Enlarge image

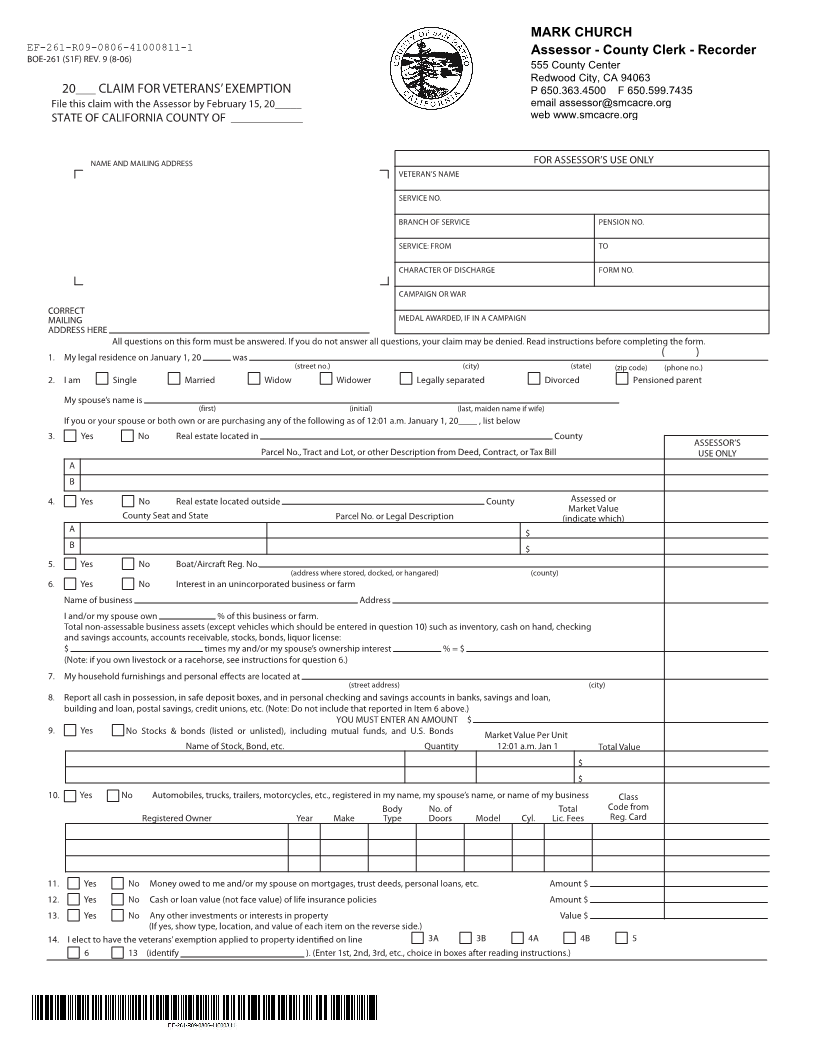

MARK CHURCH

EF-261-R09-0806-41000811-1 Assessor - County Clerk - Recorder

BOE-261 (S1F) REV. 9 (8-06) 555 County Center

Redwood City, CA 94063

20___ CLAIM FOR VETERANS’ EXEMPTION P 650.363.4500 F 650.599.7435

File this claim with the Assessor by February 15, 20_____ email assessor@smcacre.org

STATE OF CALIFORNIA COUNTY OF ____________ web www.smcacre.org

NAME AND MAILING ADDRESS FOR ASSESSOR’S USE ONLY

VETERAN’S NAME

SERVICE NO.

BRANCH OF SERVICE PENSION NO.

SERVICE: FROM TO

CHARACTER OF DISCHARGE FORM NO.

CAMPAIGN OR WAR

CORRECT MEDAL AWARDED, IF IN A CAMPAIGN

MAILING

ADDRESS HERE

All questions on this form must be answered. If you do not answer all questions, your claim may be denied. Read instructions before completing the form.

1. My legal residence on January 1, 20 was ( )

(street no.) (city) (state) (zip code) (phone no.)

2. I am Single Married Widow Widower Legally separated Divorced Pensioned parent

My spouse’s name is

(first) (initial) (last, maiden name if wife)

If you or your spouse or both own or are purchasing any of the following as of 12:01 a.m. January 1, 20____ , list below

3. Yes No Real estate located in County

ASSESSOR’S

Parcel No., Tract and Lot, or other Description from Deed, Contract, or Tax Bill USE ONLY

A

B

4. Yes No Real estate located outside County Assessed or

Market Value

County Seat and State Parcel No. or Legal Description (indicate which)

A $

B $

5. Yes No Boat/Aircraft Reg. No.

(address where stored, docked, or hangared) (county)

6. Yes No Interest in an unincorporated business or farm

Name of business Address

I and/or my spouse own % of this business or farm.

Total non-assessable business assets (except vehicles which should be entered in question 10) such as inventory, cash on hand, checking

and savings accounts, accounts receivable, stocks, bonds, liquor license:

$ times my and/or my spouse’s ownership interest % = $

(Note: if you own livestock or a racehorse, see instructions for question 6.)

7. My household furnishings and personal effects are located at

(street address) (city)

8. Report all cash in possession, in safe deposit boxes, and in personal checking and savings accounts in banks, savings and loan,

building and loan, postal savings, credit unions, etc. (Note: Do not include that reported in Item 6 above.)

YOU MUST ENTER AN AMOUNT $

9. Yes No Stocks & bonds (listed or unlisted), including mutual funds, and U.S. Bonds Market Value Per Unit

Name of Stock, Bond, etc. Quantity 12:01 a.m. Jan 1 Total Value

$

$

10. Yes No Automobiles, trucks, trailers, motorcycles, etc., registered in my name, my spouse’s name, or name of my business Class

Body No. of Total Code from

Registered Owner Year Make Type Doors Model Cyl. Lic. Fees Reg. Card

11. Yes No Money owed to me and/or my spouse on mortgages, trust deeds, personal loans, etc. Amount $

12. Yes No Cash or loan value (not face value) of life insurance policies Amount $

13. Yes No Any other investments or interests in property Value $

(If yes, show type, location, and value of each item on the reverse side.)

14. I elect to have the veterans’ exemption applied to property identified on line 3A 3B 4A 4B 5

6 13 (identify ). (Enter 1st, 2nd, 3rd, etc., choice in boxes after reading instructions.)