR OWNER ONLY OPERATOR ONLY

AND CLAIMS EXEMPTION ON ALL: LAND BUILDINGS AND IMPROVEMENTS

IF PERSONS OR ORGANIZATIONS OTHER THAN THE CLAIMANT USE THIS PROPERTY, PLEASE PROVIDE ON AN ATTACHED LIST

THE NAME OF THE USER, FREQUENCY OF USE, AND SQUARE FOOTAGE USED.

FOR ASSESSOR’S USE ONLY Whom should we contact during normal business hours for additional

information?

Received by (Assessor’s designee) NAME

of (county or city) on (date) DAYTIME PHONE NUMBER EMAIL ADDRESS

( )

THIS DOCUMENT IS SUBJECT TO PUBLIC INSPECTION