Enlarge image

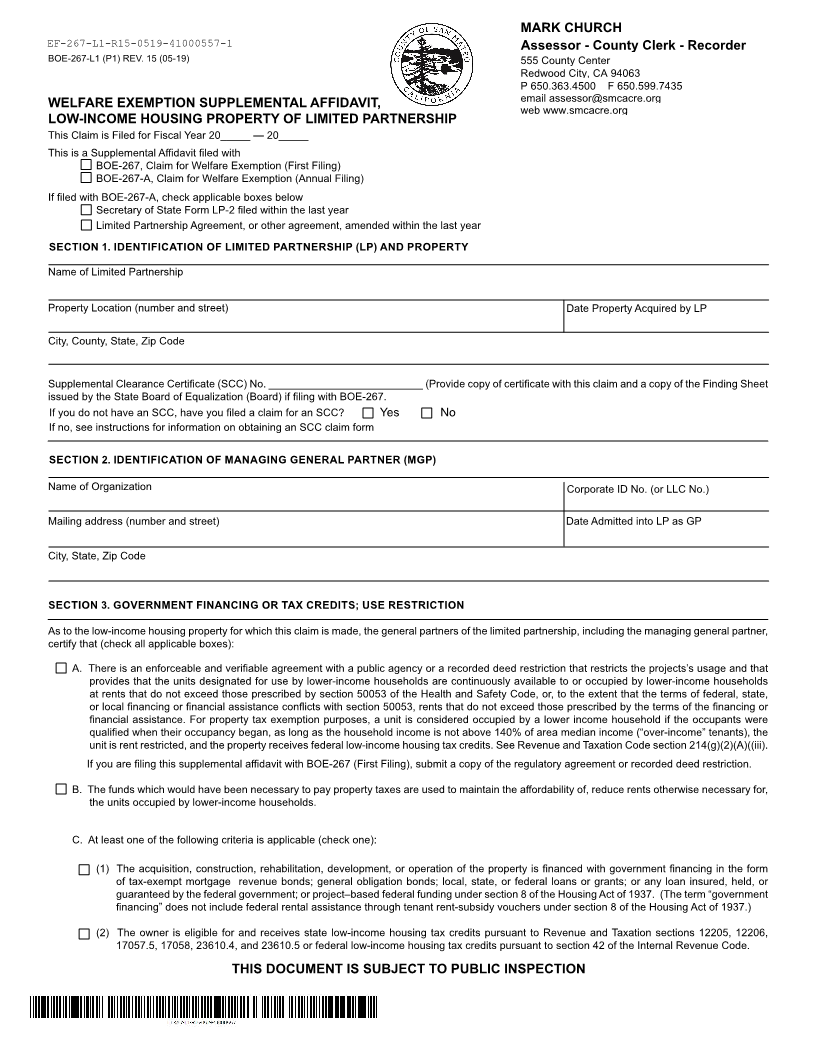

MARK CHURCH

EF-267-L1-R15-0519-41000557-1 Assessor - County Clerk - Recorder

BOE-267-L1 (P1) REV. 15 (05-19) 555 County Center

Redwood City, CA 94063

P 650.363.4500 F 650.599.7435

email assessor@smcacre.org

WELFARE EXEMPTION SUPPLEMENTAL AFFIDAVIT, web www.smcacre.org

LOW-INCOME HOUSING PROPERTY OF LIMITED PARTNERSHIP

This Claim is Filed for Fiscal Year 20_____ — 20_____

This is a Supplemental Affidavit filed with

BOE-267, Claim for Welfare Exemption (First Filing)

BOE-267-A, Claim for Welfare Exemption (Annual Filing)

If filed with BOE-267-A, check applicable boxes below

Secretary of State Form LP-2 filed within the last year

Limited Partnership Agreement, or other agreement, amended within the last year

SECTION 1. IDENTIFICATION OF LIMITED PARTNERSHIP (LP) AND PROPERTY

Name of Limited Partnership

Property Location (number and street) Date Property Acquired by LP

City, County, State, Zip Code

Supplemental Clearance Certificate (SCC) No. __________________________ (Provide copy of certificate with this claim and a copy of the Finding Sheet

issued by the State Board of Equalization (Board) if filing with BOE-267.

If you do not have an SCC, have you filed a claim for an SCC? Yes No

If no, see instructions for information on obtaining an SCC claim form

SECTION 2. IDENTIFICATION OF MANAGING GENERAL PARTNER (MGP)

Name of Organization Corporate ID No. (or LLC No.)

Mailing address (number and street) Date Admitted into LP as GP

City, State, Zip Code

SECTION 3. GOVERNMENT FINANCING OR TAX CREDITS; USE RESTRICTION

As to the low-income housing property for which this claim is made, the general partners of the limited partnership, including the managing general partner,

certify that (check all applicable boxes):

A. There is an enforceable and verifiable agreement with a public agency or a recorded deed restriction that restricts the projects’s usage and that

provides that the units designated for use by lower-income households are continuously available to or occupied by lower-income households

at rents that do not exceed those prescribed by section 50053 of the Health and Safety Code, or, to the extent that the terms of federal, state,

or local financing or financial assistance conflicts with section 50053, rents that do not exceed those prescribed by the terms of the financing or

financial assistance. For property tax exemption purposes, a unit is considered occupied by a lower income household if the occupants were

qualified when their occupancy began, as long as the household income is not above 140% of area median income (“over-income” tenants), the

unit is rent restricted, and the property receives federal low-income housing tax credits. See Revenue and Taxation Code section 214(g)(2)(A)((iii).

If you are filing this supplemental affidavit with BOE-267 (First Filing), submit a copy of the regulatory agreement or recorded deed restriction.

B. The funds which would have been necessary to pay property taxes are used to maintain the affordability of, reduce rents otherwise necessary for,

the units occupied by lower-income households.

C. At least one of the following criteria is applicable (check one):

(1) The acquisition, construction, rehabilitation, development, or operation of the property is financed with government financing in the form

of tax-exempt mortgage revenue bonds; general obligation bonds; local, state, or federal loans or grants; or any loan insured, held, or

guaranteed by the federal government; or project–based federal funding under section 8 of the Housing Act of 1937. (The term “government

financing” does not include federal rental assistance through tenant rent-subsidy vouchers under section 8 of the Housing Act of 1937.)

(2) The owner is eligible for and receives state low-income housing tax credits pursuant to Revenue and Taxation sections 12205, 12206,

17057.5, 17058, 23610.4, and 23610.5 or federal low-income housing tax credits pursuant to section 42 of the Internal Revenue Code.

THIS DOCUMENT IS SUBJECT TO PUBLIC INSPECTION